- The forward curve has weakened into a contango structure from late 2026 through at least 2030 (Bloomberg)

- Traders are re-pricing the long-term outlook to reflect expectations of a future oil surplus

- On Friday, more than 450,000 Brent crude options traded — more than double the previous record

- Activity was dominated by bearish positioning, signaling heightened downside hedging

- On Monday, bearish Brent contracts traded at their largest premium to bullish calls since late 2021

- Implied volatility jumped to its highest level in months, reflecting elevated market uncertainty

- The recent pullback has pressured longer-dated futures as supply-demand fundamentals appear looser

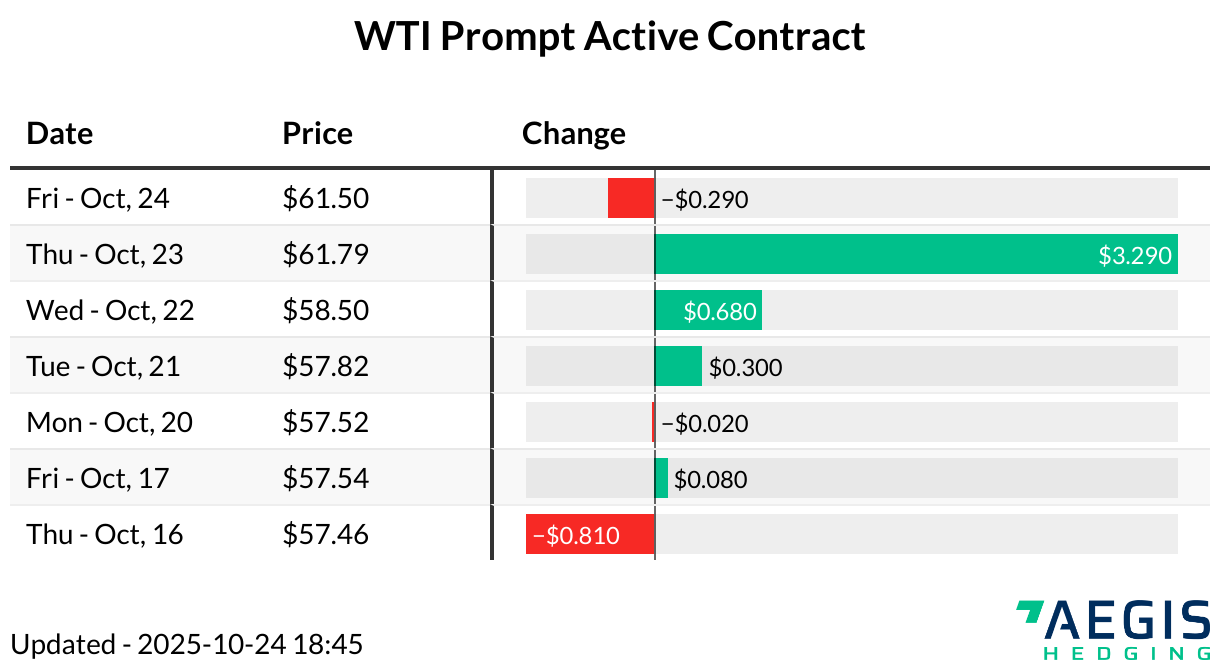

- The 2026 WTI strip settled at its lowest since late 2021

- The spread between the nearest two December WTI contracts fell to -13c on Monday

- This is the first time it has been at a discount since late 2020, it serves as a key gauge for hedge funds tracking long-term balances

- • The WTI prompt-month contract is up 53c to $61.23/Bbl (7:45 AM CT), though sentiment turns cautious amid mounting recession concerns

- Societe Generale sees WTI ending the year at $57/Bbl

- Goldman Sachs warns Brent could fall below $40/Bbl in an “extreme” downside case involving a global recession and OPEC+ unwind

- Base case: Brent at $58 this December, $55 next December, assuming a mild US recession and baseline expectations for supply

|

|

|

|

|

|

Looking for interest rate charts? We moved them here |