While oil and gas producers in the Permian Basin are undoubtedly concerned about gas prices, their response to economic forces, particularly in the gas market, has been limited. Oil remains the dominant revenue stream in the Permian, leading operators to prioritize oil operations that create an abundance of associated natural gas. Gas prices at the Waha Hub have suffered greatly in 2024 as gas production continually tests available outbound capacity.

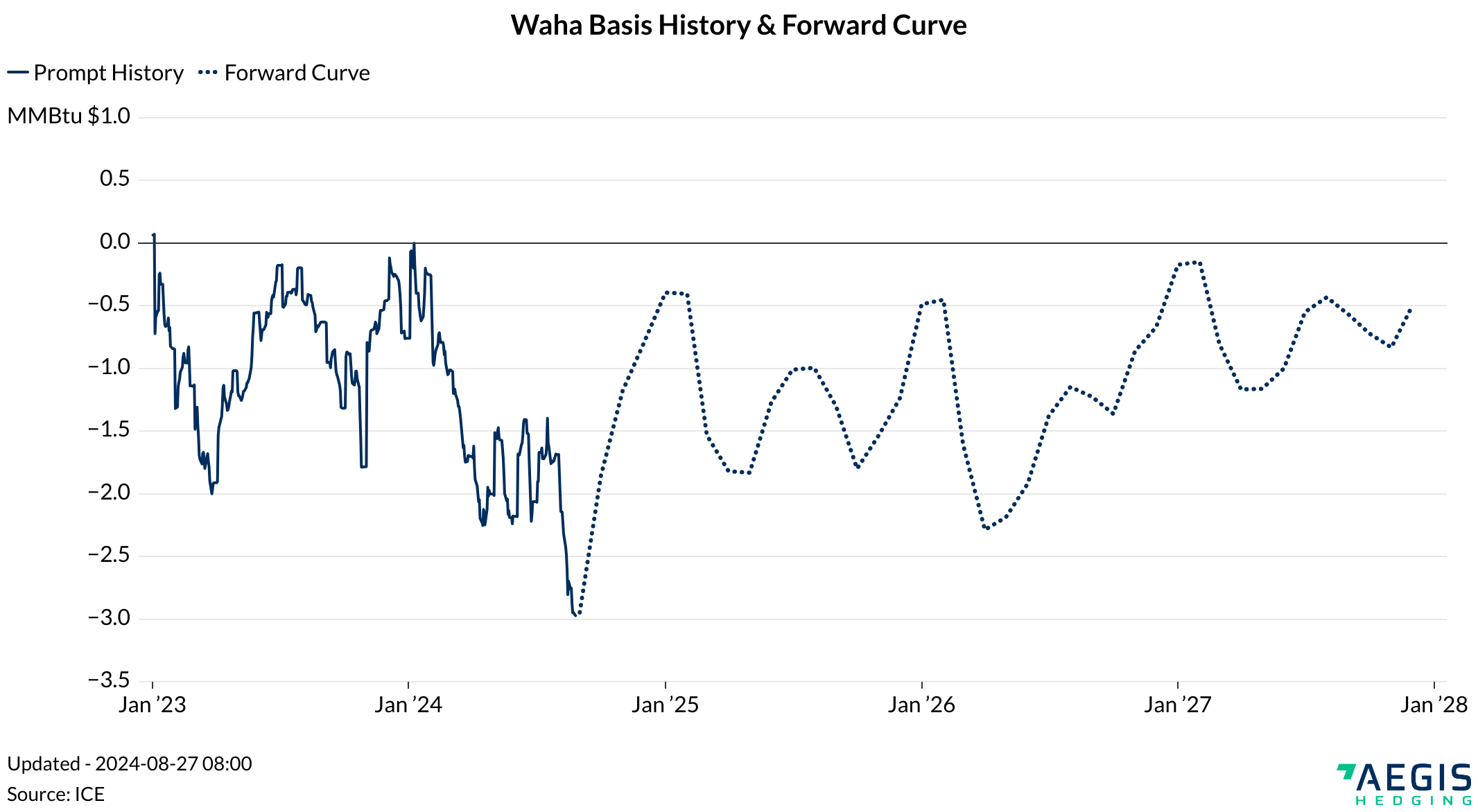

Permian producers often find themselves in a constant race to expand takeaway capacity as rising supply strains existing egress options, necessitating new pipelines or expansions to manage the increased production. The chart above illustrates historical Waha basis prices alongside the forward curve.

