Metals markets started on a down note this week, as Chinese economic data released late last week and over the weekend suggest their economy is slowing. The Caixin Manufacturers PMI, released Thursday, July 1, was pegged at 51.3, down from 52.0 the prior month. Its most recent peak was November 2020 at 54.9. Likewise, the Caixin Services PMI, released Monday, July 4, was pegged at 50.3, down from 55.0 the month prior (a 14-month low). Its most recent peak was June 2020 at 58.4. |

|||||

|

Both indices provide an overall view of their respective sectors and the Chinese economy. A reading below 50.0 implies contraction in the sector, above 50.0 implies expansion. AEGIS notes that the PMI is a survey of purchasing managers, likely the first managers in a company, to determine if they foresee increasing their output. Therefore, it is often understood as a leading, or predictive, indicator. Until recently, metals have been unfazed by the supposed slowdown; however, renewed COVID fears and the potential of new lockdowns could keep a cap on prices. On Wednesday China announced that it will implement a variety of monetary tools, including lowering the banking reserve requirement ratio (RRR), to restimulate the economy. The RRR is the portion of reserves that banks must keep “in the vault.” By lowering this requirement, banks can do more lending and better support the larger economy. The government is also requesting that banks lower financing costs to smaller companies. Later in the week, most metals markets fell victim to a broad selloff that started in Asian and European equities late Wednesday night. Worries over the newer COVID variants that continue to spread, in addition to slowing economies in Asia, played a part in keeping metals from moving higher. However, news of China cutting the RRR by 50 basis points effective on July 15 led to Friday’s rally. |

|||||

|

Bottom Line: By opening metals reserves, China is attempting to deflate metals prices. However, their stimulus efforts have the potential of creating inflation, as lowering financing costs for borrowers and other monetary stimuli incentivizes producers to obtain lower interest rate loans to rebuild inventories of raw materials. This could potentially drive prices of raw materials and finished goods ever higher. The impact of these competing policies could likely have a marginally impact, as the sales from state metals reserves are only a sliver of production, and loosening lending requirements to smaller firms can only do so much to stimulate demand. To remain strong and create lasting demand, China’s manufacturing sector needs more than just the ability to source cheap metal, they need China’s consumer base needs to remain strong too. On the macro front, further strength in the dollar could keep a lid on metal prices. A strengthening dollar makes our products more expensive for foreigners to purchase. Exports of finished goods could stall should the dollar strengthen prices beyond the appetite of foreign demand. COVID fears continue to dominate headlines, as the delta variant is creating havoc in Asia and certain areas of the US. Any ramp-up in delta variant shutdowns could slow the demand for base metals. We continue to recommend that metal consumers layer in hedges in a disciplined manner and select between swaps or call options depending on their risk-management objectives. However, option structures are generally preferred due to the recent rise in volatility. Call options premiums have increased during this rally, so collars (selling put options to offset the cost of call options) are a logical strategy. We also suggest using limit orders along with reasonable stop-loss targets to add incremental protection if prices trend higher.

