|

Gas prices have been soaring lately, and there are multiple reasons. The Russia-Ukraine conflict sometimes gets blamed for rising prices in the U.S. – we do not believe this to be the main factor. The main force behind this huge rally is a tight supply-demand balance, where the market is undersupplied, and gas inventories will likely struggle to build up to normal levels by winter. The storage deficit to the five-year average is expanding nearly every week.

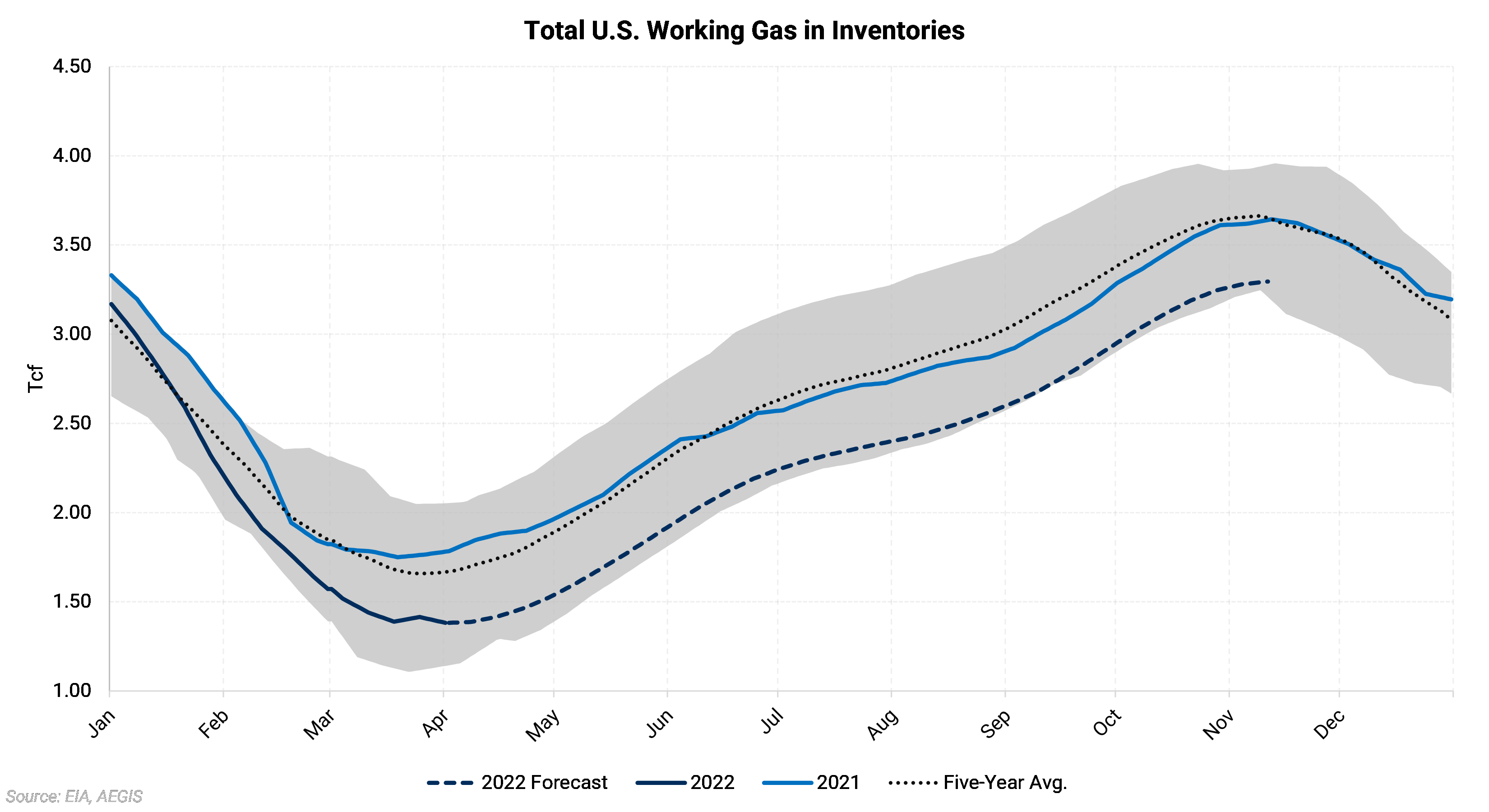

The chart above is our forecast for gas inventories. We arrived at this forecast by solving for the recent supply-demand balance, with an adjustment for weather, and then modeling the injections through the end of the summer by using 20-year average temperatures. This forecast places U.S. working gas inventories at 3,330 Bcf by the end of the injection season, almost 355 Bcf below the five-year average. Further, this is the second-lowest start to winter in the last ten years, behind only 2018, which was at 3.24 Tcf. If this materializes, the market would be much more vulnerable to winter weather and heightened volatility. Adequate inventories are around 3.6-3.8 Tcf, and usually, anything below is viewed as insufficient. The result has been that gas prices have had their hottest start in 2022 than any year on record. That run might not be done. There is serious concern that only high prices will fix the situation. Without cooperative (cooler) weather this summer, there either needs to be some demand destruction or an increase in production. |

