Nymex and Inside FERC gas settlement prices made a rare move on Jan 27; It upset portfolios that had 'incomplete' hedges |

|

|

When markets do unusual things, hedging or trading strategies get stress tested. AEGIS explains how gas basis price settlements caused problems with some hedge books, and the steps to take to mitigate the risk more completely. |

|

|

|

|

|

|

NYMEX Last Day Rally Caused Hedging Losses. What happened? |

|

|

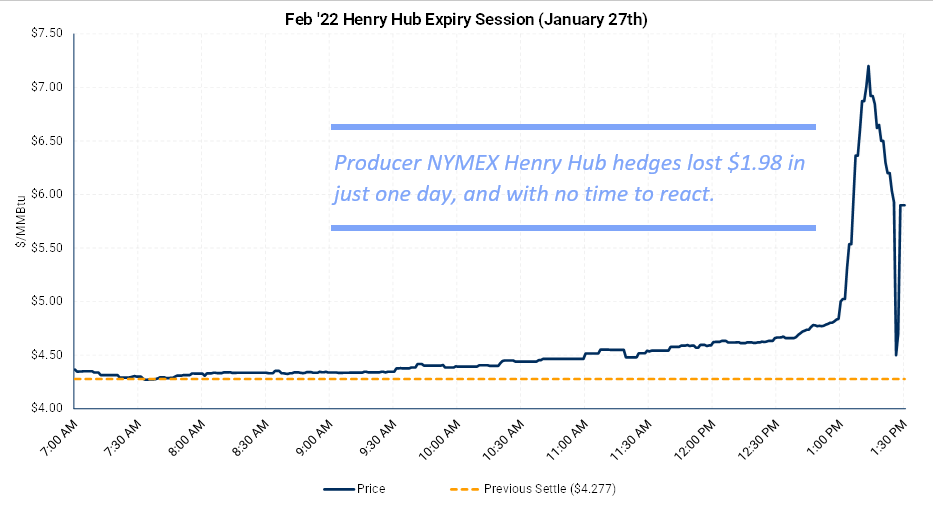

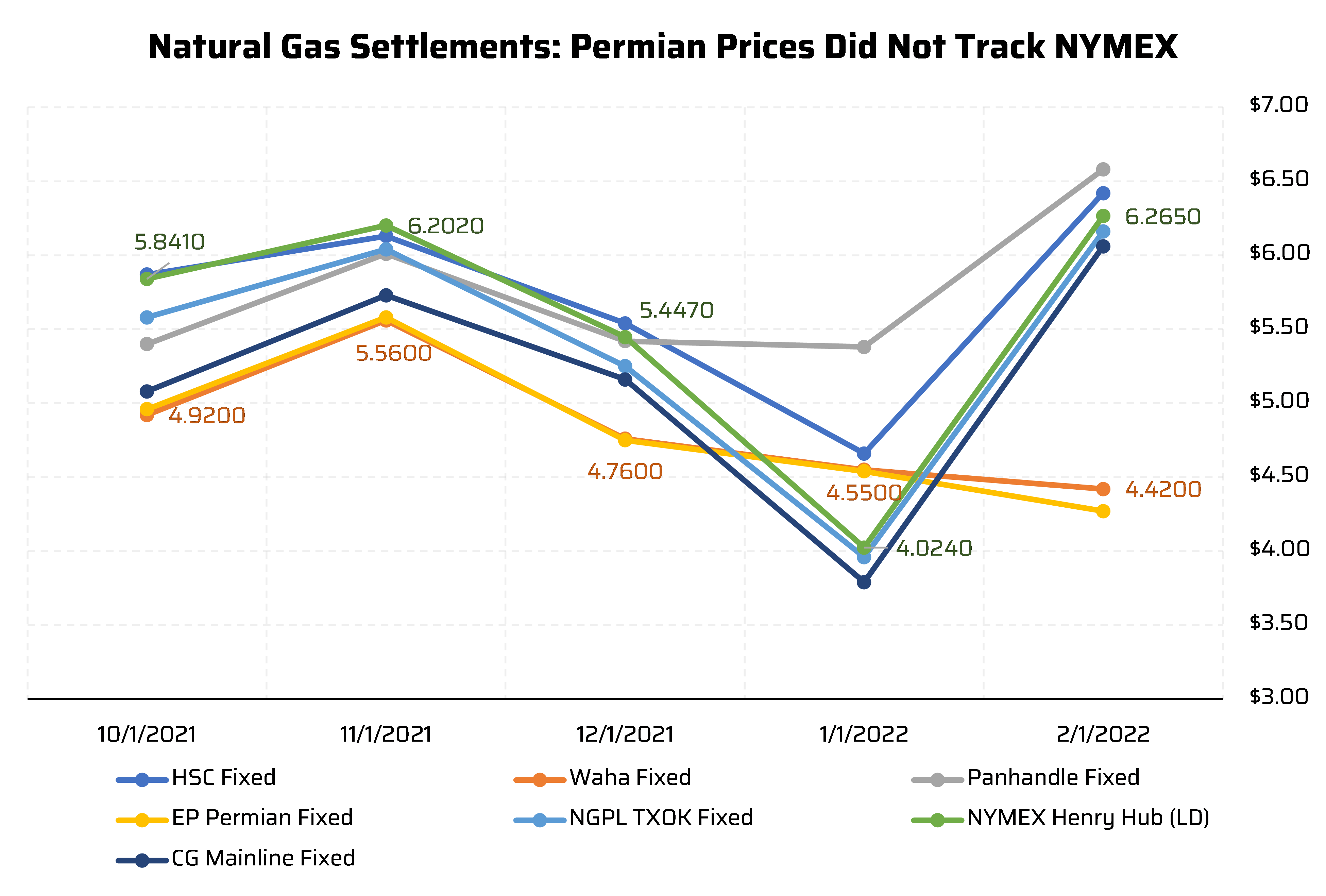

On the very last day of trading for the NYMEX Henry Hub futures and swaps contracts for February, a late-day rally led to a one-day price increase of $1.988/MMBtu. Most of the move was in the last 30 minutes. That price increase translated into the same dollar loss for producers who had used it to hedge their gas price exposure. (That’s not the end of the hedging story, but we’ll get to that) This would be no problem at all, if the gas producer's marketing contracts specified that same NYMEX price for sales in February. They wouldn't be bothered if the hedge contract went up by almost $2. So did their physical sales price received in February. It would be a wash. Unfortunately, most gas producers do not receive a price equivalent to the NYMEX price. Instead, they usually receive a locational price from one of dozens around the country – for example, Waha in the Permian basin, Columbia Gulf Mainline in northern Louisiana, Houston Ship Channel for southern Texas producers, or maybe Colorado Interstate Gas in eastern Colorado and Wyoming. These prices are negotiated by physical gas traders, in a three-day period called "bidweek" just before the month starts, and the average trade price for each location is published by Platts as an “Inside FERC” (IFERC, or IF) price on the first day of the month. The chart below shows that, for many IFERC locations, the price kept up with what happened on the NYMEX. This means that a NYMEX-only hedge worked somewhat. It wasn’t perfect, but it wasn’t disaster. However, the producers in the Permian basin had a much larger problem. The IFERC settlements meant that their gas would be sold at a much lower price in February than the NYMEX had indicated. Let’s study that problem in more detail. |

