|

Aluminum Investment funds, which are purely speculators in metals markets, have dramatically reduced their long position in LME aluminum. As of last Friday, these funds are net long approximately 3,960 contracts, down from over 23,200 in early October. Given that investment funds can greatly influence aluminum prices, this is likely why prices have trended sideways to lower in recent weeks. (Source: LME) |

|

|

Aluminum prices are trying to stabilize due to anticipated supply shortfalls next year, influenced by production constraints in China, the world's largest producer. Goldman Sachs forecasts a global aluminum shortage of 1.23 million tons in 2024, almost double the deficit of 2023, and expects the metal's price to reach $2,600/mt in the next 12 months. This is mainly due to power shortages in China and capacity limits on smelters. (Source: Bloomberg) Like Goldman Sachs, UBS also expects an aluminum shortfall, but not as severe as Goldman’s predictions. According to UBS, the aluminum market is anticipated to be nearly balanced in 2024 but is leaning towards minor shortages. This situation could lead to higher aluminum prices later in the year. The global refined aluminum supply is projected to grow modestly by 2.2% in 2023 and 2.7% in 2024. In 2023, the aluminum market is expected to shift from a previously forecasted shortage of 484,000 metric tons to a surplus of 89,000 metric tons. However, in 2024, the market is expected to experience a slight shortage of 7,000 metric tons, contrasting with the earlier expectation of a surplus of 385,000 metric tons. (Source: Bloomberg) Norsk Hydro, one of Europe’s top aluminum producers, is “shifting gears” while “stepping up growth ambitions in extrusions, recycling, and renewable power generation aimed at capturing market opportunities emerging from the green transition,” the company stated at its Capital Markets Day earlier this week. Hydro will also aim to cut costs and raise profit targets despite increasing capital expenditure. The company estimates that by 2030, aluminum demand for EVs, electrical grids, and solar panels will increase by a total of 15 million mt. (Source: Reuters) |

|

Copper Unlike aluminum, investment funds continue to add to their long position in LME Copper. As of last Friday, funds are net long approximately 8,633 contracts, compared to a net short position of over 15,000 contracts in late October. The prior position was their largest net short position since the early days of the pandemic. Given that the copper market is extremely price-sensitive to fund positioning, an increasing long position (if it occurs) could be bullish for LME copper prices. (Source: LME) Panama's Supreme Court has unanimously ruled that First Quantum Minerals Ltd.’s mining contract is unconstitutional, creating uncertainty over the future of the major global copper producer. The ruling follows mass protests and operational disruptions at the mine. This decision, coupled with ongoing protests and potential fiscal impacts on Panama, heightens the challenges for First Quantum and the Panamanian government in resolving the dispute. The mine, known as Cobre Panama, is responsible for about 1.5% of global production. (Source: Bloomberg) Like Panama, other major copper-producing countries are experiencing issues as well. Union workers at MMG’s Las Bambas copper mine in Peru ended a two-day strike on Thursday, the union announced Wednesday. The strike, which was initially going to be indefinite, was cut short as government authorities decided that an indefinite strike was prohibited. The union could potentially strike again, though, if bonuses are not paid. The Las Bambas copper mine is one of the world’s largest, responsible for approximately 2% of global production. (Source: Bloomberg) |

|

Steel Steel prices have rallied recently, supported by low inventories throughout the supply chain. Yet recession worries should leave North American steel demand flat in 1H, with a pickup possible in 2H24 if there's a soft landing. Customers of Nucor, US Steel, and other steelmakers are exhibiting buying restraint amid recession risks and mixed end-market demand. Increased infrastructure spending will likely mitigate a downturn in residential construction, while automotive production will depend on pent-up demand overcoming higher interest rates and reduced affordability. (Source: Bloomberg) The Biden administration is engaged in a trade standoff with the European Union over steel tariffs, a holdover from the previous administration. The dispute centers around a 2021 agreement on steel and aluminum tariffs that may expire soon, potentially reigniting trade tensions. Despite initial intentions to reverse prior tariff policies, the Biden administration has largely kept these tariffs in place. The current situation with the EU involves negotiations over tariff rate quotas, which set limits on tariff-free steel and aluminum imports and reflect ongoing trade policy challenges. (Source: Bloomberg) Moving onto China, the country’s steel industry may gradually recover in 2024, with improving credit conditions and property sector support potentially boosting demand and prices. Despite lower net exports, a projected utilization rate of around 89% could elevate prices to 4,100-4,300 yuan per metric ton. Crude steel production in China is expected to grow modestly by 1-2% in 2024, with domestic demand increasing similarly, offsetting property-sector declines and challenging import barriers in other regions. After significant destocking in 2023, a limited appetite for further inventory reduction could lead to a 3% rise in apparent demand. (Source: Bloomberg) As for raw materials, China’s National Development and Reform Commission (NDRC) has vowed to clamp down on surging iron ore prices, which have climbed steadily since late October. According to Bloomberg Intelligence, “NDRC warnings have the potential to take the froth out of the market, but they won’t be able to alter the fundamentals which have improved.” A recent report from Chinese researcher Mysteel showed that real estate transactions are rising. (Source: Bloomberg) Japan-based Nippon Steel, the world's fourth-largest steelmaker, is seeking out more coking coal and iron ore assets, a senior VP announced earlier this week. These ambitions are mainly to control its supply of raw materials and mitigate price volatility. In November, the company announced it was taking a 20% stake in Teck Resources’ coking coal business. "Coking coal prices are expected to rise as supply will get tighter in the medium term as there has been little investment in mines due to carbon-neutral push…. "So, it's extremely important to secure our own interests," executive vice president Takahiro Mori proclaimed earlier this week. (Source: Reuters) |

