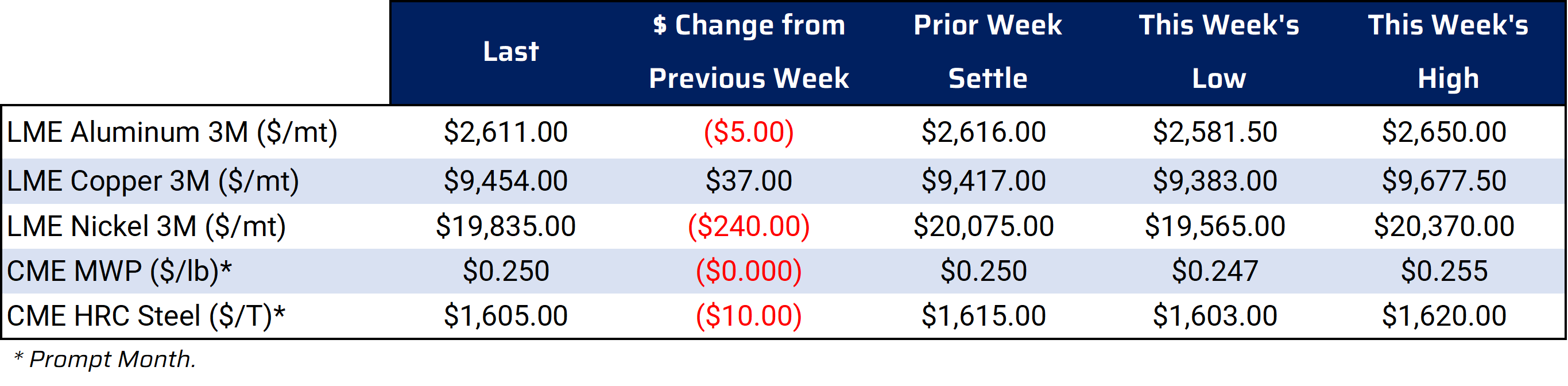

Bottom Line:LME Copper was the only base metal to advance this week. A major Peruvian producer expects to shut down a mine next week. Also, the amount of copper on warrant (i.e. available to trade) at the LME continues to be at historically low levels. Both facts could remain supportive to prices.Copper demand seems to be strong; however, headwinds remain. According to government data, Chinese imports of copper concentrate remain high, but unwrought copper imports are off levels seen this time last year. China’s faltering real estate sector could also weigh on demand. |

Notable Metals News

Prices of CME HRC Steel have tumbled in recent weeks. As of this writing, the December 2021 HRC has slid nearly $70/T in the last four weeks. Argus recently blamed the dip on seasonal maintenance shutdowns and buyer hesitancy to make spot market purchases. Maintenance season for some steel service centers runs between the Christmas and New Year’s holidays. Also, due to ample inventories, there are concerns that spot steel purchases might not rebound once the new year begins.

Potentially bullish aluminum news occurred in Iceland this week. As of Tuesday, December 7, Iceland’s main utility has lowered power to aluminum smelters. The national utility, Landsvirkjun, is cutting electricity to aluminum smelters by 30 MW. This represents 2.5% of the electricity the smelters purchase, according to Iceland Monitor. The company had planned to make cuts in January but is also blaming low hydroelectric reservoir levels and other bottlenecks for the setback. According to the US Geological Survey, Iceland was the 10th-largest aluminum producer in the world in 2020. The country produced 860,000 mt that year.

Like aluminum, potentially bullish news also happened in copper. One of Peru’s largest copper mines, the MMG Ltd-owned Las Bambas copper mine has been plagued by road blockages after environmental protestors began picketing late last month. Talks between the mine owners and protestors broke down earlier this week, and the company expects to shut down the mine next week. The duration of the possible shutdown is currently unknown. According to the company website, the Las Bambas mine produced 311,020 mt of copper concentrate in 2020. Reuters recently stated the mine can produce 400,000 mt of copper concentrate per year, which is approximately 2% of world production.

|

Hedge Strategy Suggestions: |

|||||

|

For LME Aluminum, the forward curve is relatively flat throughout 2022. However, it becomes backwardated (where shorter-term contracts are priced higher than the deferred market) beyond 2022. For consumers who are unsure of market direction, option collars (buying a call and a selling a put) are logical strategies. Producers can also use the relatively flat curve to hedge inventory. LME Copper is in backwardation through December 2023. Thus, end users can make deferred purchases at a deep discount to the cash market. Layering into swaps with tenors throughout the second half of 2022 might be a logical tactic for such end users. For CME HRC Steel, the backwardation begins immediately and is extreme. For example, the spread between January 2022 and February 2022 is approximately $100/T as of this writing. Similar to copper, layering into swaps with tenors throughout the second half of 2022 might be a logical tactic for such end users. |

|||||

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

Aluminum traded in very tight $68.50 range this week and was down a mere $5/mt. Its week-over-week trading range keeps getting smaller. Similarly, its forward curve barely budged. Perhaps a new catalyst is needed to break out of the recent ranges. |

|||||

|

|||||

|

The forward curve for the MWP looks like the letter “Z”. After stable prices throughout 2022, the market dips into backwardation beginning in January 2023. Given this week’s flat trade, the forward curve is barely above that of last week. |

|||||

LME Copper |

|||||

|

Like aluminum and the MWP, copper’s forward curve barely moved this week. As we stated in the opening, bullish and bearish supply-demand news seems to have had minimal impact on the market.

|

|||||

|

|||||

|

Continuing the theme, the shape of nickel’s forward curve is the same as last week and has barely moved. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

As for HRC steel, charts remain in a downtrend, and rallies have been met with quick resistance. Even as prices have begun to slide, the forward curve remains severely backwardated throughout calendar year 2022. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

12/10/2021: AEGIS Factor Matrices: Most important variables affecting metals prices 11/30/2021: Section 232 Tariffs: Most relevant developments (AEGIS Reference) 11/30/2021: Will the Omicron COVID Variant Impact South African Metals Production or Exports? |

|||||

Notable News |

|||||

|

12/9/2021: Evergrande has defaulted on its debt, Fitch Ratings says 12/7/2021: FEATURE: Copper market to be well supplied in 2022 12/8/2021: Landsvirkjun Reduces Power Delivery to Large Users 12/7/2021: US HRC: Prices resume downward slide 12/7/2021: FEATURE: Copper market to be well supplied in 2022 12/7/2021: Copper price up as China imports rise 12/7/2021: Aluminium prices may gain next year on demand, supply concerns 12/6/2021: China Evergrande shares plunge as it teeters on brink of default 12/6/2021: China frees up $188 billion for banks in second reserve ratio cut this year 12/3/2021: MMG's Las Bambas mine in Peru faces shutdown as talks to end blockade fail |

|||||