|

|

|

|

|

The table below shows how a Permian producer who: (1) initially had exposure to future IFERC Waha priced sales; (2) partially hedged with a NYMEX natural gas short, then; (3) added a locational basis hedge for Waha, and; was left with all these floating-price risks mitigated. A note about (3): Waha basis is traded as a differential, rather than a price. We disaggregated the differential into two prices for illustration.

|

|

|

|

|

|

Notice that the NYMEX portion of the Waha basis trade canceled with the NYMEX hedge from (2). The result is a simultaneous long and short position in IFERC Waha. These two offset each other, canceling any floating-price risk, and converting to fixed price. It’s a complete hedge for a producer who receives IFERC Waha for gas produced in the field. It is standard practice at AEGIS to counsel our clients to hedge in this manner, to match hedges completely to the cash price received.

|

|

If You Only Follow One Rule, Make It This One |

|

|

Match your hedges to your physical, cash-price exposure. Maybe you faced this problem in February, where losses on NYMEX hedges caused you to write a big check to the bank, but you will not receive an equivalently higher cash price for your gas during February. The problem arose from a lack of a basis hedge. Let’s revisit the table and see what is missing.

|

|

|

|

|

|

Without a basis hedge in place, the NYMEX hedge only provides partial protection for the IFERC Waha sales. This practice has a very poor track record. Not only did this tactic not work for February, it has been notoriously ineffective in the past, under what could be called “normal” circumstances. The main reason, in our view, is because the Permian basin is prone to pipe congestion and troubles with egress. The AEGIS recommendation to almost everyone is to find precisely the price location and volumes you plan to sell. Then, have AEGIS match the correct hedging contract to your physical, cash-price exposure.

