Aluminum stumbles in early 2024, but bullish news emerges.When the calendar turned to 2024, the LME Aluminum 3M contract hovered near $2,375/mt, having rallied nearly 11% in the final three weeks of 2023. Prior to the rally, the benchmark LME 3M contract was near the lowest level since October 2022. This bounce has quickly faltered in the first weeks of 2024. |

|

|

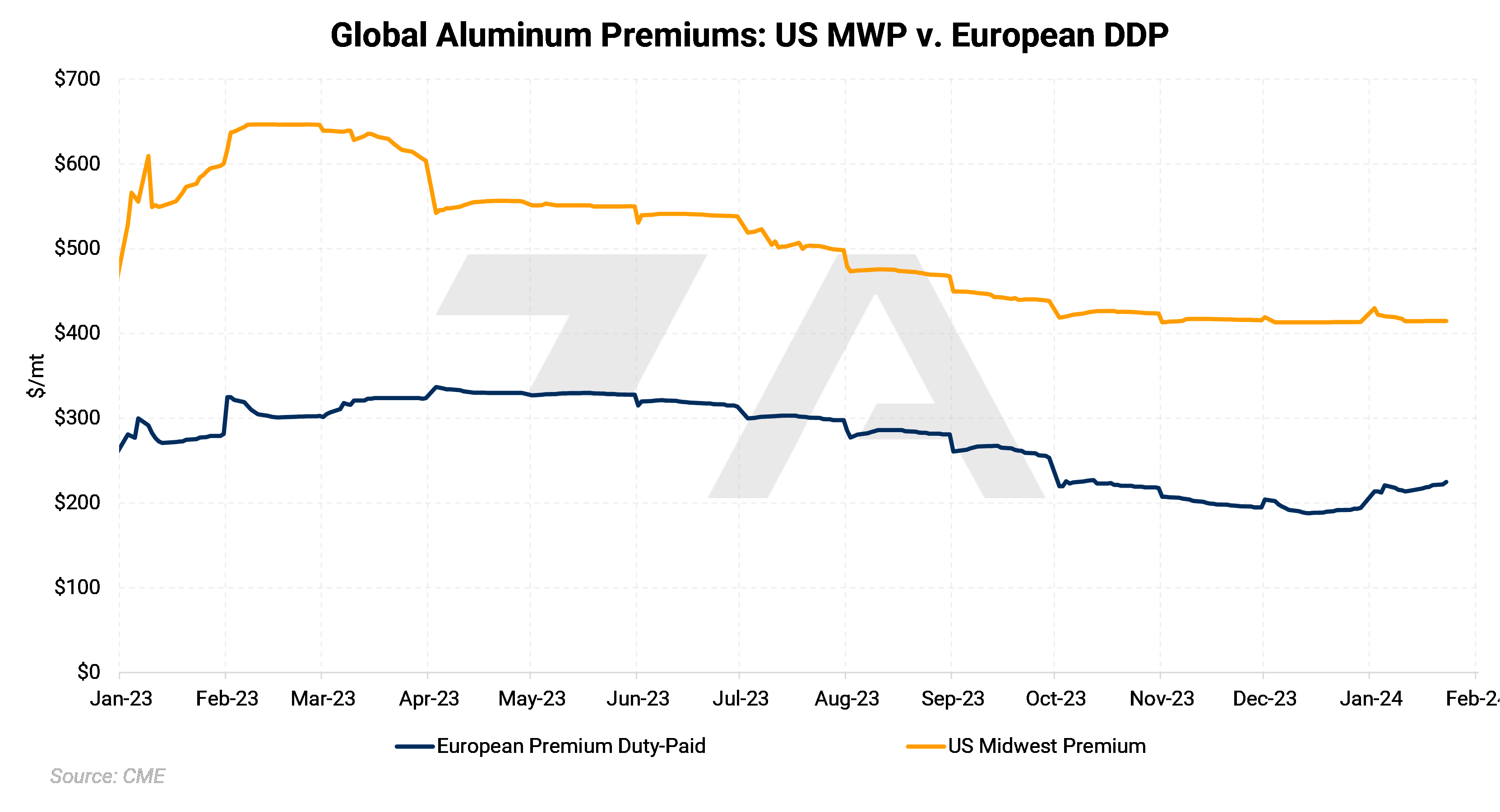

Import premiums are starting to trend higher.On January 23rd, aluminum prices surged on reports that the EU might sanction Russian aluminum. The EU’s ability to implement these sanctions remains unclear, as doing so requires a unanimous decision by all 27 EU members. Since the beginning of the Russian-Ukraine conflict in early 2022, trading Russian metals has been a controversial subject in political circles and the physical market, with many physical buyers and sellers shunning Russian metals. Through September 2023, approximately 11% of the EU’s unalloyed and unwrought primary aluminum imports came from Russia, down from 20% during the same period in 2022 and 2021. (Sources: Bloomberg, Reuters) This news could be bullish for international import premiums. Prompt month CME European Duty Paid Premium futures jumped slightly on yesterday’s news, but prompt month CME MWP futures were little changed. The European premium had previously bottomed in mid-December and rallied from approximately $188/mt to $224/mt as of the January 23 close. Meanwhile, the prompt month Midwest Premium has been essentially flat since mid-November, but the futures forward curve has developed in that time. If the EU does ban imports of Russian imports, both premiums could rally as the US competes against the EU for the same non-Russian metal. (Source: CME) |