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

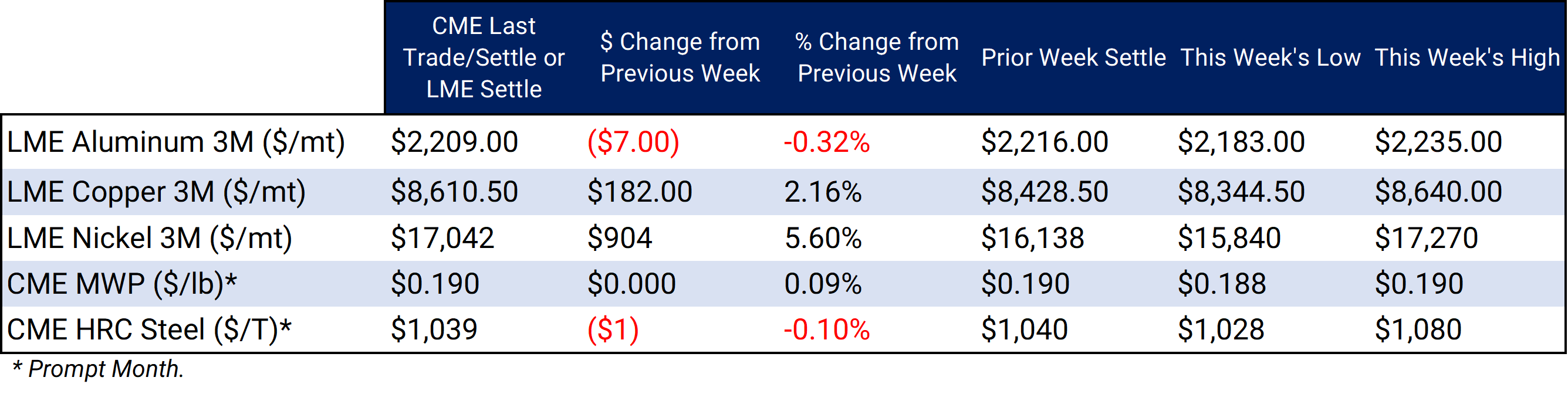

LME Aluminum 3M settled at $2,209/mt, down $7/mt on the week. Aluminum prices were down this week. This has caused the futures forward curve to shift vertically lower by approximately $10/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 19.0¢/lb this week. The CME Midwest Premium market is now in a contango from the December ‘23 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,610.5/mt, up $182/mt on the week. Compared to last Friday, LME Copper's forward curve has risen vertically by approximately $180/mt and remains in contango for the remainder of 2023 and throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $17,042/mt, up $904/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $900/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $1,039/T, down $1/T on the week. Steel mill profit margins have improved dramatically in Q3 and Q4. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $610/st, up from about $320/st on September 1. This is mainly due to prompt month CME HRC steel futures rallying alongside prices in the physical market. Since steel prices have increased significantly recently, mills should consider hedging production and raw material usage for late 2023 and early 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

11/30/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 11/17/2023: Aluminum and Copper End-Users Should Hedge As Inflation Eases 10/17/2023: Important US Economic Data (AEGIS Reference) 09/28/2023: Aluminum Buyers Should Hedge Alongside Chinese Importers |

|||||

Notable News |

|||||

|

11/29/2023: Nippon Steel to hunt for more coking coal, iron ore assets-executive 11/29/2023: UK car production expected to hit 1 million in 2023 - industry body 11/29/2023: Aluminium maker Hydro ups profit goals, sees higher capex 11/29/2023: India's April-Oct steel imports from China at four-year high 11/28/2023: Panama president directs First Quantum to shut copper mine after court ruling |

|||||