|

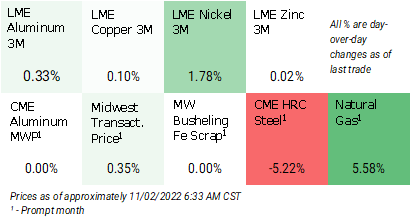

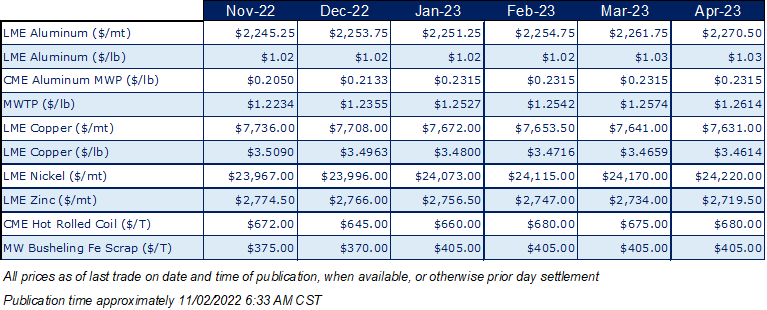

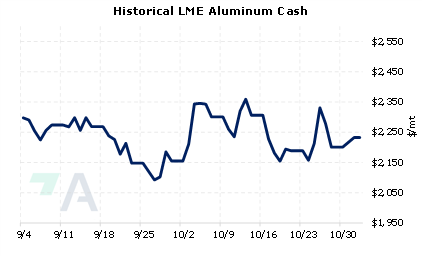

Starting in mid-November, three aluminum smelters in China’s Henan province will curtail approximately 110,000 mt of combined annual capacity due to unprofitability and pollution controls, according to Bloomberg and Shanghai Metal Market. AEGIS notes that this unprofitability likely stems from soaring electricity costs due to low hydropower supply across several key Chinese aluminum production regions. According to Shanghai Metal Market, production costs for Henan’s province smelters exceed 19,000 yuan/mt, or $2,618/mt. This compares to LME aluminum prices, which are $2,232.50/mt in the cash (November 1 settle) and $2,255/mt in the 3M Select (7:35 AM CST). Henan province has approximately 2 million mt of aluminum smelting annual capacity, representing nearly 5% of the country’s total. (Source: Bloomberg, Shanghai Metal Market) |

|

|

|

AEGIS notes that these curtailments are the latest in a growing list of cutbacks by Chinese aluminum producers. In mid-September, Shanghai Metal Market reported that aluminum smelters in Yunnan province might cut production by 20 to 30%, or 1 to 1.5 million mt, far more than the 500,000 mt reduction requested by local authorities. We also note that Chinese aluminum production continues at a blistering pace, despite the recent curtailments. Aluminum production averaged over 114,000 mt/day in September, a new record daily volume; however, total monthly production was 3.42 million mt last month, down slightly from the record 3.51 million mt in August, according to China’s National Bureau of Statistics. Will more production cuts cause LME aluminum prices to rally? Prices are down nearly 20% in 2022, as the last trade on the 3M Select contract was $2,255/mt (7:35 AM CST). Aluminum end-users might consider using the recent dip in prices by applying simple hedges involving swaps and call options. Such positions are standard for consumer hedging, but they can result in opportunity costs or cash costs if metal prices decrease. Please contact AEGIS for specific strategies that fit your operations. (11/2/2022) |

||

|

|

||

Note: Clients with AEGIS Platform access can see this and other research, plus hedge portfolio reporting and tools here. |

||

|

|

||

Price Indications |

||

|

|

||

|

|

||

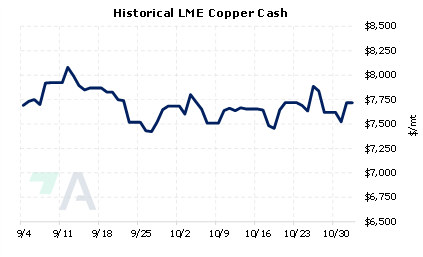

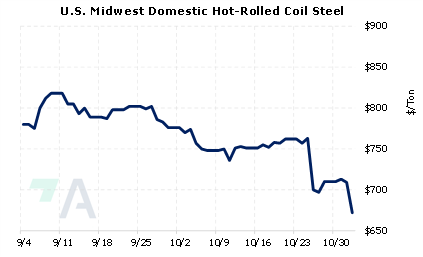

Today's Charts |

||

|

|

|

|

|

|

AEGIS Insights |

||

|

10/26/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 10/05/2022: European Aluminum Smelters Might Have Negative Margins Through 2023 8/31/2022: Will Chilean Production Issues Drive Copper Prices Higher? |

||

|

|

||

| Important Headlines | ||

|

11/2/2022: UK sanctions four Russian steel and petrochemical tycoons 11/1/2022: US HRC: Prices continue to fall, market weak 10/31/2022: China shows the LME there are still buyers for Russian metal 10/31/2022: LME Week: Nickel market looks for stability 10/28/2022: Ford North American sales fall sequentially 10/28/2022: Glencore cuts zinc output guidance after production drops 18% in nine months 10/27/2022: US Steel earnings, steel production drop 10/27/2022: Glencore to stick with Rusal's aluminium in 2023 -sources |

||

|

|

||

|

Important Disclosure: Indicative prices are provided for information purposes only, and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee to the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as “edge,” “advantage,” “opportunity,” “believe” or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.

|

||