|

|

Easier Said Than Done? AEGIS Platform Tools Make It Simple and Automatic |

|

|

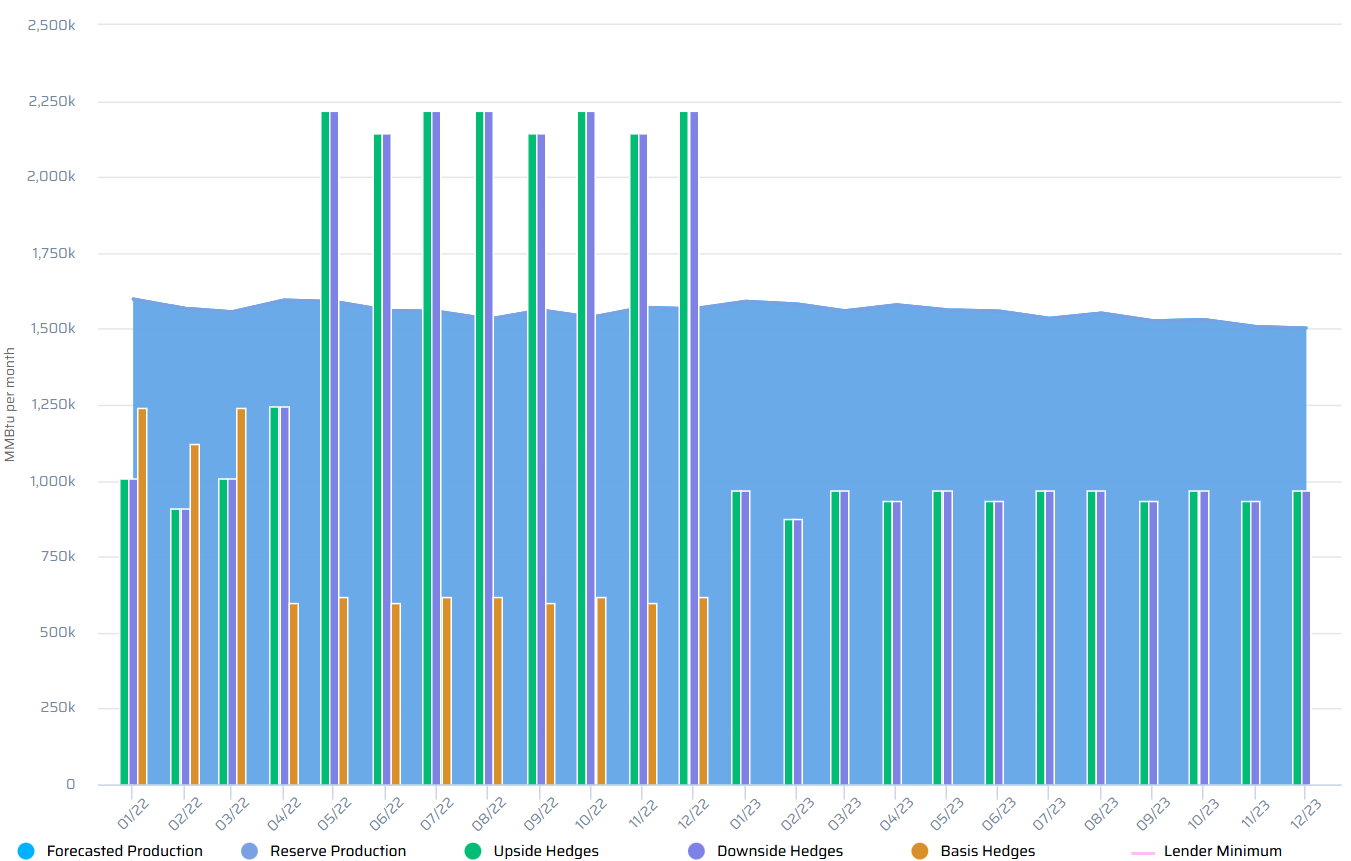

The root of the issue many faced in February is not having enough basis hedges to “complete” the regional price hedge. One easy tool to check for this risk is on the AEGIS online platform. Our platform aggregates your production expectations, all your existing hedges, and your goals and constraints. One particular chart shows how AEGIS clients can check for inadequate basis hedges. The image below shows how this gas producer does have some hedges (see “downside hedges”) for protection, but the “basis hedges” have not been added in equal number. Compare the purple series with the orange series: |

|

|

|

|

|

|

|

|

This problem (among others, as you might notice) can be quickly identified and measured. The AEGIS trading desk can assist in the execution of any hedges with your counterparties. |

|