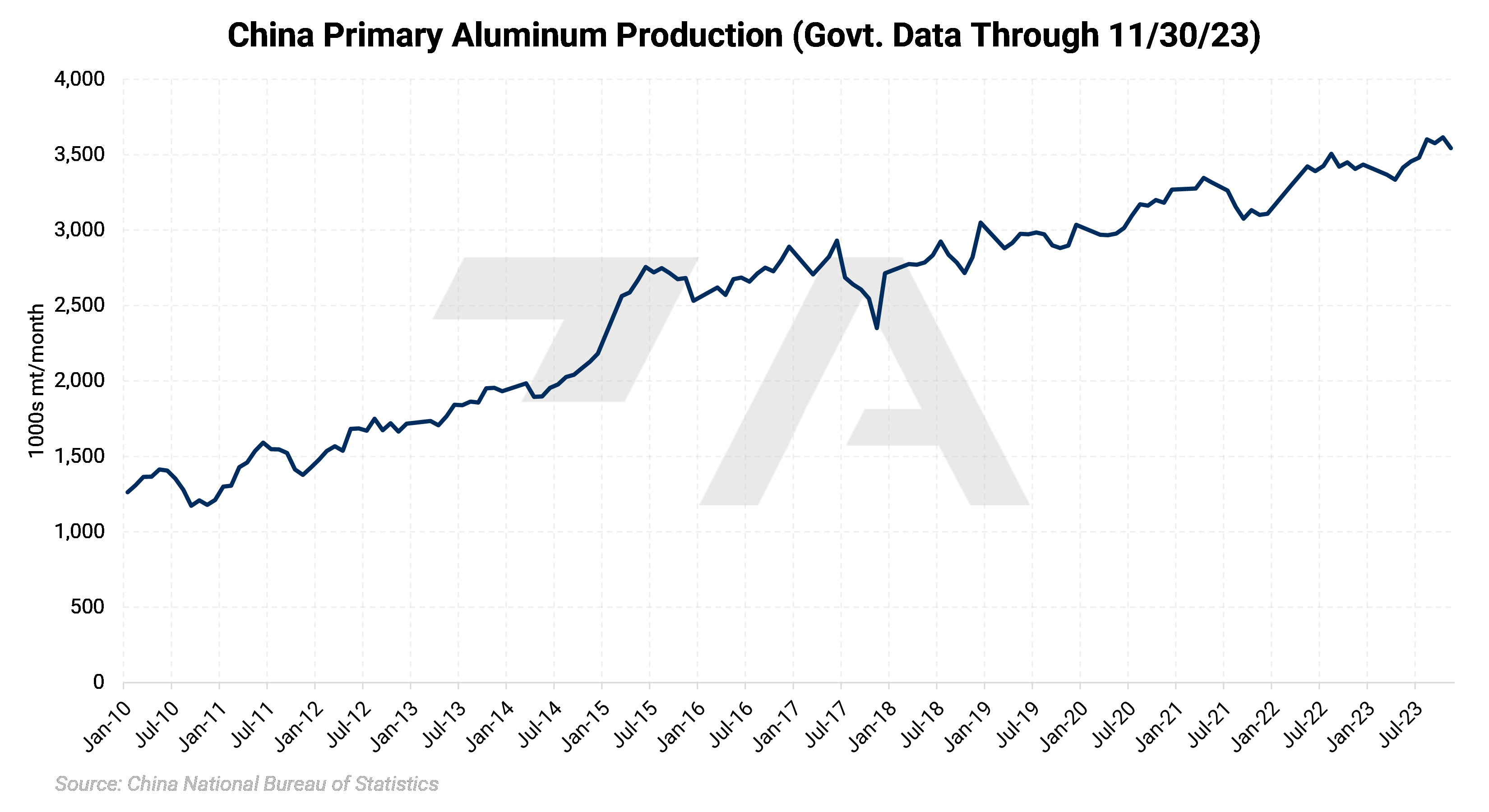

Aluminum production surges in 2023.In 2023, LME Aluminum finished essentially unchanged on the year despite soaring Chinese production amid tepid demand. As the chart below shows, China’s monthly production hit new all-time highs on several occasions this past year despite production issues in the country’s top production region, Yunnan province. So long as China’s smelters keep this brisk pace and demand doesn’t materially grow, we think that aluminum prices will likely remain rangebound in 2024. |