|

|||||

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

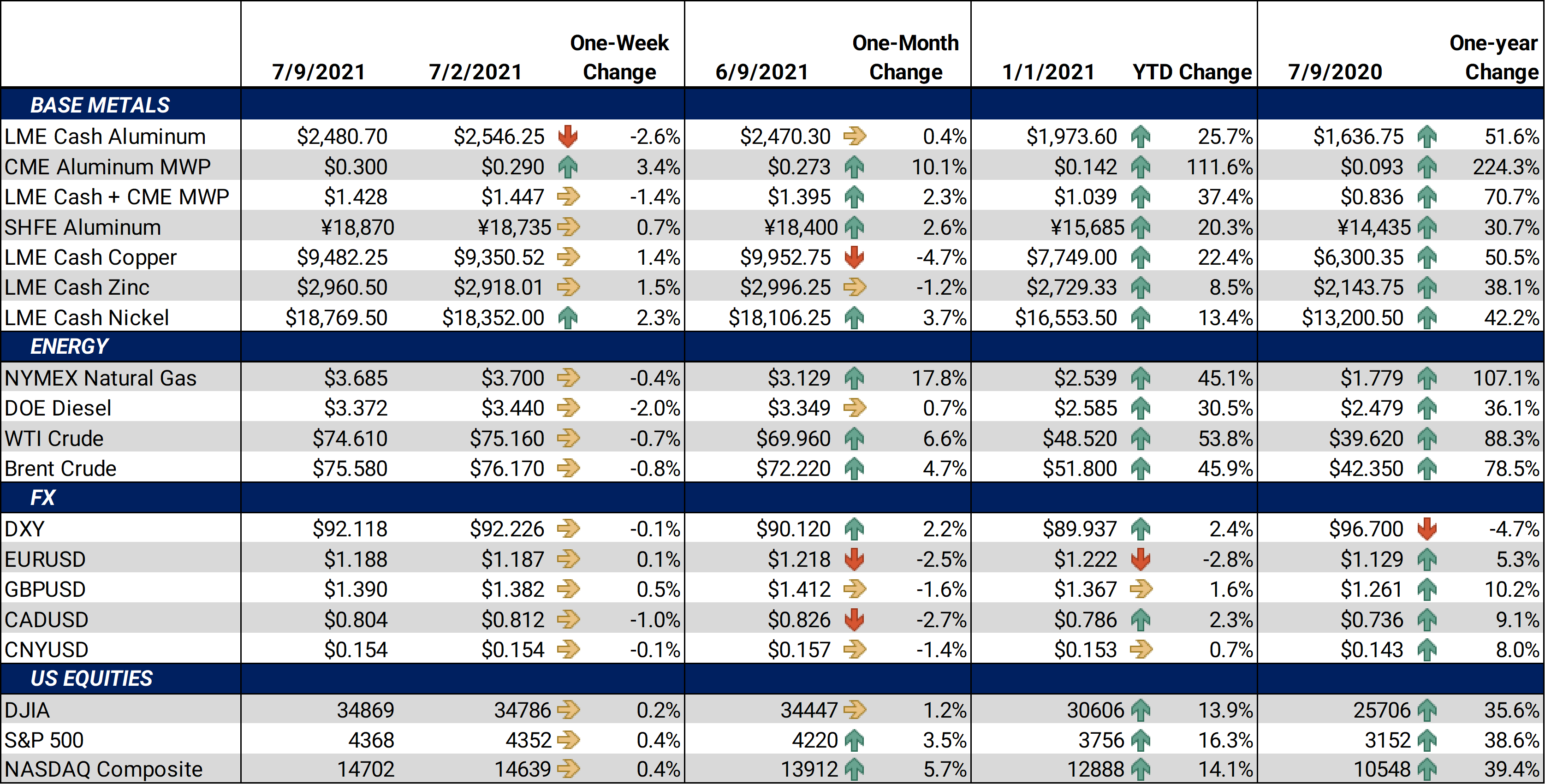

Despite the continued strength in MW Premium, the LME 3M Select finished lower for the week, with last trade at $2493.00/mt, and trade ranging from $2432.00/mt to $2581.50/mt. Chartists would note that this week’s trade created a bearish engulfing candle (meaning this week’s bearish move “engulfed” last week’s smaller bullish move), suggesting more downside potential. Demand was positive at this Monday’s auction by China’s State Reserve Bureau. However, prices were approximately a 5% discount to the Shanghai futures settlement that day. Cash-3M last traded at $21.80/mt contango (where cash is cheaper than 3M), widening from $15.75/mt during last week’s trade. Farther down the curve, Dec ‘21/Dec ‘22 continued to show backwardation, suggesting that there are still few buyers for long-dated contracts. In general, we have seen less long-dated consumer hedging with both premiums and LME at high levels.

|

|||||

Midwest Premium |

|||||

|

The aluminum MW US Transaction premium continued its push higher this week as the CME MWP contract for July had a last trade of 29.75¢/lb at the time of this writing, up nearly 0.55¢/lb for the week. The market grapples with the Russian export tariffs that begin on August 1. American and European end-users are scrambling to source aluminum before tariffs go into effect. Likewise, high freight costs, and shipping delays, are also adding fuel to the fire. There is some chatter that this rally is unsustainable; however, we have heard those thoughts throughout this rally. This premium has nearly tripled since June 2020. Who cries uncle first, the processor or the consumer? Mimicking the activity we have seen over the past several weeks, there was little MWP trading activity in Cal ‘22; the backwardation in the forward curve remains significant and makes inventory hedging expensive. |

|||||

|

|

|||||

LME Copper |

|||||

|

LME Copper 3M Select traded sideways this week, with last trade at $9493.00/mt. The LME 3M contract traded in a slightly larger range than last week, from $9,268.00/mt to $9,632.50/mt. Chartists will likely view $9,000/mt level as nearby support, which is just beneath the low set during the week of June 21. The much-hyped auctions by China’s State Reserve Bureau launched on Monday, with prices coming in at trade expectations. After Monday’s sale, one anonymous trader reported to Fastmarkets that he purchased copper at 67,700 yuan ($10,473)/mt. This price is a discount of about 1,030 yuan ($159.34)/mt to the July copper contract on the Shanghai Futures Exchange. This same trader reported that the auction started at 61,000 yuan ($9,436.52)/mt, and quickly jumped. In a recent blog post, we commented on the Chilean mine strikes and their potential impact on the copper market. At that time, we viewed it with caution, as non-union replacement workers had been hired as temporary. However, on Friday, July 2, Chilean state copper commission Cochilco, stated that output at the Escondida mine was down 9% in May 2021 compared to May 2020 (as reported by Kitco). Markets were largely unfazed by this news.

|

|||||

|

|

|||||

LME Nickel |

|||||

|

After lackluster trade the past few weeks, nickel finally broke out of the recent range and closed near the highs of the week. Last trade on the LME 3M Select contract was $18,755/mt, with a trade range of $17,930/mt to $18,780/mt for the week. Like other base metals, nickel tends to benefit from industrial demand. However, the dollar’s recent rally and lower trade in copper has kept the price of nickel range bound. New, positive fundamental news will likely need to occur to break nickel out of the narrow range we have seen since late April.

|

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

HRC steel traded in a very tight band this week, as outside markets weighed on the metal. The CME HRC futures contract for July ’21 last traded at $1,791/T, about $2/T higher than last week. Deferred, or longer-dated, contracts through the remainder of the year and into 2022 continue to show signs of backwardation, and there is little reason for this to change in the near term. Opportunities remain open for HRC consumers to hedge future prices below the current spot price. For both producers and those carrying inventory, we continue to believe that buying put options remains the best structure to achieve protection against a major market correction. From a consumer perspective, buying calls can be used to protect against a continued rally. Using options with staggered strike prices allows for participation in a downward price correction. |

|||||

|

|

|||||

|

|

|||||

Notable News |

|||||

|

China's state metals reserves auctioned off in double-quick time Copper production in Chile falls 1% in May - report China's cabinet says it will use RRR cuts to support real economy China frees up $154 billion for banks to underpin economic recovery Sudbury strike, Indonesia lockdown jolt nickel prices China to boost steel scrap usage by 23% in next five years Biden Targets Big Business in Sweeping Executive Order to Spur Competition Job Openings Are at Record Highs. Why Aren’t Unemployed Americans Filling Them? |

|||||