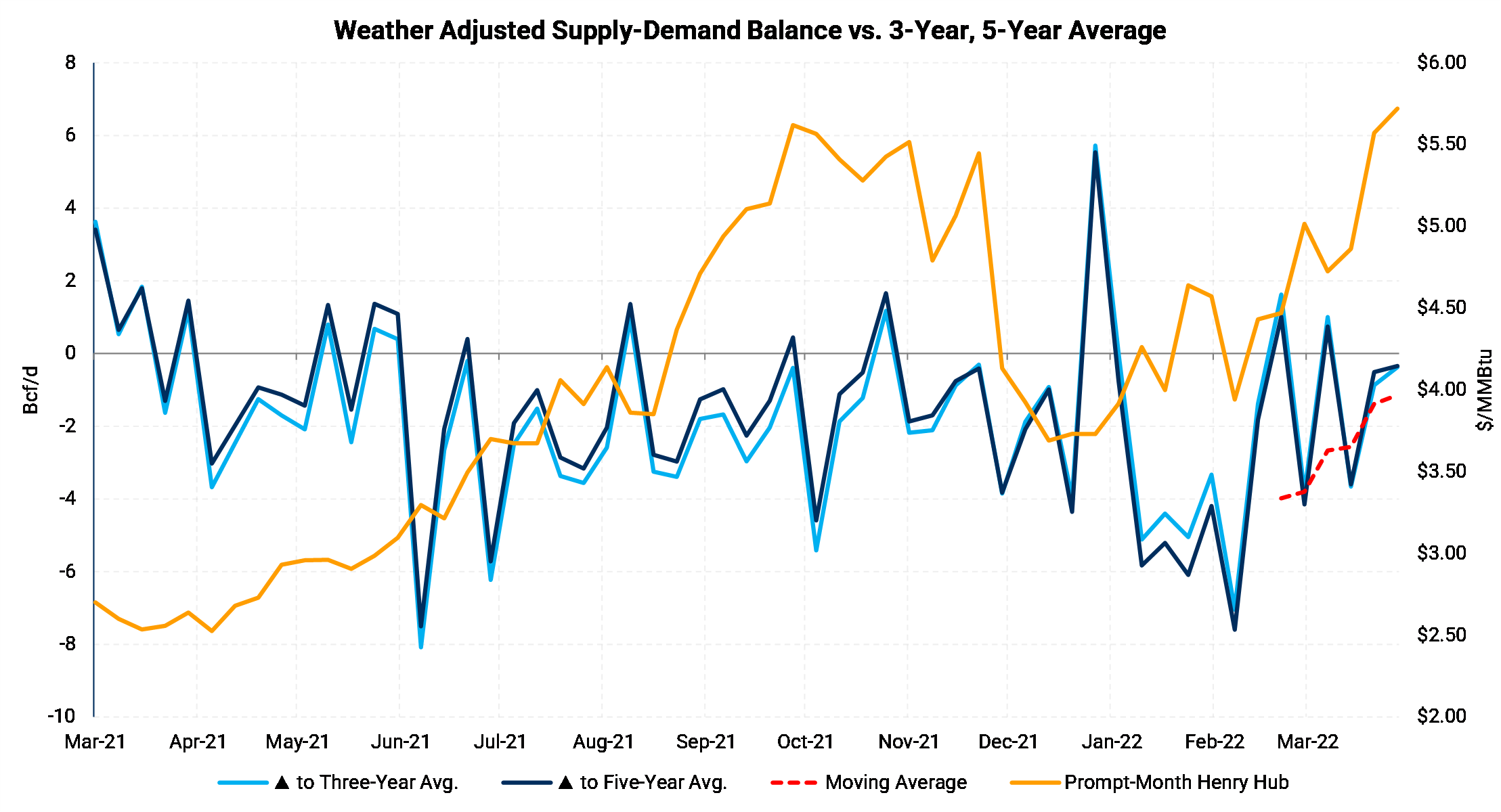

Tight Supply-Demand BalanceGas demand is strongly-tied to weather, and so hotter weather during the summer translates into more gas demand for power for air conditioning, similar to how gas demand for residential and commercial sectors ramps up during periods of cold weather as the fuel is used for home heating. Because of this, the weather needs to be accounted for when modeling gas demand. If we adjust for the effect of weather, the U.S. gas market is still under-supplied by around 1.1 Bcf/d to the five-year average, but what exactly does this mean? Under normal weather conditions, the amount of gas injected into storage would be 1.1 Bcf/d lower than the five-year average, which would mean that the deficit to the five-year average would widen by another 200 Bcf by the time winter arrives. This 1.1 Bcf/d weather-adjusted deficit to the five-year average represents around 0.9 Bcf/d of loosening in the supply-demand balance since last summer.