|

|

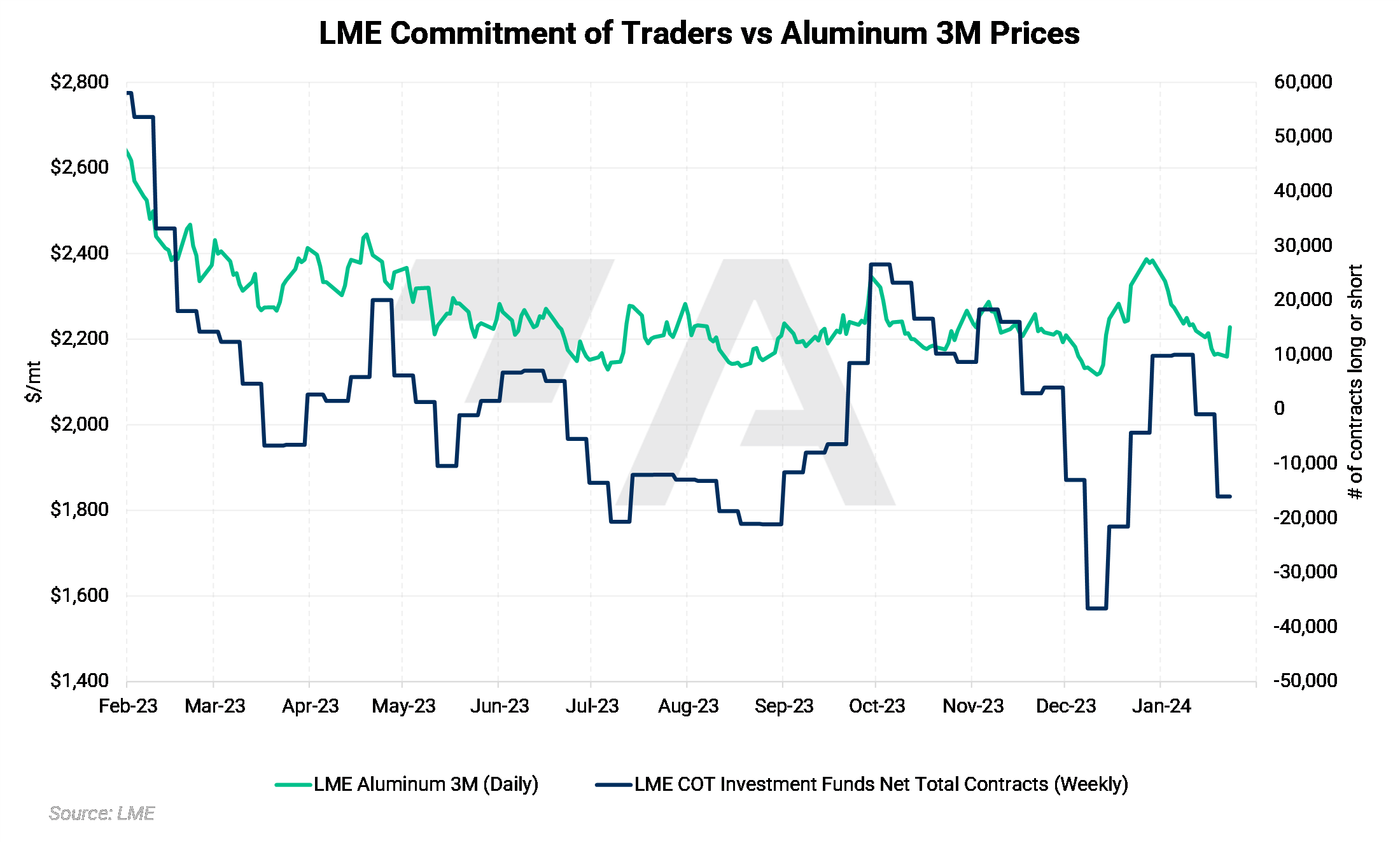

What will funds do?Investment funds, which are generally considered speculators in metals markets, can have an oversized influence on LME aluminum prices. As the chart below shows, the movements in LME aluminum prices are nearly lockstep with the actions of investment funds. As of this writing, these funds are short LME aluminum. However, that position can quickly change, especially if there are significant supply or demand issues. Investment funds likely did some short covering on the reports of the EU’s potential ban on Russian metals, but it is unclear if funds will feel that this is a long-term bullish catalyst for LME aluminum. |

