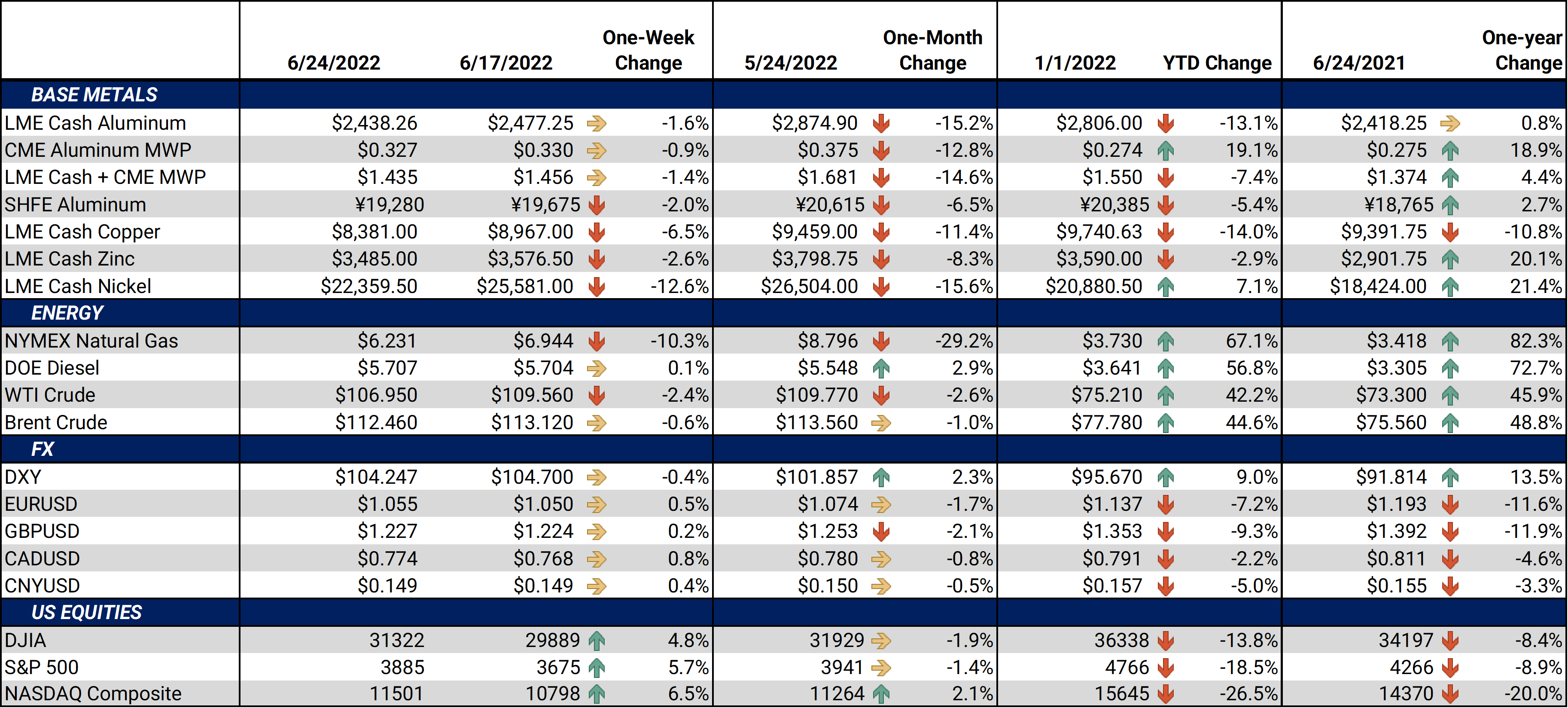

Bottom Line:Century Aluminum, which is the largest American primary aluminum producer, is temporarily idling its largest smelter due to “skyrocketing energy costs,” according to a June 22 press release. This is the first major announcement in recent history of a shutdown by a US metal producer, according to Bloomberg. The Hawesville, KY facility, which has a production capacity of 250,000 mt/year, will begin idling procedures on Monday, June 27. According to Century’s CEO, the “unprecedented rise in global energy prices arising from the Russian war in Ukraine has dramatically increased the price of energy in the U.S. and around the globe. The power cost required to run our Hawesville, KY, facility has more than tripled the historical average in a very short period. Unfortunately, this makes it necessary to temporarily curtail operations for approximately nine to twelve months until energy prices return to more normalized levels. We are confident that energy prices will moderate in the next year and believe strongly in the future prospects of the Hawesville smelter given its recent performance and the continuing important role it plays in US national security.” Most of the smelter’s 600+ employees will be laid off while the plant is idled. AEGIS notes that the local power and gas prices in Kentucky and elsewhere in the U.S. have very weak links to European prices. It is possible the international demand for thermal coal may have increased local power prices, but only be indirect means. Still, other producers (and manufacturers in general) can often hedge energy prices, and AEGIS can show you how.

|

Notable Metals News

Spot ferrous scrap prices are off 20% since March, and many analysts expect more weakness. American steel and ferrous scrap markets “seem to be heading into the summer with reduced momentum,” according to Recycling Today. According to Kallanish Commodities, a reduced “buying appetite” by Turkish mills, cheaper Russian billet, a weakening Chinese steel market, and overall bearish industry sentiment are to blame for lower American scrap prices. Shredded-steel scrap prices have already tumbled this year. In its monthly index update released on Monday, the Raw Material Data Aggregation Service confirmed that spot shredded scrap prices are down from $604/T in March to $481/T in June. Some scrap market participants remain bearish, as one anonymous steel supplier quoted by Kallanish Commodities on Monday stated “All grades are likely to fall. I am having difficulties in foreseeing a recovery in the near future.” Kallanish itself echoed similar comments, proclaiming “US scrap market conditions are pointing to further price falls.”

