Bottom Line:The "best ever" aluminum demand in 2021 and early 2022 will dissipate and lead to large surpluses in 2023 and 2024, says Harbor Aluminum. According to their estimates, the supply surplus could reach 1.1 million mt in 2023 and 1.4 million in 2024, up considerably from an expected surplus of 200,000 mt in 2022. At its annual summit this week, Harbor Aluminum's managing director asserted, "We all know that last year and so far this year has been the best ever in terms of demand. But there's one component of that demand borrowed from the future, and we'll need to pay that -- consumers cannot sustain this level of goods spending seen the past two years." |

Notable Metals News

A bearish tone for aluminum demand is also affecting international premium prices. Yesterday Bloomberg reported that one producer was offering $162/mt for July-September shipments to Japan, and one major consumer was bidding $130/mt. Late last week, Reuters that producers were offering premiums of $172/mt to $177/mt for July-September shipments to Japan, nearly unchanged from last quarter's premium of $172/mt. This is the premium over the London Metal Exchange (LME) cash price that Japanese importers agree to pay for primary aluminum shipments. One trader cited by Reuters last week proclaimed, "A significant volume of aluminum has been transported in recent months from LME warehouses in Asia to Europe, where premiums were much higher…. But the Asian market is still in a glut due to the lack of easy container arrangements to ship more metal out of the region." Negotiations for 3Q are ongoing but should conclude by month's end. According to the Japan Ministry of Finance and USGS data, the country imported approximately 2.793 million mt of aluminum in 2021, or about 4% of global production.

China's COVID lockdowns, which started in March, have weighed on copper demand and global prices in recent months. Prior to Monday, LME copper prices dropped from $10,080/mt to $9,520/mt, or 5.5%, between March 1 and June 1. However, LME Copper 3M Select surged on Monday after Shanghai eased lockdowns late last week and allowed companies to resume production. Still, it will take a while for manufacturing volumes to return to normal, according to Bloomberg. One analyst quoted by Reuters on Monday asserted, "We agree with this directionally but remain cautious as we still believe a timely and decisive rollout of stimulus measures, over and above what has been announced, from China is required to support prices at current levels."

As for steel, global steel prices are expected to remain high, yet lower than 2021 levels, according to Moody's Investor Services. In its most recent mining and metals outlook, released on Monday, Moody's stated that steel consumption in China has dropped due to COVID lockdowns, and the country's rising inflation has weighed on sentiment. In addition, the research firm says that supply-chain issues are reducing global demand, and panic buying of steel is decreasing. As for raw material costs, iron ore prices could drop as Brazil increases its output; however, Chinese steel production and demand will likely be the dominant driver in steel prices moving forward.

Finally, regarding both steel and aluminum, automotive manufacturers are experiencing reduced profit margins due to all-time high costs for raw materials such as metals and petrochemicals, according to the Wall Street Journal's summary of comments from Bank of America. According to BofA's calculations, raw material costs for the average US vehicle now total $4,950, nearly 86% higher than the 30-year historical average of $2,660. The Wall Street Journal's summary also adds, "Record vehicle prices have helped automakers offset those higher costs. But the bank sees vehicle prices easing in the next few years, compressing margins if raw materials remain elevated."

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

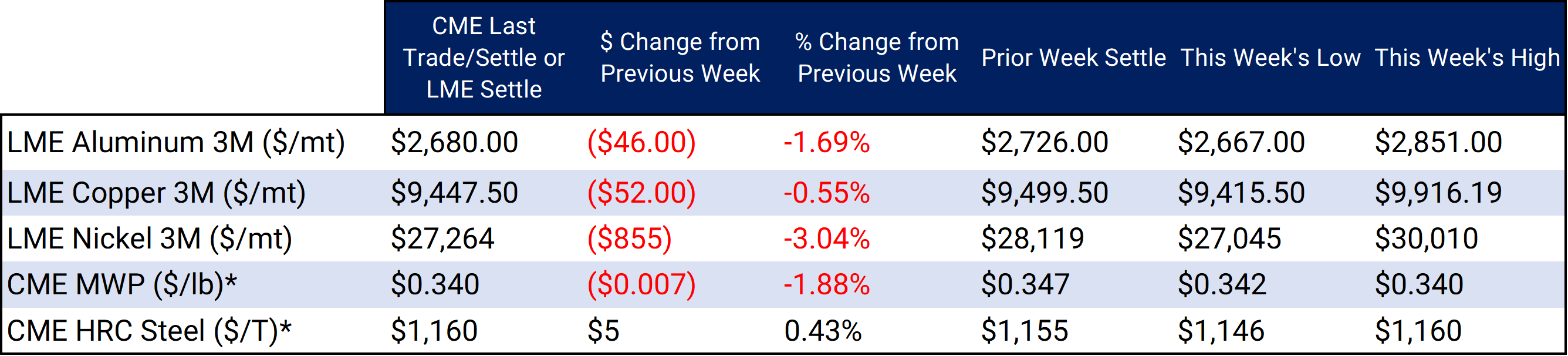

LME Aluminum 3M settled at $2,680.00/mt, down $46.00/mt on the week. Compared to last Friday, the forward curve for LME Aluminum has shifted slightly lower vertically by approximately $50/mt. The forward curve is now backwardated beyond October 2022, peaking with a small "hump" that month. The backwardated curve from November onwards allows aluminum end-users to hedge future needs at prices cheaper than that of spot prices. The aluminum market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 34.00¢/lb this week. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this market is tricky, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $9,447.50/mt, down $52/mt on the week. Similar to aluminum, LME Copper's forward curve has also shifted vertically lower by approximately $50/mt compared to last Friday. The forward curve is relatively flat through December 2023, but then reverts to backwardation in January 2024 and beyond. A backwardated forward curve favors copper consumers. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $27,264/mt, down $855/mt on the week. Nickel prices were down this week, but the shape of nickel's forward curve is essentially unchanged compared to last Friday. However, it has shifted vertically lower by approximately $900/mt compared to last Friday. It remains in a slight contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded at $1,160/T, up $5/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with strategically placed limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

06/8/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 05/23/2022: India's Steel Exports Tariffs Shock Producers 05/11/2022: China's Metals Exports are on the Rise |

|||||

Notable News |

|||||

|

6/9/2022: Copper price slips after new China lockdowns 6/9/2022: China COVID jitters flare up as parts of Shanghai resume lockdown 6/7/2022: Steel output starts June with a lull 6/6/2022: Stronger China demand prospects propel copper to five-week peak 6/3/2022: Peru Cabinet meeting ends with no word on Las Bambas mine crisis 6/2/2022: Copper price scales $10,000 on Chinese stimulus, lockdown reprieve 6/1/2022: UPDATE 1-Global aluminium producers seek Q3 premiums of $172-$177/T in Japan talks - sources

|

|||||