|

Aluminum *Please note that our offices will be closed on Monday, January 1, due to the New Year’s Day holiday. The LME and CME are also closed that day. We will not produce a Metals First Look that morning. * |

|

|

Aluminum and alumina prices jumped late last week and early this week after an explosion occurred at one of Guinea’s main ports that is responsible for most of the country’s bauxite exports. Bauxite is the ore from which alumina is produced, and alumina is then processed to make aluminum. Nearly 70% of China’s bauxite imports come from Guinea, making it an important supplier to the world’s largest aluminum-producing country. (Source: Bloomberg) Aluminum stockpiles at LME warehouses continue to surge due to the UK’s recent ban on Russian metals. As of Friday morning, 549,050 mt of primary aluminum sits in LME warehouses, up from 454,375 mt on December 1. Nearly all of the LME’s stocks are in Asian warehouses. The LME’s South Korea warehouses are known repositories of Russian metal, but the recent influx has also occurred in Taiwanese and Malaysian warehouses. Earlier this month, the United Kingdom banned its citizens and companies from trading Russian-origin metals. (Sources: LME, Bloomberg) |

|

Copper Analysts are bullish on miners and metals producers for early 2024. In a note earlier this week, analysts from Jefferies proclaimed, “The prospect of Fed rate cuts, falling treasury yields, and a weaker dollar are clear buy signals for mining equities." They did caution that “a rally could be shortlived if a recession follows.” (Source: Bloomberg) Similarly, analysts are bullish on copper, but this is due to Chinese supply concerns as opposed to outside market influences in the US. Ming Gong, a metals analyst at Chinese brokerage Jinrui Futures, asserted, “The market’s supply-demand balance for next year has changed. We see disruptions in [the] availability of copper concentrates and there’s still not enough scrap for smelters or consumers.” (Source: Bloomberg) Although some analysts are quite bullish on copper for 2024, others have a more tempered view. In a synopsis from earlier this week, Argus stated that supply issues in Central and South America remain problematic, but demand, specifically in the global EV sector, is expected to slow. Also, China’s property sector continues to struggle despite recent economic stimulus measures. (Source: Argus) UAE-based International Resources Holding will invest $1 billion into Zambia’s Mopani copper mines (ZCCM), Zambia announced late last week. Although the mines are operational, ZCCM is currently not profitable and operates at about one-fifth of its potential capacity. As Bloomberg suggested, this investment will boost the production of cobalt and copper, both of which are key for the energy transition. Zambia is Africa’s second-largest copper producer, behind the Democratic Republic of Congo. (Source: Bloomberg) |

|

Steel Like copper, Argus is similarly skeptical about US domestic steel demand as well. Prices rallied in the fourth quarter due to major steel producers holding down production. But with demand expected to wane in early 2024, further prices are unlikely. Also, the prospect of buyers bringing in cheaper imports could weigh on the steel market. (Source: Argus) One of the world’s largest nickel smelters, based in Indonesia, shut down earlier this week due to a deadly fire that caused extensive damage. “We have ordered PT Indonesia Tsingshan Stainless Steel to stop its operation until our entire investigation is completed,” a local police chief stated. The operation is a subsidiary of China's Tsingshan Holding Group, the world’s largest stainless steel producer. (Source: Reuters) Iron ore prices in Southeast Asia have surged to an 18-month high while demand prospects continue to improve. Late last week, several of China’s largest state-owned banks cut interest rates while recent data showed that real-estate transactions are picking up. Also, some market participants believe the Chinese government will conduct another round of real estate-related stimulus measures. All of these moves will likely boost steel demand in the world’s largest producer and consumer of the metal. (Source: Bloomberg) |

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

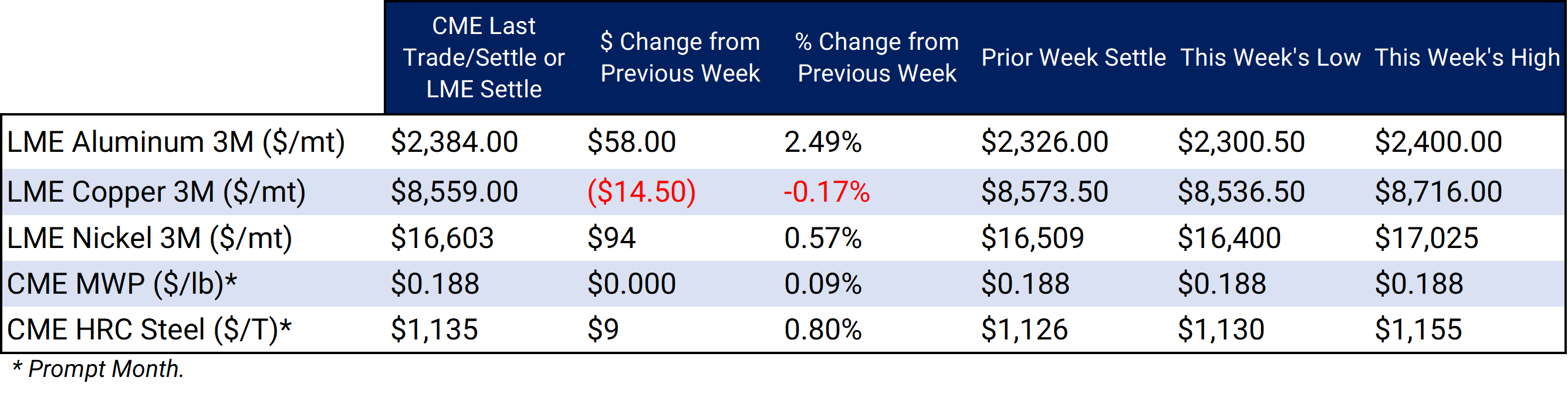

LME Aluminum 3M settled at $2,384/mt, up $58/mt on the week. Aluminum prices were up this week. This has caused the futures forward curve to shift vertically higher by approximately $60/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 18.8¢/lb this week. The CME Midwest Premium market is now in a contango from the January ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,559/mt, down $14.5/mt on the week. Compared to last Friday, LME Copper's forward curve has fallen vertically by approximately $15/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $16,603/mt, up $94/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $95/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $1,135/T, up $9/T on the week. Steel mill profit margins have improved dramatically in Q3 and Q4. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $657/st, up from about $320/st on September 1. This is mainly due to prompt month CME HRC steel futures rallying alongside prices in the physical market. Since steel prices have increased significantly recently, mills should consider hedging production and raw material usage for late 2023 and early 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

12/27/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 12/8/2023: Aluminum and Copper Markets Diverge but Hedging Opportunities Persist for End-Users 12/06/2023: Important US Economic Data (AEGIS Reference) 11/17/2023: Aluminum and Copper End-Users Should Hedge As Inflation Eases |

|||||

Notable News |

|||||

|

12/26/2023: Viewpoint: Copper demand in question for 2024 12/26/2023: Death toll at Indonesia smelter fire rises to 18, operation halted 12/24/2023: Indonesia nickel smelter furnace fire kills 13 workers, injures 46 12/23/2023: Guinea fuel supplies improving since oil storage blast 12/22/2023: Minor metals markets brace for Jan shipping disruptions |

|||||