The chart above is an AEGIS model that shows how much supply needs to rise, or non-weather demand needs to fall, to bring the market back into balance. For most of the year, the supply shortfall has been around 2 Bcf/d. In March 2021, the weather-adjusted supply-demand balance first showed signs of an undersupplied market. This resulted in higher prices in 2021, and the chart shows how the supply-demand balance fared during this time of higher prices. Markets tend to try and fundamentally re-balance themselves via demand destruction from higher prices, as demand is more of a short-term lever, while production tends to take months to respond to periods of high prices.

|

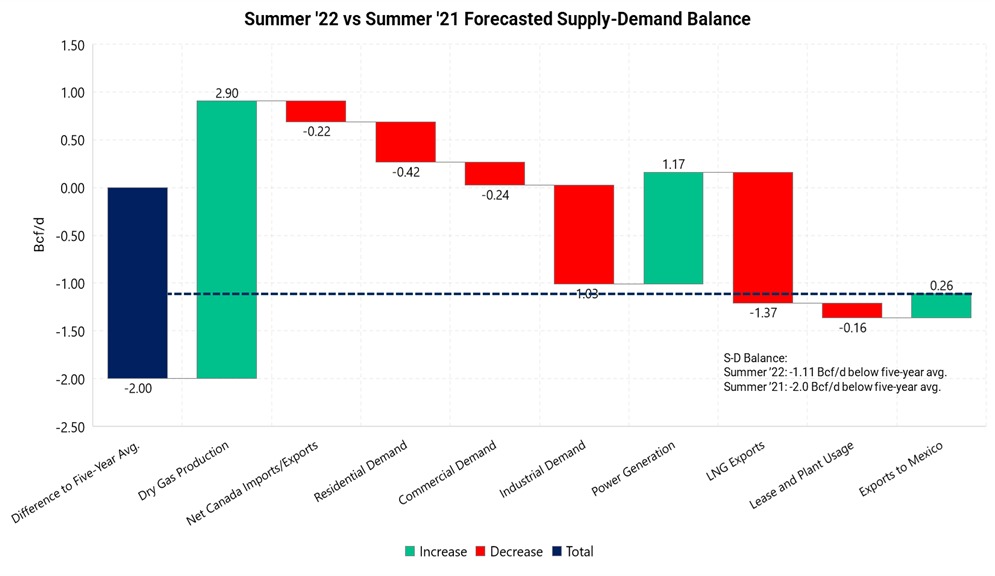

Summer 22 Supply-Demand Balance

The largest change in this year's supply-demand balance from last is dry gas production, which is up by 2.9 Bcf/d year-over-year. While lower-48 dry gas production is still slightly removed from its all-time high, current levels are at 96 Bcf/d. According to the EIA's Short-Term Energy Outlook, dry gas production is forecast to be 2.9 Bcf/d higher this summer compared to last. Natural gas production growth has been struggling lately, after reaching 97.31 Bcf/d in December, but there has been a pickup in drilling and completion activity, which precedes production growth. The EIA is also forecasting lower natural gas-fired power generation this summer, which can be attributed to higher prices and increased power generation by alternative sources, namely coal and renewables. Still, the increases in industrial demand, LNG exports, and residential-commercial demand offset all of the demand lost by the power sector. According to the EIA, power generation will be 1.17 Bcf/d lower year-over-year, while residential-commercial demand, industrial demand, and LNG exports will be up by 0.66 Bcf/d, 1.03 Bcf/d, and 1.37 Bcf/d, respectively. The net impact of the changes in the individual components places the market at around -1.11 Bcf/d under-supplied relative to the five-year average, which is around 0.89 Bcf/d looser than last summer's average of -2 Bcf/d. In conclusion, this market is still under-supplied and needs to loosen if inventory levels are going to rebuild enough to enter winter with adequate inventories.