|

|

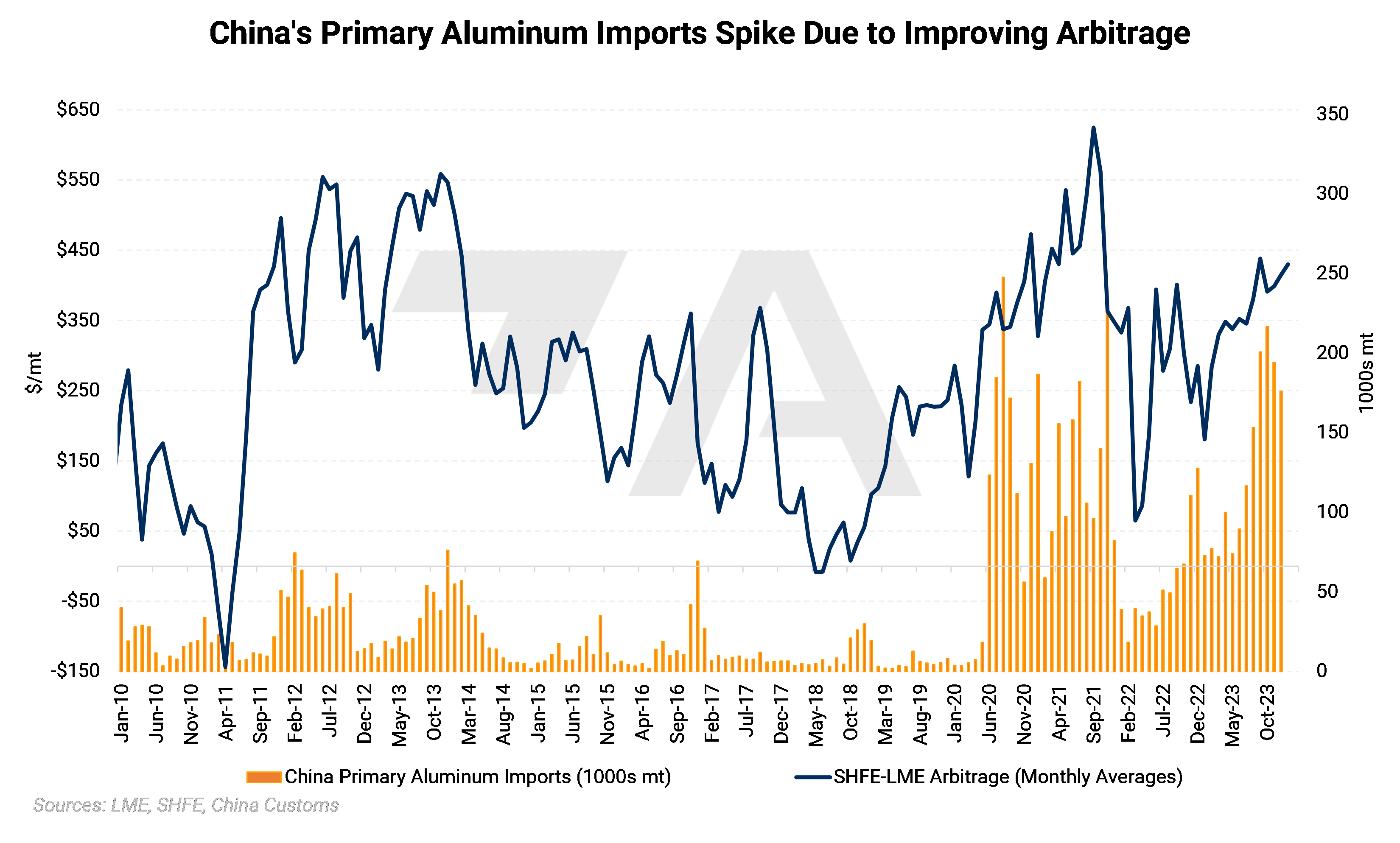

Are there any other potential bright spots?One factor that AEGIS will keep an eye on in 2024 is Chinese primary aluminum imports. Throughout 2023, SHFE aluminum prices remained strong relative to the LME. The spread between these two prices, known as arbitrage, subsequently widened throughout most of 2023, leading to higher imports into China. If this spread remains strong in 2024, then we should expect imports to continue at a brisk pace. This import demand could be supportive to both SHFE and LME prices. |

