LME Aluminum hit $3,000/mt on Monday; however, the rally was short lived as the metal finished lower for the day. Most base metals started the week with a bearish tone after reports of China’s renewed crackdowns on its tech sector. Additional reports that one of China’s largest real estate developers, Evergrande Group, is headed towards bankruptcy likely weighed on markets. Evergrande is a major end user of HRC steel, so bankruptcy fears may have added to the bearish tone for deferred HRC contracts this week. (Evergrande is nearly in $300 billion in debt and set to default on a bond interest payment next week. Its electric vehicle subsidiary, Evergrande New Energy Vehicle Group, has never produced a vehicle and is nearly bankrupt as well). |

Notable Metals News

The political coup which occurred in Guinea earlier this month has not affected shipments of bauxite ore, according to the company. A spokesperson for Emirates Global Aluminum, which wholly owns Guinea Alumina Corp, stated that production or shipments are continuing as normal. Bauxite, an important ore from which aluminum is produced, is a major export of Guinea.

Chinese authorities have further tightened electricity-consumption restrictions on aluminum production regions, which has slowed production. According to Reuters, authorities have told smelters in the Yunnan region to keep production at or lower than August volumes through the remainder of the year. This request also includes those who use hydroelectricity. Aluminum production areas are currently experiencing severe electricity supply crunches, as the country looks to reduce the carbon footprint of metals manufacturing.

Recent data shows how much metals production has dropped in China. Aluminum production in China fell by 3% month-over-month in August, largely due to electricity restrictions. Similarly, steel production fell 10.1% year-over-year in August. This coincides with a recent drop in iron ore demand and lower imports from Australia.

In the US, the automobile industry continues to see fallout from the worldwide semiconductor shortage. Last Friday, Toyota announced it will be cutting worldwide production by 40% in October. This is in addition to the 40% cut they implemented during September.

