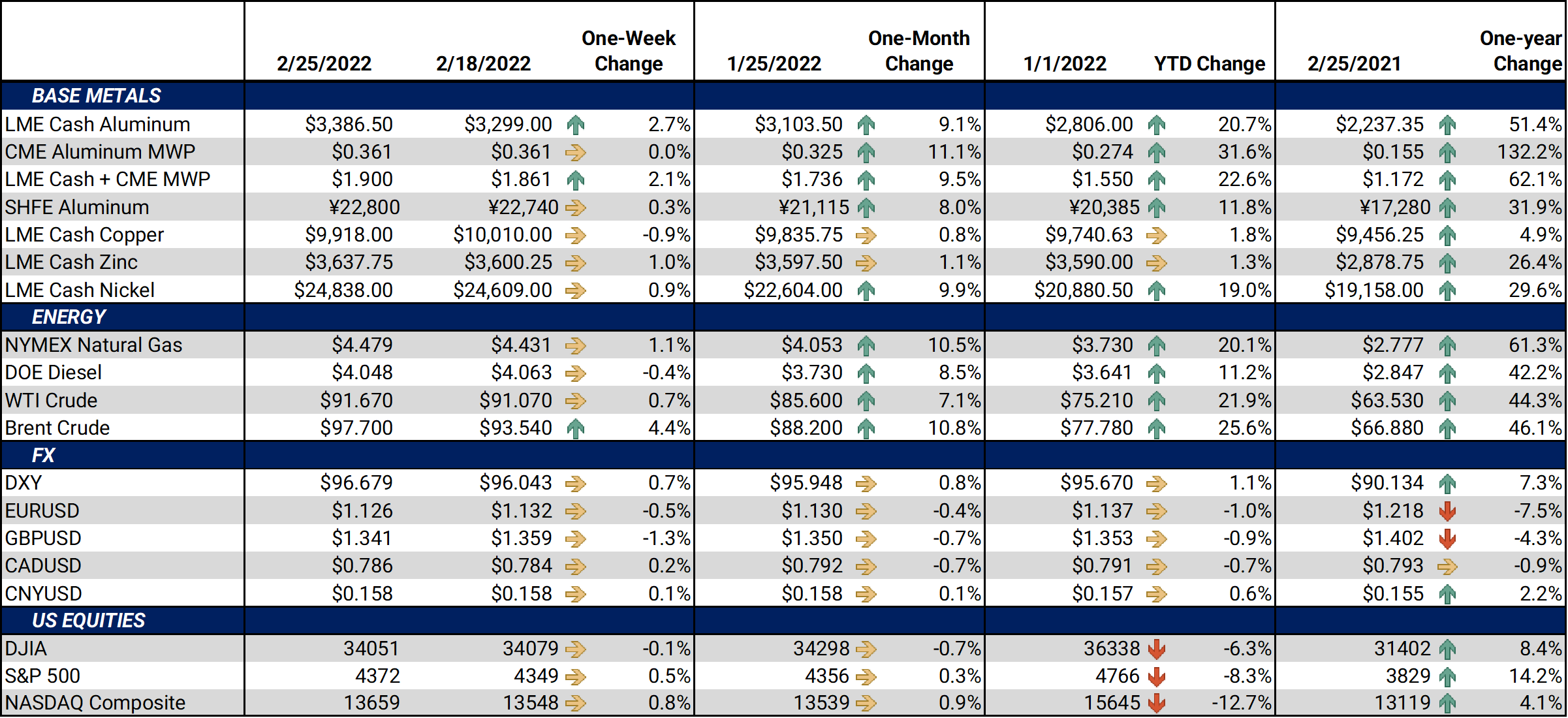

Bottom Line:Earlier this week, Russian President Vladimir Putin recognized two separatist, pro-Russian regions (Luhansk People's Republic and Donetsk People’s Republic) of eastern Ukraine as independent states. Putin also ordered troops into these regions. US President Biden sanctioned both regions and several Russian banks and people close to Putin. The EU and UK have also sanctioned Russia. Metals sanctions have not yet been included.Russia’s invasion of Ukraine has bolstered metals markets, namely nickel and aluminum. However, US has refrained from sanctioning Russian aluminum producers. In the weeks prior to the Russian invasion of Ukraine, White House officials had met with US aluminum industry representatives and at that time stated there was no plan to sanction Russian aluminum producers, according to Bloomberg. In 2020, Russia was the fifth-largest supplier of aluminum to the US, representing about 3% of our imports, according to the USGS. The US represented nearly 7% of Rusal’s (the state-owned aluminum producer) revenue in 2020, according to their annual report.Similarly, no European allies have yet sanctioned Russian aluminum producers. Europe imports nearly 9% of their aluminum tubes and pipes from Russia, according to trendeconomy.com. Nearly 41% of Rusal’s revenue in 2020 came from Europe, according to their annual report. Rusal does not give regional volume breakdowns in their annual report, only revenue by region.More Russian aggression would likely encourage more political response. Sanctions by either the US or Europe could jeopardize global supply and send LME prices and US or European premiums higher. |

Notable Metals News

The sanctions implemented this week might still slow steel exports from Ukraine, even if the sanctions do not target metal trade itself. The two separatist regions in Ukraine which were recognized by Russian President Vladimir Putin, and subsequently sanctioned by the US, are key strategic steel and iron ore production areas. Some Ukrainian steel production has stopped, according to Argus.

The most immediate effect of slower supply is on the European market, but the global nature of the steel market would likely force Europe's purchases into other regions. Loss of steel supply would test supply chains and prices beyond Europe.

Seven of Ukraine’s twelve steelmaking plants are in the two separatist regions, according to UKRMETALURGPROM, Ukraine’s metals association. According to the association, in 2021 Ukraine produced 19.08 million mt of metal products of which to 15.12 million mt, or 79.2% was exported. In 2021, the main markets for Ukrainian steel products, were EU-27 (35.0%), other Europe (19.4%) and NAFTA (9.7%). Ukraine is the sixth-largest supplier of steel to the EU, according to the European Steel Association.