|

|

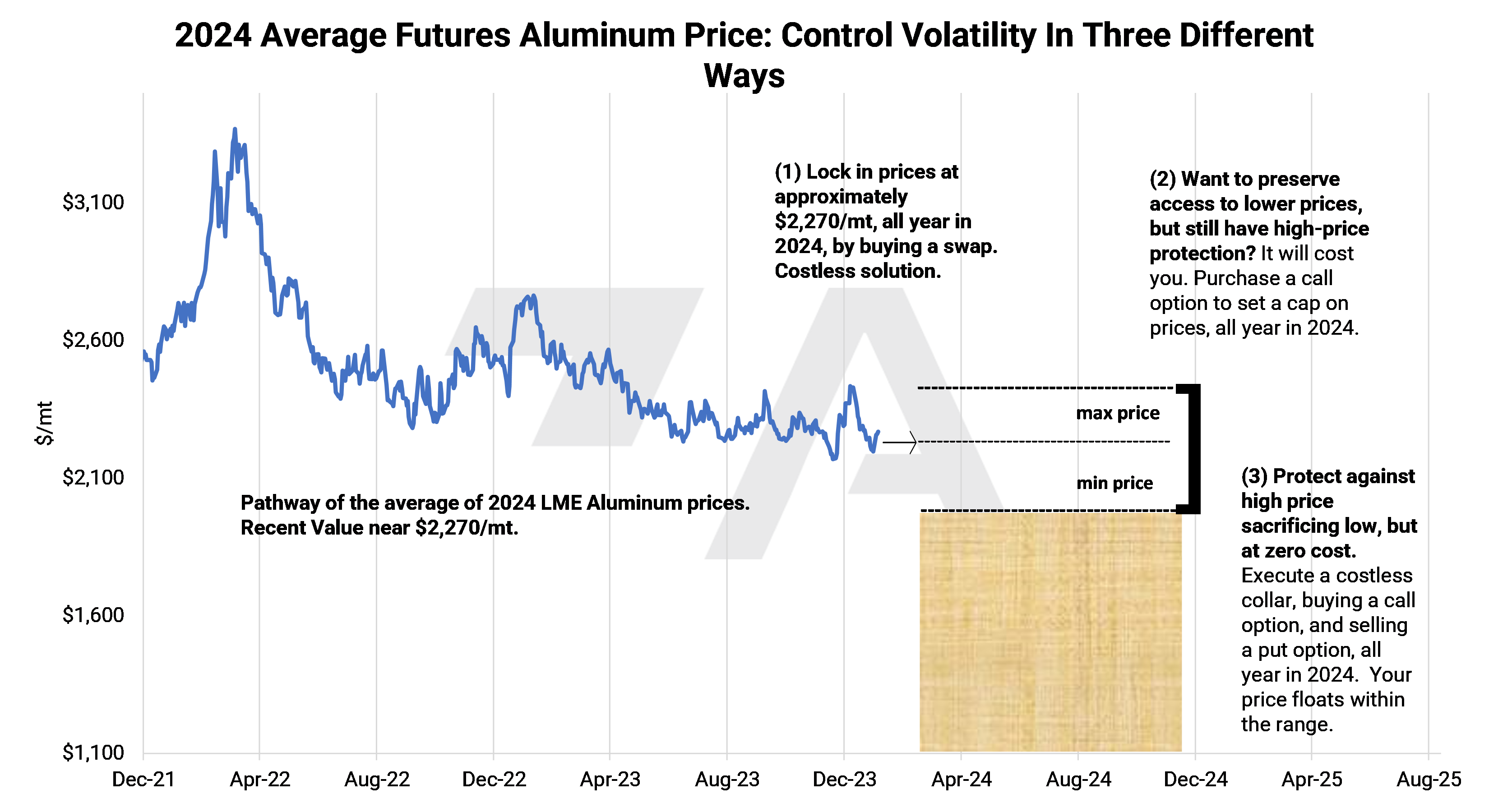

This price risk can be hedged!Even though LME aluminum remains in a downtrend, aluminum end-users should consider doing long-term hedging while prices are near the lower end of the recent trading range. Below, we detail several strategies that end-users could implement. Please contact us for more information and specific strategies. As for the CME MWP, AEGIS can also help consumers who need coverage in that market. However, swaps are thinly traded, and there is no options market. Again, please contact us for more information and specific strategies. |

|

|

AEGIS can build your hedging program.AEGIS can help aluminum buyers develop specific strategies that fit their operations. We are also happy to introduce new clients to more counterparties, therefore ensuring that you are receiving the best possible price. Please contact us for details. |

Important Disclosure: Indicative prices are provided for information purposes only and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee of the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as "edge," "advantage," "opportunity," "believe," or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.