|

|

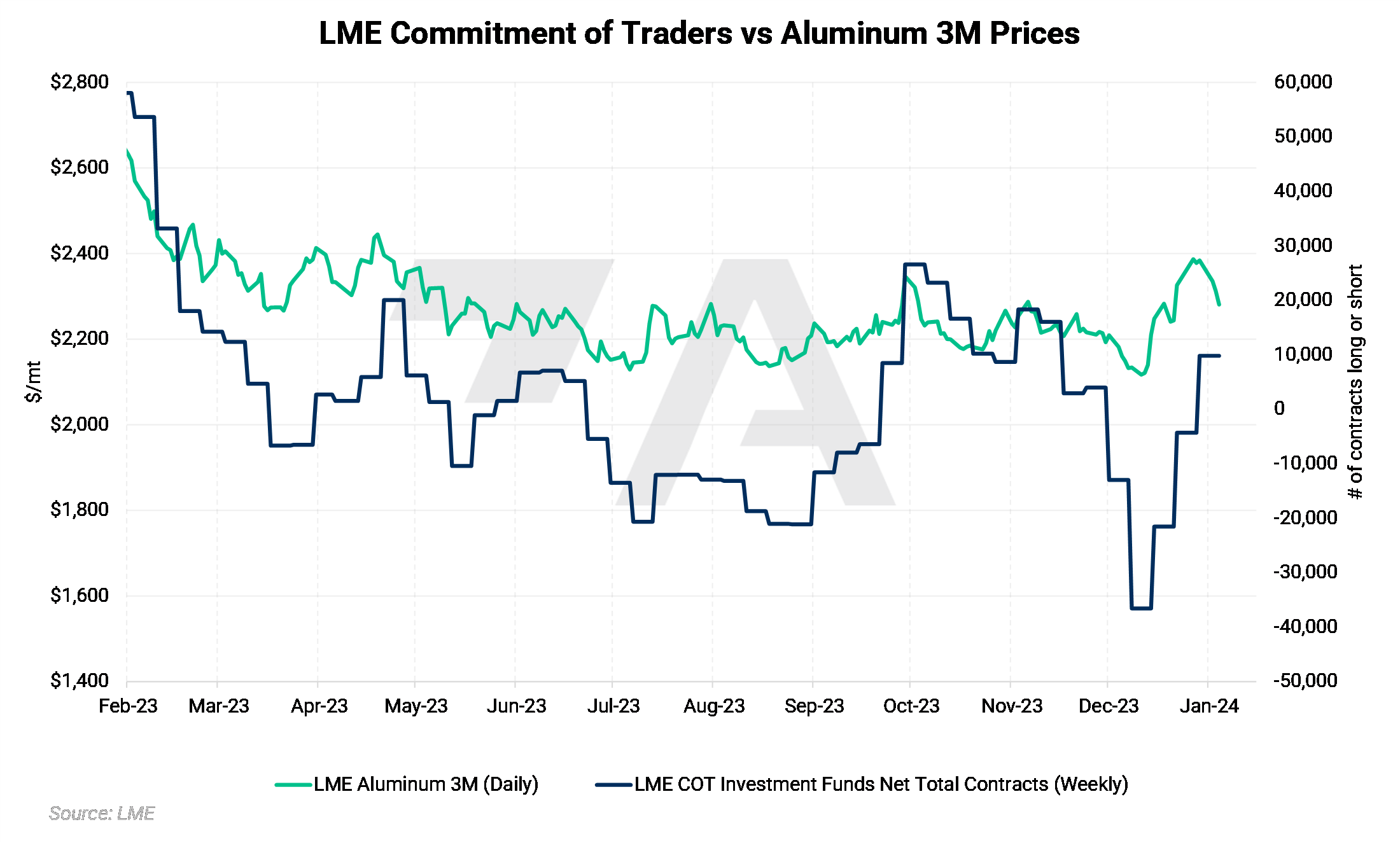

Aluminum prices are subject to speculator positioning.Speculative positioning was also a key driver of aluminum prices in 2023. As the chart below shows, the actions of investment funds, which are purely speculators in metals markets, essentially mirrored the price action of LME aluminum. Even though these funds spent very little time being net short last year, a reduction in their long position in early 2023 helped push the market lower, and a refusal to build a significant long position kept prices rangebound. The significant short position that they built in November quickly dissipated as bauxite and alumina production issues in China took center stage. Of course, we will continue to watch for any supply-demand issues that could impact investment funds' views (and, therefore, positioning) on LME aluminum. |

