|

Aluminum China's aluminum production is nearing last year's peak levels, with a significant ramp-up in previously idled capacities in Yunnan province. The increase in production, which rose 5% year-on-year to 3.65 million metric tons in May, is pushing domestic alumina prices close to their highest since late 2021. This surge is largely due to improved rainfall in Yunnan, alleviating previous power shortages and allowing local authorities to lift restrictions on aluminium producers, thereby reinstating approximately 1.15 million tons of capacity. (Reuters, July 1, 2024) |

|

|

However, this increase in aluminum production is straining the alumina supply, as the growth in demand from smelter restarts outpaces the production of alumina, which only saw a 3.4% increase. The mismatch is evident in the price performance on the Shanghai Futures Exchange, where alumina prices have risen by 15.3% since January, compared to a 3.5% increase in aluminum prices. This scenario has led to higher and more volatile alumina pricing, exacerbated by environmental inspections and the increased reliance on bauxite imports from Guinea, highlighting a new vulnerability in China's position as the world's leading aluminum producer. |

|

Copper A major indicator of Chinese copper demand has shown positive signs for the first time in nearly two months, as buying activity increases. The premium for imported refined copper in Shanghai's tax-free bonded zone climbed to $3 a ton, marking a shift from its unusual recent discount to LME prices. This adjustment follows a period since May during which buyers were hesitant to meet record copper prices amid soft demand for the metal. Despite copper’s rise, driven partly by speculative investments, its momentum had slowed due to perceived weaknesses in the Chinese market, the world's largest consumer of the metal. Recent developments suggest a potential strengthening of the market; the Yangshan premium has turned positive and copper stockpiles in China decreased last month after a significant increase in May. However, the sustainability of this uptick in purchases, attributed by some analysts to delayed buying rather than a genuine improvement in demand, remains uncertain. (Source: Bloomberg) |

|

Other Important LME and CME Metals & Markets

|

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

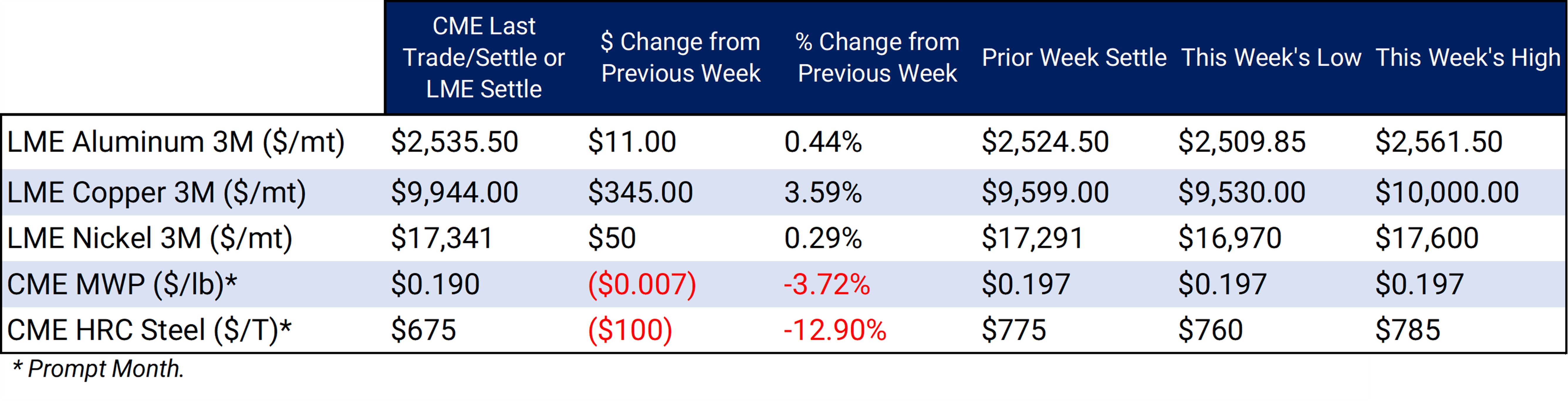

LME Aluminum 3M settled at $2,478.43/mt, down $9.39/mt on the week. Aluminum prices were down this week. Compared to last week, the futures forward curve remains in a contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 19¢/lb this week. The CME Midwest Premium market is now in a contango from the June ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $9,795.24/mt, down $339.26/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted vertically lower and is in contango throughout 2024 and early 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $17,082.21/mt, down $41.97/mt on the week. As prices were down this week, nickel’s forward curve also shifted lower. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $675/T, down $7/T on the week.

|

|||||

|

|

|||||

AEGIS Insights |

|||||

|

5/29/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 5/2/2024: Important U.S. Economic Data (AEGIS Reference) 4/25/2024: Mexico's New Tariffs on Steel and Aluminum Imports Create Uncertainty in U.S. Markets 2/27/2024: Aluminum Consumers Should Still Implement Hedges, Even Though Russia Sanctions Mean Little |

|||||

Notable News |

|||||

|

5/29/2024: Anglo rejects BHP's last-ditch attempt to continue takeover talks 5/27/2024: India's NALCO tops Q4 profit estimates on lower input costs 5/24/2024: India's Hindalco beats Q4 profit view as lower costs outpace weak aluminium prices |

|||||