Notable Economic Data

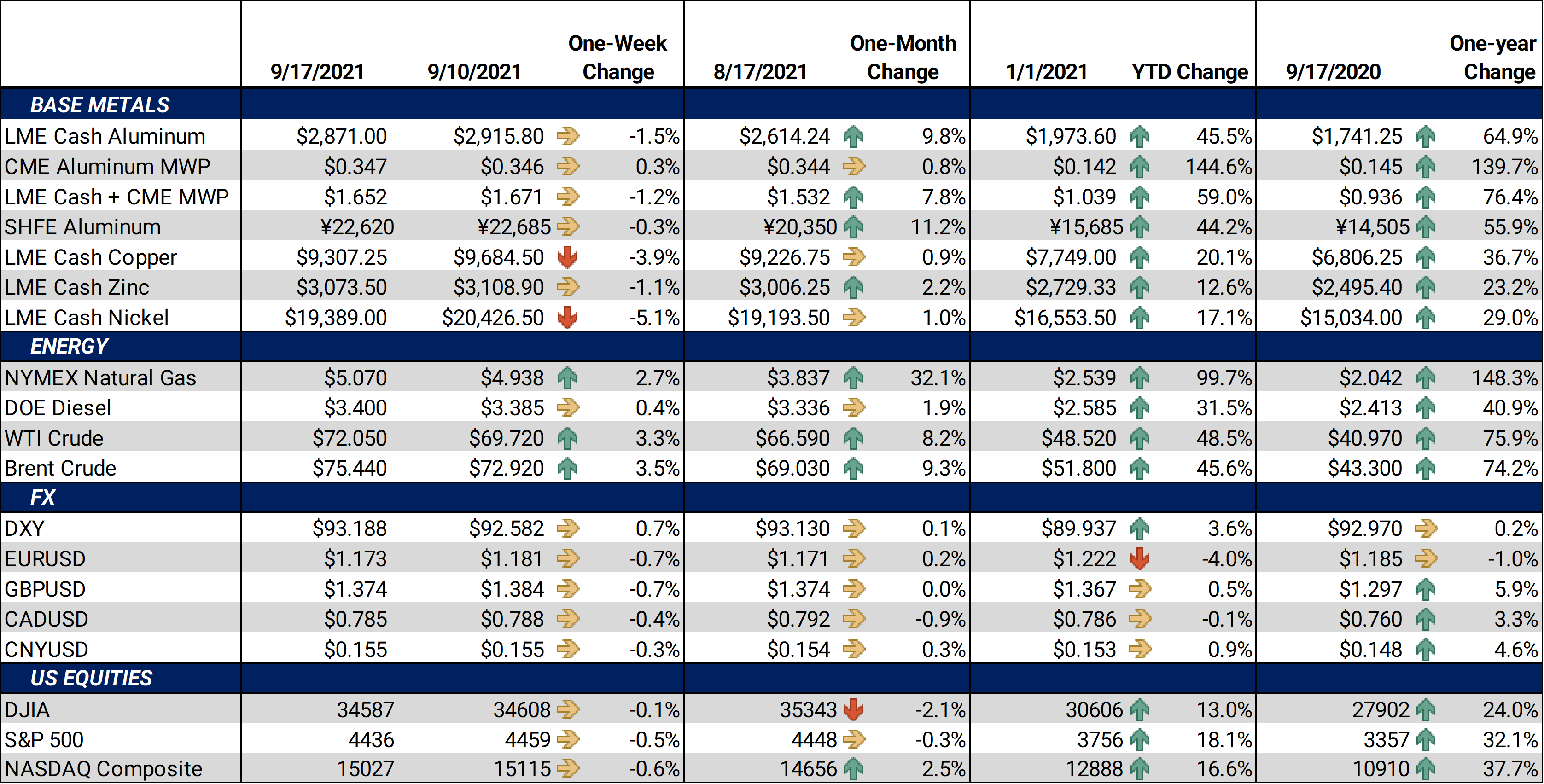

This week’s Chinese economic indicators were bearish. Year-over-year industrial production was up 5.3%, lower than the 5.8% analysts’ estimate. Likewise, year-over-year retail sales were up 2.5%, lower than the 7.0% analysts’ estimate.

This week’s US economic indicators were mixed. Year-over-year CPI was up 5.3%, matching analysts’ median estimates. Month-over-month PPI was up 0.3%, slightly lower than the 0.4% analysts’ estimate. Month-over-month industrial production was up 0.4%, matching analysts’ estimates.

| Bottom Line: | |||||

|

Base metals largely fell this week likely from jitters related to China’s economy, continued crackdowns on its tech and other sectors, and a possible Evergrande bankruptcy. Likewise, production cuts in the automobile sector both here and abroad may have aided the selloff in deferred HRC steel futures. Ongoing issues such as worldwide logistics upsets and sky-high freight and container costs, could keep supporting metals prices. We continue to recommend that metal consumers layer in hedges in a disciplined manner and select between swaps or call options depending on their risk-management objectives. Option structures are generally preferred due to the recent rise in volatility. However, call options premiums have increased during this rally, so collars (selling put options to offset the cost of call options) are a logical strategy. We also suggest using limit orders along with reasonable stop-loss targets to add incremental protection if prices trend higher. |

|||||

|

|

|||||

LME Aluminum |

|||||

|

This week’s aluminum trade set new highs for 2021. The last trade on the LME 3M Select was $2,874/mt, with trade ranging from $2,824/mt to $3,000/mt. Cash-3M last traded at a $13.50/mt contango (where cash is lower than 3M), widening from last week’s trade of $8.20/mt contango. The forward curve has been quite volatile recently, as it has had an over $35 swing from backwardation to contango since August 27. Short-term consumer hedges could be affected, so contact AEGIS to discuss the details. Farther down the curve, Dec 2021/Dec 2022 continued to show backwardation, so the longer-term consumer hedge discount is still available. |

|||||

|

|||||

|

The CME MWP contract for September 21 had a last settlement of 34.675¢/lb at time of this writing. Little “new” news has occurred in recent weeks, thus “old” news such as sky-high freight costs, lack of trucking and steady demand is keeping the MWP elevated. Similar to the past several weeks, there was little MWP trading activity in Cal ‘22; the backwardation in the forward curve remains significant and makes inventory hedging expensive. |

|||||

|

|

|||||

|

|||||

|

Last trade for the LME 3M Select was $9,267/mt, and trade ranging from $9,253/mt to $9,755/mt. From a chartists’ perspective, resistance is now the late-July high trade of $9,924/mt. This week was the weakest LME copper has had in nearly a month. Copper could be taking cues from Chinese economic health and certain companies in the Chinese real estate sector. Copper has largely traded sideways since late-July, with little conviction in either direction. Perhaps a new catalyst is needed to break out of the recent range.

|

|||||

|

|

|||||

|

|||||

|

Nickel had an ugly week, coughing up two weeks of gains. Last trade on the LME 3M Select contract was $19,355/mt, with a trade range of $19,195/mt to $20,475/mt for the week. |

|||||

|

|

|||||

|

|

|||||

|

|||||

|

HRC steel futures were mixed this week. As of this writing, the CME HRC futures contract for September ‘21 last traded at $1,927/T, up $7 for the week. Trade range was from $1,1915/T to $1,934/T. Deferred, or longer-dated, contracts through the remainder of the year and into 2022 continue to be backwardated. Opportunities remain open for HRC consumers to hedge future prices below the current spot price. For both producers and those carrying inventory, zero or low cost collars or swaps are currently the best structure to achieve protection against a major market correction. |

|||||

|

|

|||||

|

|

|||||

Notable News |

|||||

|

Electric-car crash is double pain for Evergrande METALS-Soaring aluminium hits $3,000 for first time since 2008 Toyota, Nissan to stockpile chips in face of global shortage EU to suspend planned tariffs on Chinese aluminum, lobby group says Guinea Coup Strains China’s Supply Chains, Tests Non-Interference Policy Xi Jinping’s crackdown on everything is remaking Chinese society Why Australia should be worried about China Evergrande’s fate Home: Shanghai squeeze revitalises flagging nickel market

|

|||||