|

|

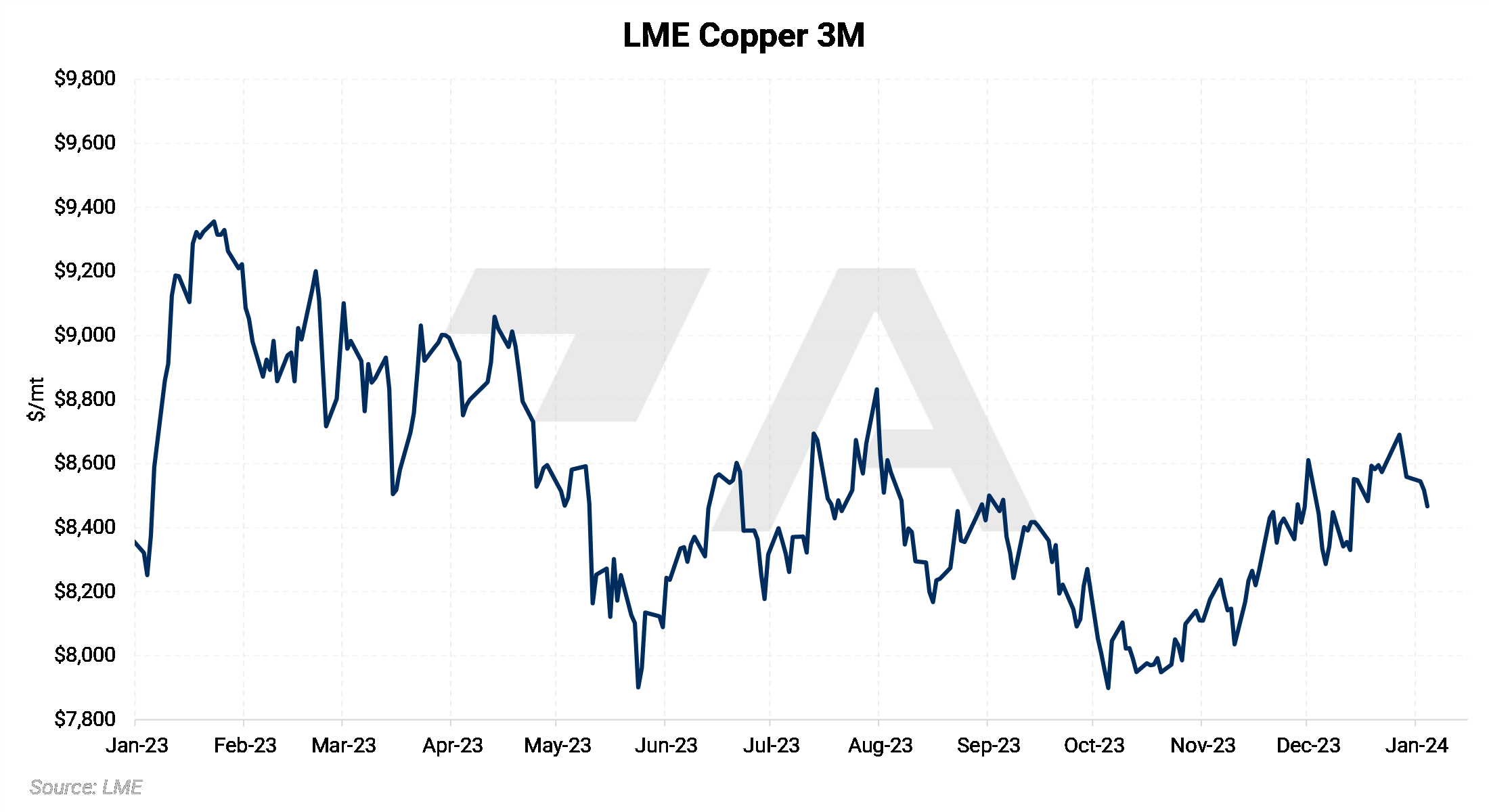

Copper has a last minute surge.Despite spending most of the year in the red, LME Copper finished up about 2% on the year. Most of this gain occurred in the final two months of the year. Although short-term production issues in South America dominated the headlines this year, the market largely shrugged off that news while demand issues held precedents. The permanent closure of Panama’s largest mine, which was responsible for about 1.5% of global production, along with rising import demand from China, helped spur the rally in late 2023. The Panamanian mine closure was particularly important, as it changed several analysts’ viewpoints on copper supply and prices for 2024. The copper market will likely remain in a surplus next year, but the surplus will be smaller than expected. This will likely help to keep a floor under copper prices in the coming year. |