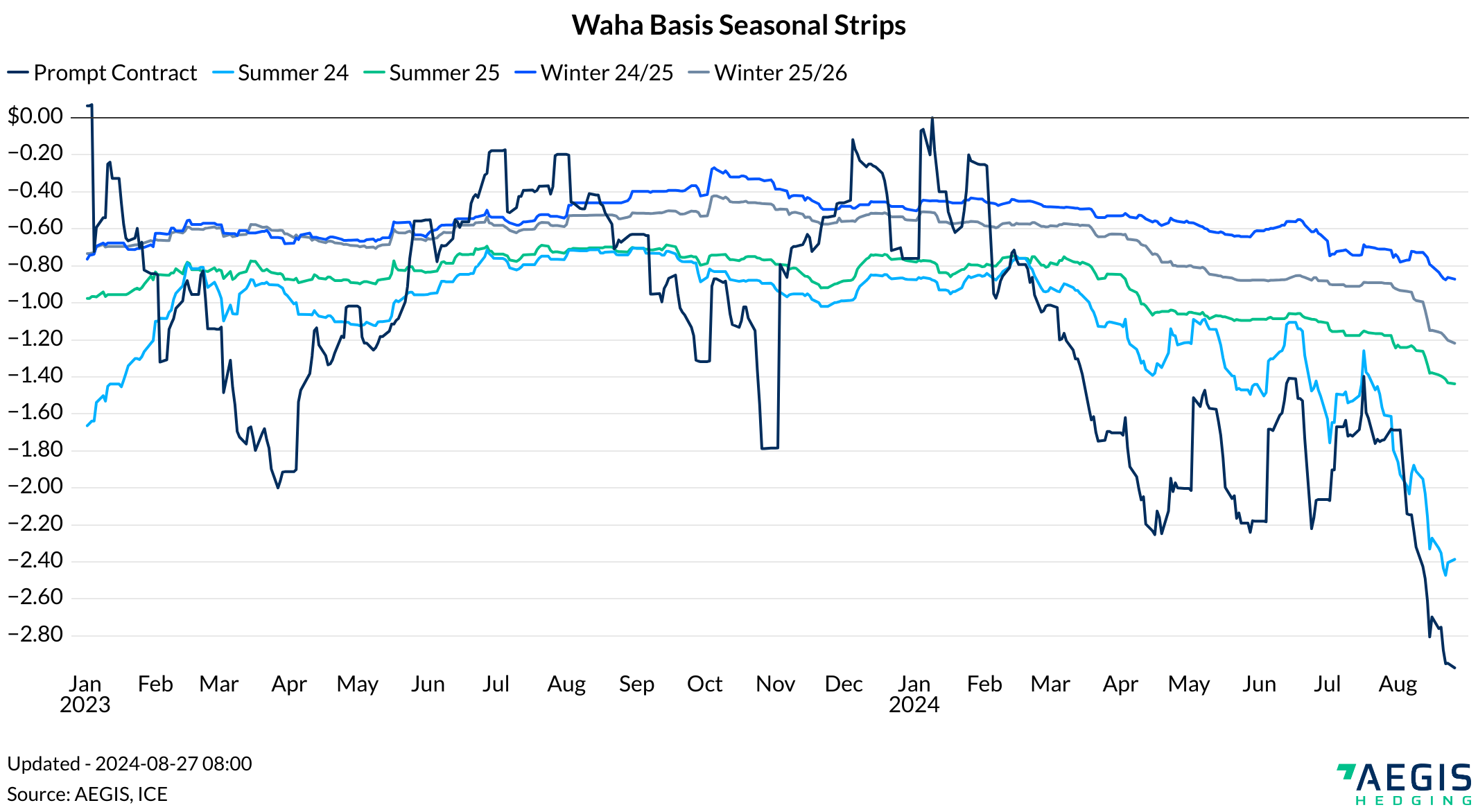

While this static view provides insight, it doesn't capture the evolution of the curve over time, which is better represented in the seasonal strips chart below. For this, we can focus attention to the chart below that shows select seasonal strips over time.

