Bottom Line:** Please note that the LME will be closed on Monday, May 2. AEGIS will not produce a First Look that morning. ** Total world zinc supplies could fall into deficit this year and drive prices higher, as Glencore expects their production to drop by approximately 107,800 mt, from 1.1178 million mt in 2021 to 1.01 million mt this year, according to their First Quarter 2022 Production Report released yesterday. The International Lead and Zinc Study Group, a UN-founded trade organization, now predicts a global supply deficit of 292,000 metric tons in 2022, according to a press release from this morning. Glencore cites “persistent challenges in ramping up processing capabilities at Kazzinc’s Zhairem operation” for the drop in zinc production.

|

Notable Metals News

Earlier this week, Russia’s Nornickel, the world's largest refined nickel producer, asserted that their operations were “uninterrupted” by Russia-Ukraine conflict. The company made 52,000 mt of the metal in Q1 2022, up 10% year-over-year, according to a company press release. Regarding the Ukrainian conflict, the company stated, “In spite of certain challenges in logistics and deliveries of equipment, spares and consumables, due to geopolitical situation, our operations remain uninterrupted. Currently, we are using new logistical arrangements and exploring opportunities with alternative suppliers.” The company says production increases at the Oktyabrsky and Taimyrsky mines, and ramp-up of the Norilsk Concentrator led to higher refined-nickel output.

Global steel production has dropped in recent months. Chinese steel production led global production lower last quarter, as the country produced 243.5 million mt, down 10.5% year-over-year, according to the World Steel Association. Total global steel output fell by 6.8% to 456.6 million mt, compared to Q1 2021. Of the top 10 steel nations, only India had a production increase, making 31.9 million mt, up 5.9% compared to Q1 2021. The supply decrease coincided with a rallying steel market; for example, May CME HRC futures are up nearly 45% from the January lows. US production was down a mere 0.4%, as we produced 20.3 million mt last quarter.

Continuing on steel, the EU could end tariffs on Ukraine steel, per a proposal being considered, according to Reuters. This could encourage President Joe Biden to end the current 25% Section 232 tariff on Ukrainian steel, Fortune magazine proclaimed hours after the EU announcement. Earlier this month, US Senators Dianne Fienstein and Pat Toomey penned a letter to Biden urging him to do so, stating, “Lifting the U.S. tariff on steel from Ukraine is a small but meaningful way for the U.S. to signal support for Ukraine and to provide stability and improve the country’s long-term economic outlook." The current tariff was set in 2018 as part of the Section 232 tariffs that sought to reduce the flow of metals imports, thereby preventing foreign exporters from dumping cheap steel onto the US market. The US imported 127,853 mt of Ukrainian steel in 2021, down from a pre-Section 232 volume of 240,730 mt in 2017.

Finally, to compete with the LME, the CME will launch aluminum options on May 23, pending regulatory approval, according to their press release yesterday. The option contract will be a derivative of the current physically-delivered CME aluminum futures. In the press release, CME Group’s Global Head of Metals, Jin Chang, states, “Our new option contract is the latest example of CME Group's decade-long track record of helping the aluminum community to manage risk as their needs evolve,” adding “a record 4,888 Aluminum futures contracts traded on April 19 and average daily volume in April currently around 1,300 contracts, up over 100% from last year.” The CME introduced its aluminum futures in 2014.

If these options gain popularity, they could be another risk-mitigation tool to aluminum consumers to set upper limits on their aluminum input costs. LME aluminum options already exist, with good liquidity. The CME version's slightly different specifications may make them a better tool in specific situations.

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

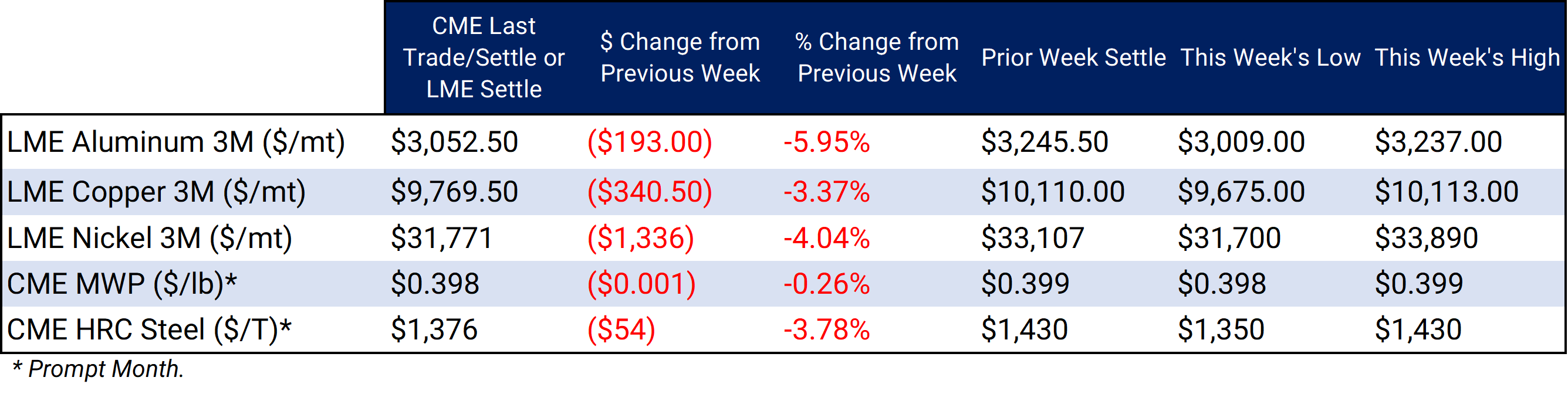

LME Aluminum 3M settled at $3,052.50/mt, down $193/mt on the week. The forward curve for LME Aluminum is currently quite backwardated, meaning that spot prices are higher than futures prices. A backwardated forward curve favors the consumer hedger. The aluminum market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 39.821¢/lb this week. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this market is tricky, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $9,769.50/mt, down $340.50/mt on the week. The forward curve for LME Copper is currently quite backwardated, meaning that spot prices are higher than futures prices. A backwardated forward curve favors the consumer hedger. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $31,771/mt, down $1,336/mt on the week. Like LME copper and aluminum, the forward curve for LME Nickel is currently backwardated, meaning that spot prices are higher than futures prices. A backwardated forward curve favors the consumer hedger. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded at $1,376/T, down $54/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with strategically placed limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

04/27/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 04/21/2022: Russian Metals Production and Related News: Most Recent Developments (AEGIS Reference) |

|||||

Notable News |

|||||

|

4/28/2022: Glencore cuts output guidance for copper, zinc, cobalt 4/27/2022: EU to suspend tariffs on Ukraine imports for one year 4/27/2022: Peru govt declares state of emergency near MMG’s Las Bambas mine as stand-off continues 4/26/2022: CME Group to Launch an Aluminum Option Contract on May 23 4/25/2022: Column: Bears tip-toe back into copper market as demand fears grow 4/24/2022: Indian aluminium producer NALCO faces coal scarcity due to train shortage 4/22/2022: March 2022 crude steel production |

|||||