|

|

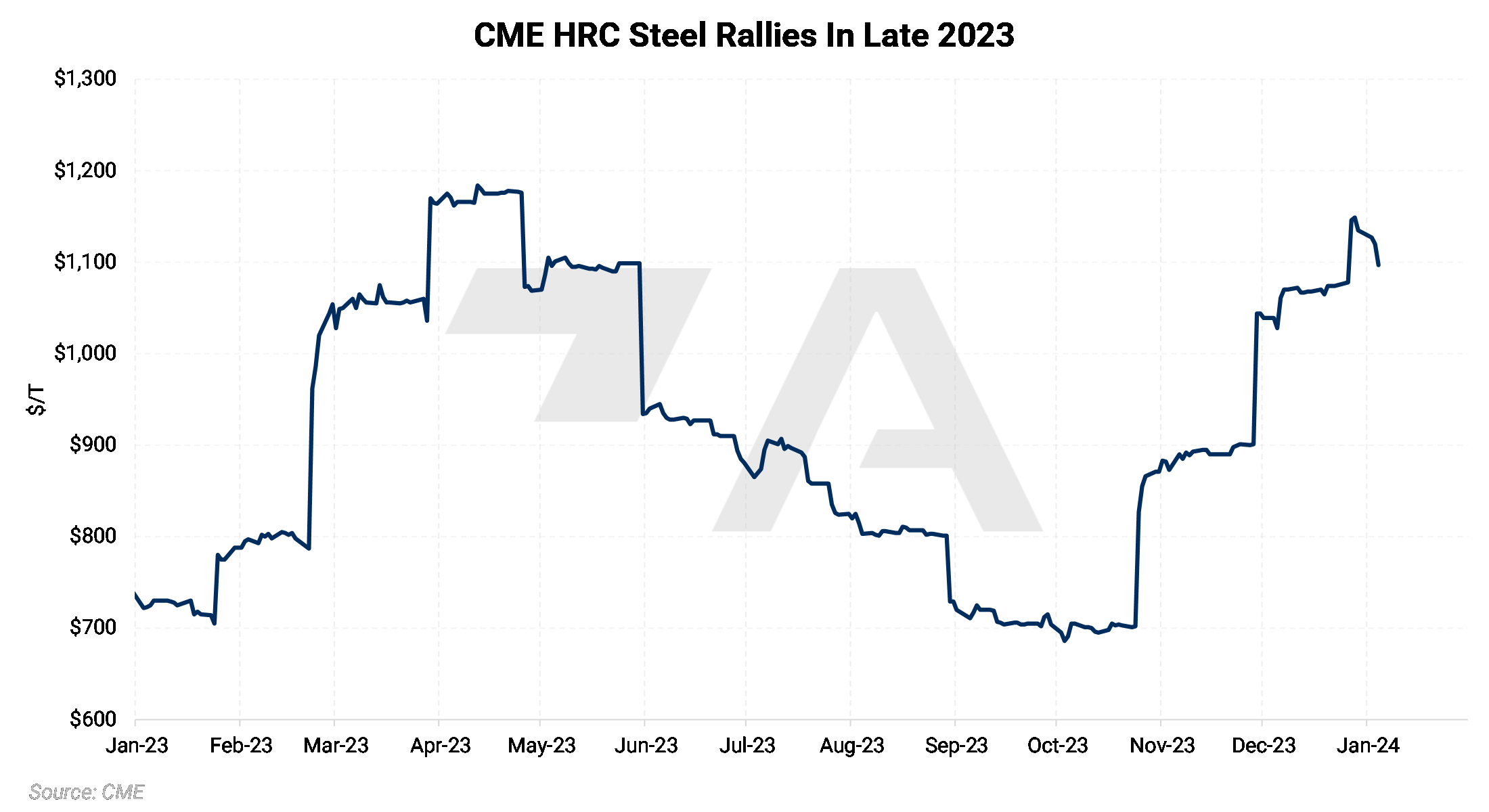

CME HRC Steel remains rangebound.Compared to other years since the pandemic, CME HRC steel prices were relatively rangebound in 2023. Prompt month HRC currently hovers near $1,100/st, up from around $700/st at the beginning of the year. Despite subpar demand, steel producers were quite disciplined about production, which helped them stay profitable and kept prices from falling dramatically. One of the most interesting developments in the steel market occurred in late December when Nippon Steel, a Japanese steelmaker, announced it would buy US Steel, an American rival. AEGIS cautions that US officials have already stated the deal will go through tremendous scrutiny that will likely drag into late 2024. Also, since most steel markets are regional, this merger will probably have little impact on steel supply, demand, or prices in the US. |