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

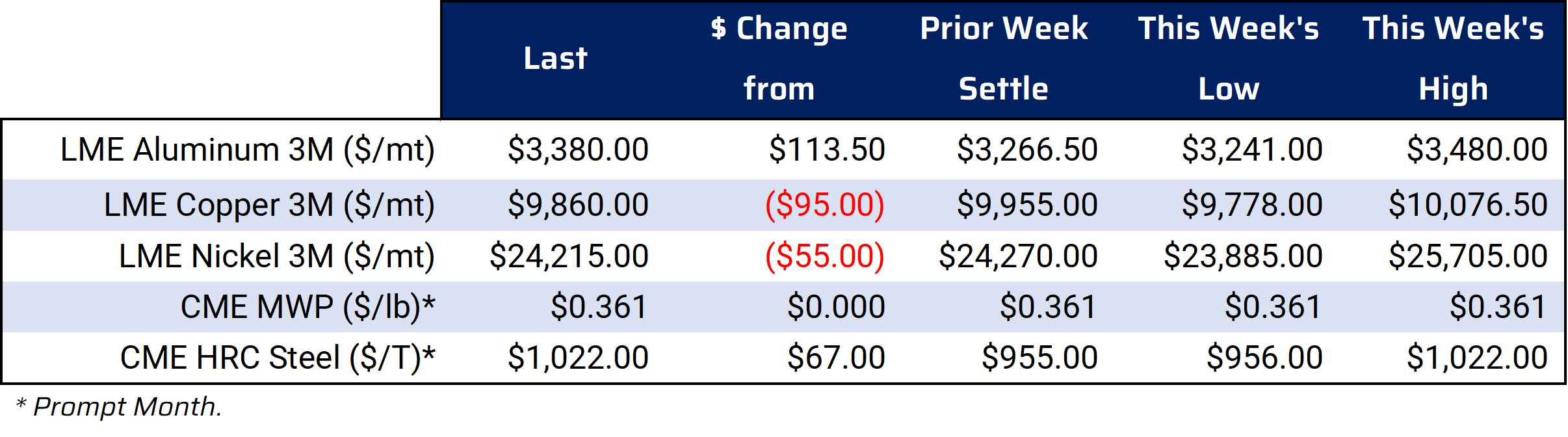

Aluminum prices rallied this week. The LME Aluminum forward curve remains backwardated, or downward sloping. For most 2022 contracts, the curve shifted higher by slightly over $100/mt. The backwardated curve shape is a benefit to consumers, allowing for hedging at prices lower than current cash or near-term prices. End users who have longer-term price risk might consider zero-cost collars as pressure to the upside remains in play. Producers can sell forward a portion of forecasted production volumes using a layered swap strategy. Please note that doing so may incur losses – in other words, limit your upside price benefit – if prices rally further. Such producers may consider purchasing out-of-the-money puts at historically high prices to increase the likelihood of achieving revenue targets. Finally, the new war between Russia and Ukraine could affect aluminum supplies. Russia is an important aluminum supplier, and trade frictions or sanctions could endanger global supply and send prices higher. |

|||||

|

|||||

|

The forward curve for the Midwest Premium (MWP) has shifted slightly higher compared to last week. Those who need to make sales further down the curve might consider hedging a smaller percentage of expected exposure. Please note that doing so might incur hedging losses if prices rally further, perhaps offsetting the beneficial increase in asset values. |

|||||

LME Copper |

|||||

|

LME Copper prices were down this week. Copper’s forward curve remains in backwardation through December 2023. The forward curve through has shifted slightly lower compared to last week. End users who have longer-term price risk may consider zero-cost collars. The backwardation allows for an attractive ceiling (cap) price by buying a call option, while still participating in much lower prices (should they decline), compared to cash. The risk in such a strategy is chiefly reduced access to low prices in an extreme bearish event. Producers can sell forward a portion of production forecast using swaps at historically high prices to increase the likelihood of achieving revenue targets. Please note that selling swaps may incur hedging losses if prices rally further, so matching the price basis of your hedges with the price basis of your production is very important.

|

|||||

|

|||||

|

The forward curve for nickel has shifted slightly higher, while the shape of the curve is relatively unchanged from last Friday’s. Like some other LME metals, nickel’s forward curve is quite backwardated. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

For CME HRC Steel, prices through mid-2022 are aligning with spot prices more closely. In other words, the nearby part of the forward curve has flattened. The forward curve for 2022 has shifted slightly higher from last week. The front three contracts have moved to a slight contango. However, beyond July ’22 the forward curve remains backwardated, meaning that future prices are lower than spot prices. Consumers can take advantage of this backwardation by purchasing swaps or call options. Please note that doing so might incur losses if prices slide further. The CME HRC steel market is thinly traded, so please contact AEGIS for strategies. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

02/16/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 02/15/2022: Section 232 Tariffs: Most relevant developments (AEGIS Reference) |

|||||

Notable News |

|||||

|

2/25/2022: Ukraine ports and steel plants shut down: Update 2/24/2022: Factbox: Commodity supplies at risk as Russia invades Ukraine 2/24/2022: Biden imposes additional sanctions on Russia: 'Putin chose this war' 2/24/2022: Stocks slump, oil rips past $100 as Russia invades Ukraine 2/23/2022: Russia’s Putin announces military operation in Ukraine 2/23/2022: Statement by President Biden on Nord Stream 2 2/22/2022: Nickel price hits decade high as Ukraine tensions fuel supply concerns 2/22/2022: Biden responds with limited sanctions after Putin recognizes breakaway Ukraine regions 2/22/2022: U.S. imposes sanctions after Putin recognizes breakaway Ukraine regions 2/21/2022: Statement by Press Secretary Jen Psaki on Russian Announcement on Eastern Ukraine 2/21/2022: Aluminum shortages to deter blanket sanctions on Rusal |

|||||