Note the ongoing decline in forward pricing for Waha, reflecting market expectations of persistent egress challenges despite new pipeline additions. Since the start of 2024, forward strips have trended lower with the anticipation of continued egress issues despite new incoming pipe.

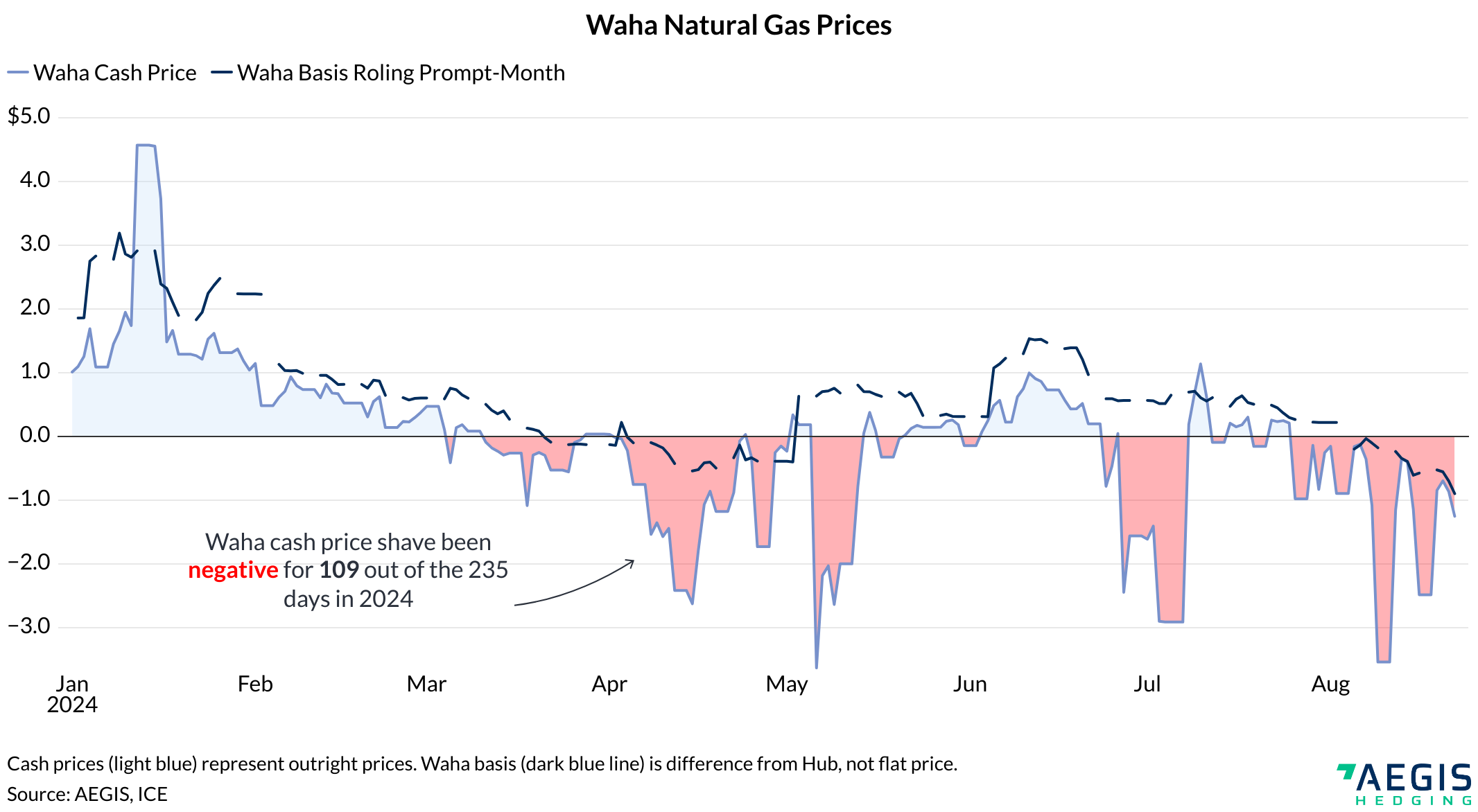

Turning to more real-time price weakness. With producers operating at the very edge of the basin’s available takeaway capacity, Waha gas prices have frequently settled in negative territory for both the prompt-month and cash markets. Waha cash market behavior, shown below, highlights how unfavorable pricing has been up to this point in 2024. As of this writing, Waha spot prices have settled negative on 109 out of the 235 days (including weekend pricing) so far in 2024, representing a staggering 47% of the time!

Receive daily insights into oil and natural gas markets from AEGIS experts, delivered directly to your inbox—for free. Subscribe Now

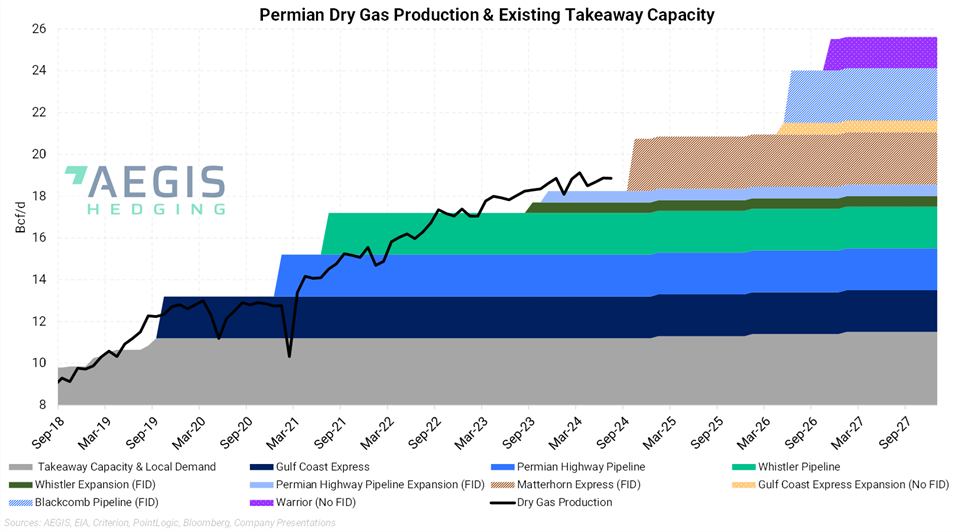

It all comes down to takeaway capacity versus supply. As we sit here today, the modeled Permian supply is straining the daily available takeaway capacity. The graph below shows that help is on the way in the near term in the form of the 2.5 Bcf/d Matterhorn pipeline (brown stacked area). This large greenfield pipeline provides the much-needed takeaway relief that is causing such acute weakness at Waha.

Opinions differ on how quickly the Matterhorn pipeline will reach capacity, with some suggesting it could be filled by next spring. This capacity won't necessarily handle all new gas; instead, existing supply may be rerouted from less desirable corridors, like West Texas to Midcontinent. The extent of "new" gas entering the market in the next three to six months post-Matterhorn will be crucial.

While the Matterhorn pipeline offers some relief, it may be short-lived. There is still significant weakness in the Waha forward curve for Cal 2025 and Cal 2026. The front of the curve at nearly -$3.00/MMBtu aligns with our earlier discussion, but the discounts of around -$1.25 to -$1.29 for Cal 2025 and Cal 2026 raise questions. A weak Cal 2026 is understandable, given the next major pipeline isn't due until late 2026, WhiteWater’s Blackcomb pipeline. However, Cal 2025 being similarly discounted might suggest severe 2024 weakness is dragging it down, or traders are highly bullish on Permian supply, expecting egress to fill sooner rather than later. In any case, Permian gas prices face an uphill battle unless oil prices shift significantly.

The current forward curve suggests Waha gas prices are likely to remain volatile and weak, reflecting the ongoing challenge of balancing production growth with infrastructure development in the Permian Basin.