|

|

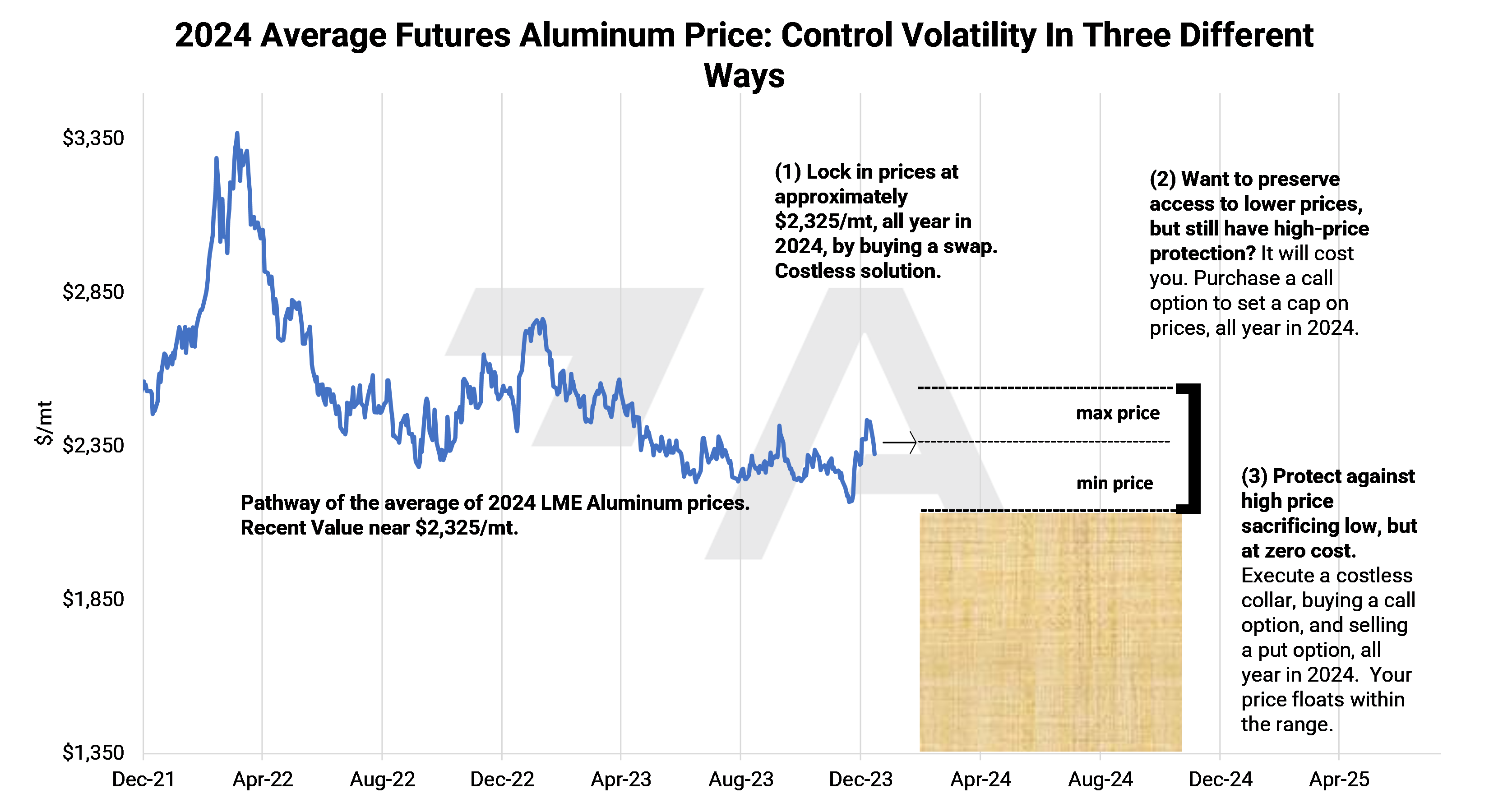

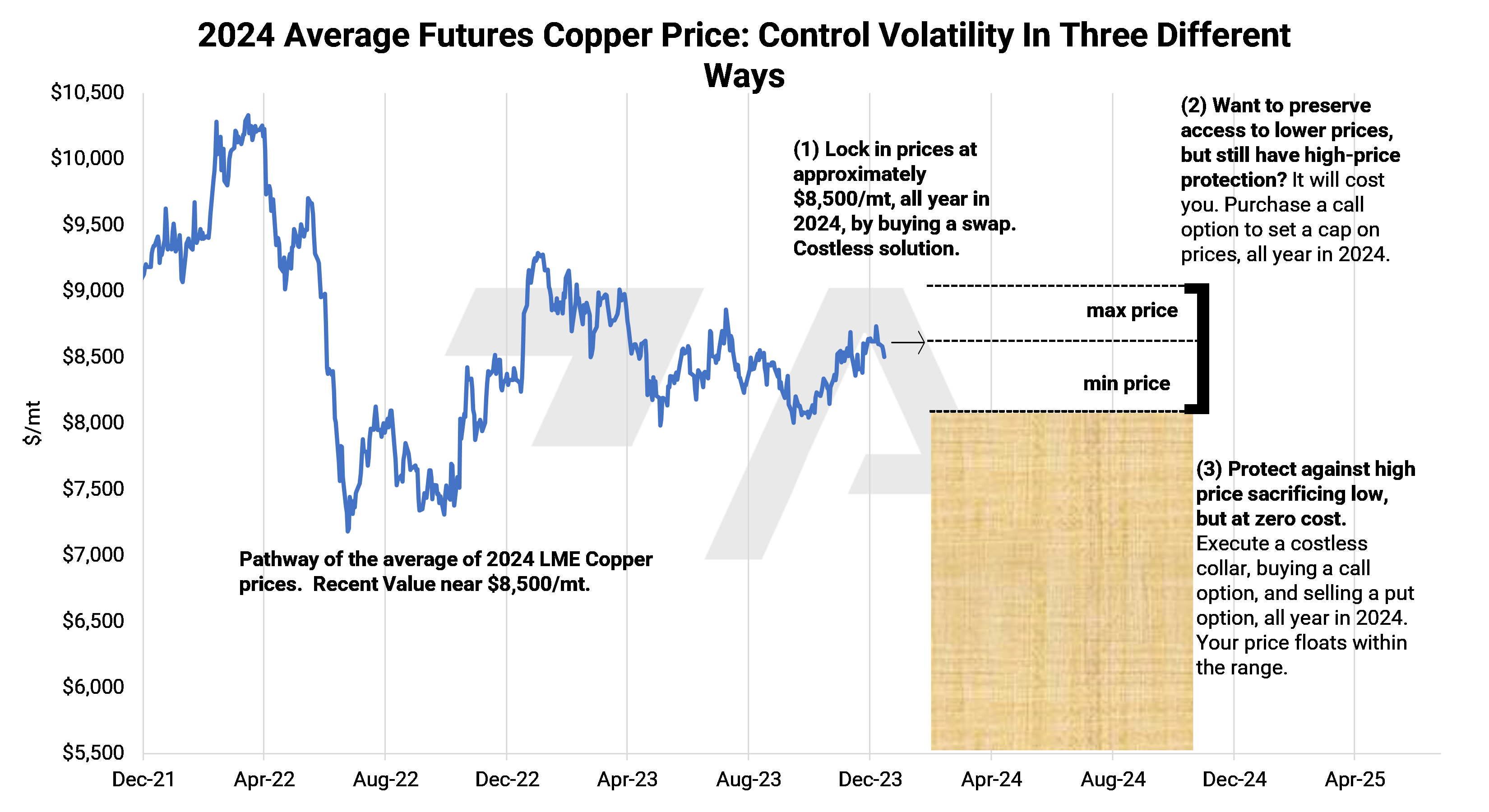

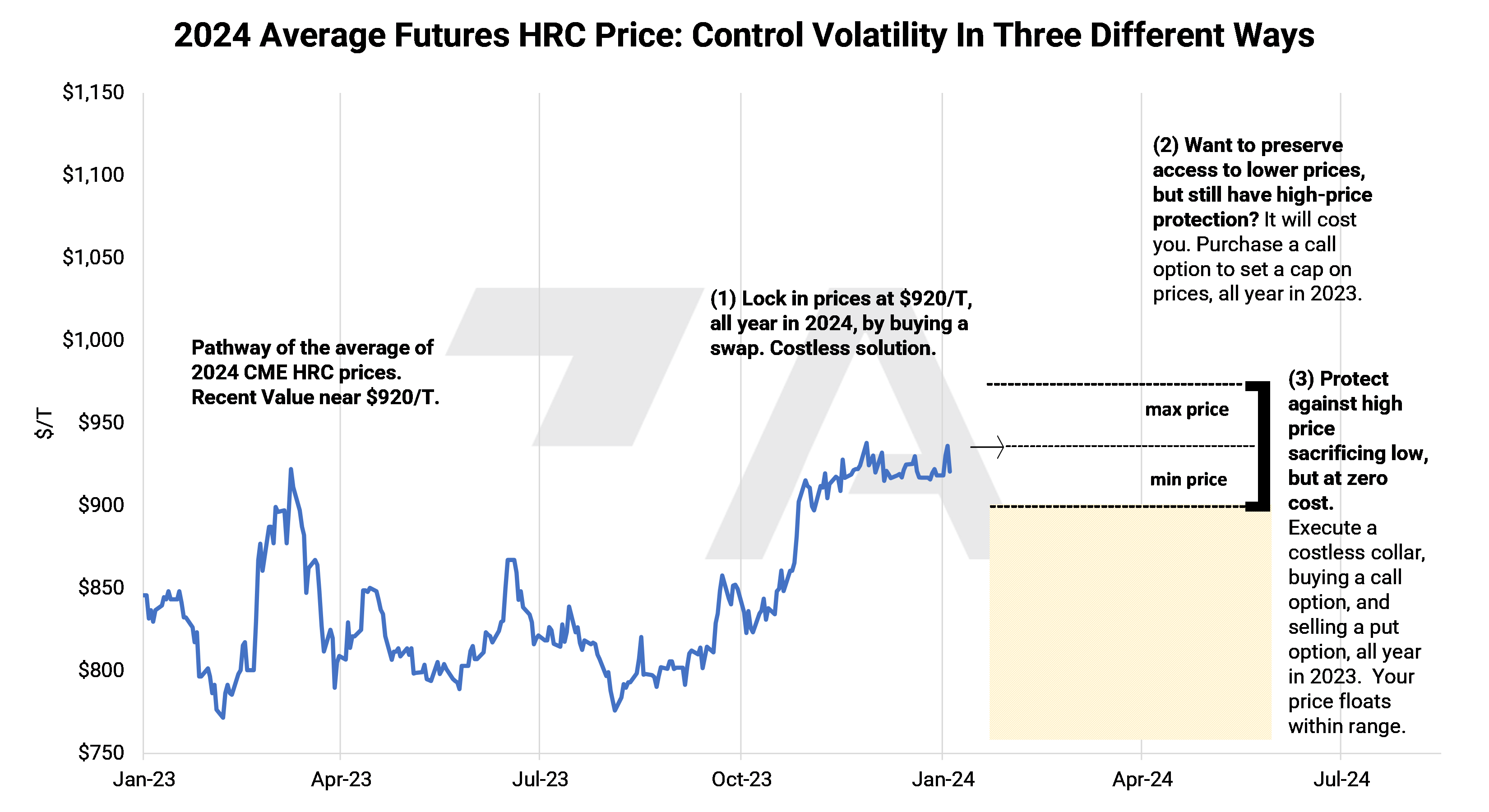

What should end-users do?... This price risk can be hedged!Relative to their 2023 trading ranges, we remain neutral to bearish on LME aluminum, copper, and CME HRC Steel in the short term. However, consumers of any or all three metals should consider long-term hedging at these levels. Demand should continue to recover (especially in China), and any supply issues will likely underpin the market. Below, we detail several hedging strategies for each metal. |

|

|

|

|

|

|

AEGIS can build your hedging program.AEGIS can help aluminum, copper, and HRC steel buyers develop specific strategies that fit their operations. We are also happy to introduce new clients to more counterparties, therefore ensuring that you are receiving the best possible price. Please contact us for details. |

Important Disclosure: Indicative prices are provided for information purposes only and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee of the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as "edge," "advantage," "opportunity," "believe," or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.