Friday marked the last day of trading for June Canadian crude differentials. WCS diffs widened out just over $2.00 USD/Bbl from May to settle at ($12.89) USD/Bbl for June barrels. MSW diffs followed suit settling at ($3.89) USD/Bbl for June, $0.78 USD/Bbl weaker than May.

Canadian crude inventories remain sky high. Wood Mackenzie data shows that Alberta has continued to add barrels over the last month and is now nearing 38MM Bbls. While there is not a single piece of data that is more glaring than others, lower takeaway on pipelines and rail is one culprit. A decrease in refinery demand and continued upgrader maintenance in Western Canada is another.

Planned and unplanned outages in the US Midcontinent and Eastern Canada have led to decreased pipe flows. Alberta upgrader turnarounds are now expected to stretch long into the summer as Covid -19 outbreaks have caused delays. These delays equate to lower demand on the bitumen side, and lower production on the synthetic side.

Western Canadian refinery inputs have declined over the last month with Imperial’s 189,000 bpd Strathcona refinery and Suncor’s 142,150 bpd Edmonton refinery still in planned refinery turnarounds. All told, it has been a very heavy turnaround season for the areas that call on Canadian crude.

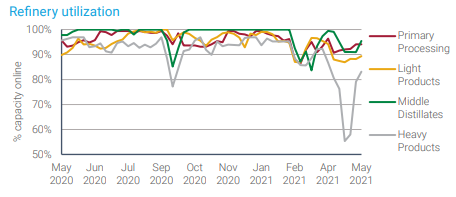

| Enough talk about declines! There has been a significant uptick in Midwest refinery utilization for those that utilize heavies in their crude slate. Early pipeline data is already starting to reflect this increased demand beginning with June apportionment on the Enbridge line. June heavy barrels were apportioned at a whopping 52% vs 43% in May. Exxon’s Joliet is expected to fully come back online this week and should be back to full capacity by June. The refinery handles 250,000 bpd (primarily Canadian crude) and experienced a full plant turnaround starting in early March. |

Source: Wood Mackenzie |

|

Source: Wood Mackenzie |

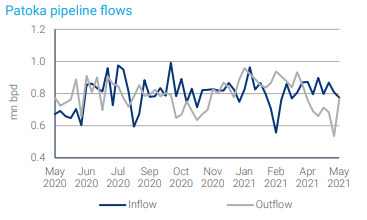

Looking further South, PADD 2 ex-Cushing inventories have shown a notable increase – almost 7 MM bbls since early April. Patoka inventories in particular are notable. DAPL volumes into Patoka have been steady over the past month, but there has been a material decline in flows from Patoka to the USGC (on ETCOP). This crude has had to flow into storage contributing to the rise in inventory. |

Increased refinery runs coupled with general increased summer demand should help alleviate the storage pressure, but we are on a razor’s edge here. Any surprise events that cause more crude bottlenecks will widen regional differentials, which can ultimately ripple all the way back to Canada.