Recession fears and a poor outlook for Chinese demand have weighed on copper prices, and analysts fear these factors could continue to do so. This is an about-face from bullish estimates earlier this year, as analysts quoted by mining-journal.com in January predicted $10,500/mt or higher due to a forecasted pre-Beijing Olympics demand boom and supply-chain bottlenecks that would impact supply. On Monday, Ole Hansen, head of commodity strategy at Saxo Bank A/S proclaimed, “Copper is facing a triple challenge currently… the technical outlook is weak following the lowest weekly close in 14 months, extended China lockdowns, and not least increased recession concerns following last week’s multiple rate hikes.” In a note late last week, UBS Group analysts made similar comments regarding copper, stating “demand outlook is mixed with a China recovery offset by the deteriorating macro outlook for Europe/US due to inflation.”

As for Chinese aluminum production, the Henan province, a key production region, could curb output if power generation problems occur this summer, according to Reuters. The province experienced a record power load this past Sunday, and “electricity supply in Henan is expected to be relatively difficult this summer,” according to Reuters’ summation of a state media report from this past weekend. Andy Home of Reuters predicts “power will be prioritized for cooling homes with big industrial users facing rationing.” China produced a record 3.423 million mt of primary aluminum in May, according to the National Bureau of Statistics. The Henan province produces about 36% of China’s primary aluminum, according to the South China Morning Post.

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

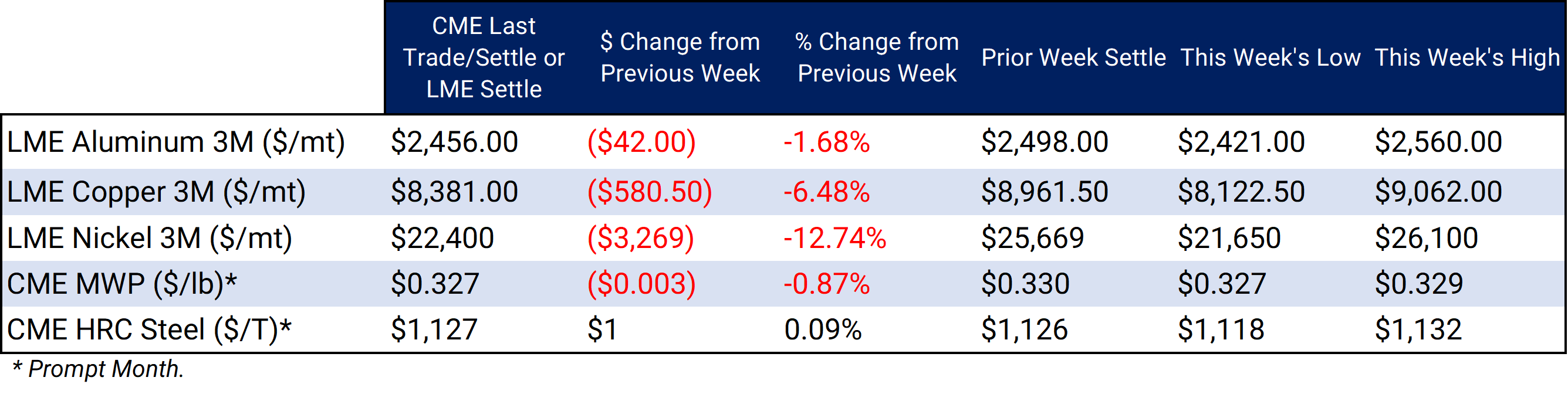

LME Aluminum 3M settled at $2,456.00/mt, down $42.00/mt on the week. Compared to last Friday, the forward curve for LME Aluminum has shifted lower vertically by approximately $50/mt. The forward curve is now in contango through 2026, meaning that spot prices are lower than futures prices. This allows aluminum producers to hedge future sales at prices higher than that of spot prices. The aluminum market has sufficient liquidity to use swaps and options. If you are a consumer of aluminum, you might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 32.67¢/lb this week. The CME Midwest Premium contract continued lower this week and remains in backwardation. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly-traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,381.00/mt, down $580.50/mt on the week. Similar to last week, LME Copper's forward curve has shifted vertically lower by approximately $500/mt compared to last Friday and is essentially flat through 2025. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $22,400/mt, down $3,269/mt on the week. Nickel prices were down again this week. Nickel's forward curve is in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded at $1,127/T, up $1/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with strategically placed limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

06/23/2022: What is Green Steel Anyways? 06/22/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 05/23/2022: India's Steel Exports Tariffs Shock Producers |

|||||

Notable News |

|||||

|

6/22/2022: Chile copper workers begin nationwide strike over smelter closure 6/22/2022: Explainer: Why is there a worldwide oil-refining crunch? 6/22/2022: Toyota cuts July global production plan by 50,000 vehicles 6/21/2022: Steel output and price drops hit ferrous market 6/21/2022: Copper price rises as looming strike in Chile adds to supply worries 6/21/2022: Column: Global aluminium production pendulum swings back to China 6/20/2022: Column: Iron ore suffers short-term demand woes, longer-term China threat 6/20/2022: China power demand sets new records as heatwaves bake northern cities 6/20/2022: Analysis: Quantity over quality - China faces power supply risk despite coal output surge 6/17/2022: Chile's Codelco to close Ventanas smelter 6/17/2022: Peru expects lower economic growth on impact of mine protests

|

|||||