|

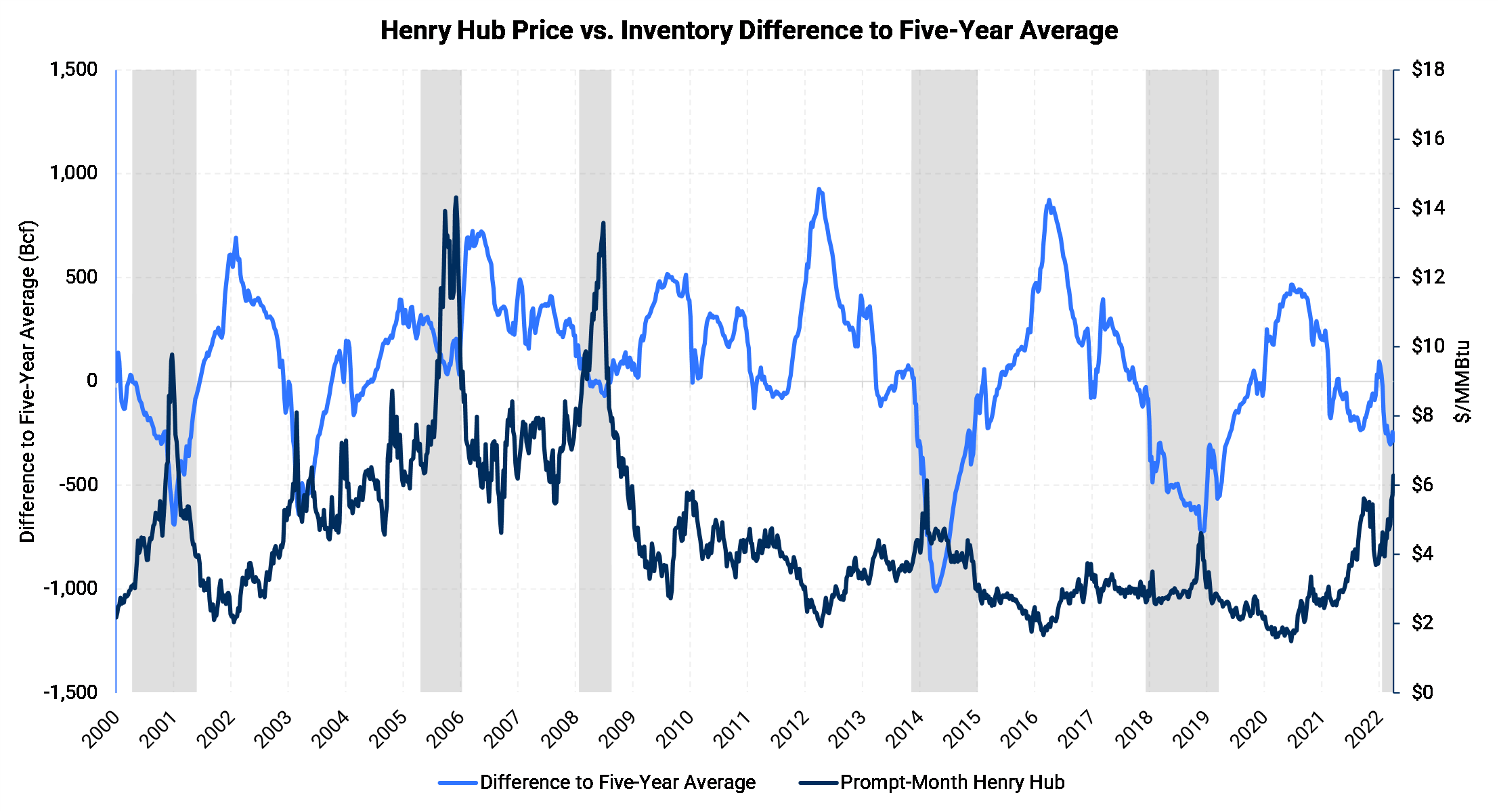

StorageUnderstanding how the supply-demand balance compares to the five-year average is important because of its relationship to prices. In the past, gas prices typically rise when the deficit in inventories to the five-year average is widening, as evidenced by the chart below. The chart shows the difference to the five-year average versus the prompt-month Henry Hub price. The relationship between the two is inverse, and I have highlighted several times in history when the relationship was apparent. Further, the price increase usually does affect either supply/demand, which is how the market rebalances itself and incentivizes storage injections. In January 2022, stocks were briefly at a surplus to the five-year average through the first couple of weeks in January, and prices were falling. However, colder weather finally arrived towards the end of January, and the deficit to the five-year average started to widen rapidly, reaching a low of -304 Bcf on March 11, leading prices to their best start to a year on record. Since March 11, the deficit in inventories to the five-year average has hovered between -250 and -300.

Another important distinction is that although this year's supply-demand balance may be slightly looser than Summer '21, inventories are at a much lower starting point as we enter the injection season. Last year, prices were higher as there were inventory concerns, and this year's setup actually looks much more problematic. In fact, in 2021, inventories were never at a deficit this large, and the last time the deficit was this large was in May 2019. In conclusion, this year's setup looks encouraging for producers but a reason for caution if you are a consumer. We have yet to observe a change in the tight supply-demand balance, and if it holds steady, we could enter winter with much lower inventories than usual. Production remains the largest wild card. If it surprises to the upside, it would be much easier to get more gas into the ground. Only time will tell, but drilling rigs have been ticking higher lately, and several agencies, including the EIA, forecast enough production growth to enter the winter season with adequate inventories.

|