|

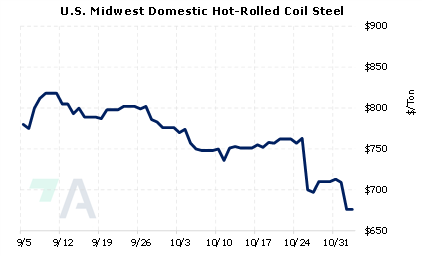

Argus's weekly US HRC assessment, which is now at $709.75/st, fell $26.50/st this week. This assessment has fallen nearly 8.5% since October 4, as the market contends with falling demand. Steel service centers believe demand will stay subdued into the final months of 2022, according to Argus reports. For example, appliance maker Whirlpool recently stated they cut output by 35% last quarter due to an expected cutback in consumer demand into 2023. |

|

|

|

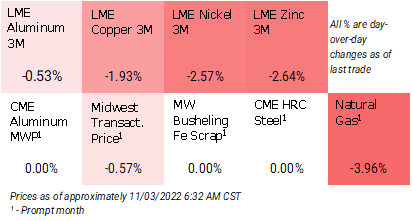

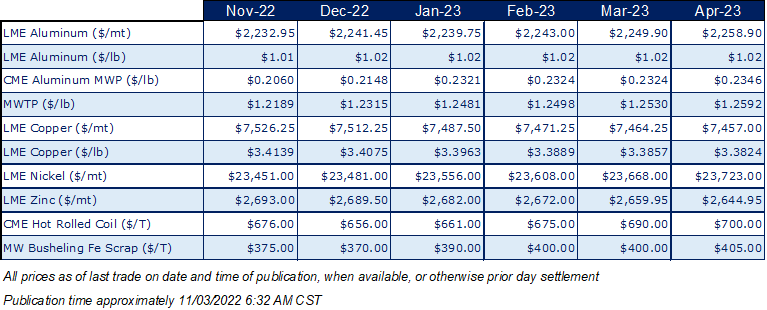

As for supply, steelmakers keep increasing output. Last week, AEGIS commented that Cleveland Cliffs will increase production by 300,000 to 400,000 st in 4Q, even though automotive demand only increased by 100,000 in 3Q. Oversupply continues to be a “top issue” for the industry, as more supply will come online in the next six months. However, there is potential for supply issues in the coming months. US Steel and the United Steelworkers are currently negotiating a new contract to replace one that expired in September, and unnamed sources cited by Argus believe that a potential strike by the United Steelworkers (USW) could be “the only action that could turn around the market, save increased production cuts by steelmakers.” (Source: Argus) The currently oversupplied steel market has pressured steel prices lower, as the prompt month (November) CME HRC futures are down nearly 56% from the highs of mid-March, as the last settle was $676/st (7:00 AM CST). This could be a good time for steel end-users to hedge future needs into 2023 by buying HRC swaps. Using swaps converts a variable cost into a fixed cost, thereby ‘locking in’ a price for the hedged steel. Since HRC swaps are thinly traded, we suggest using limit orders to establish a specific steel price. Such positions are standard for consumer hedging; however, they can result in opportunity costs or cash costs if metal prices decrease. Please contact AEGIS for specific strategies that fit your operations. (11/3/2022) |

||

|

|

||

Note: Clients with AEGIS Platform access can see this and other research, plus hedge portfolio reporting and tools here. |

||

|

|

||

Price Indications |

||

|

|

||

|

|

||

Today's Charts |

||

|

|

|

|

|

|

AEGIS Insights |

||

|

11/02/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 10/05/2022: European Aluminum Smelters Might Have Negative Margins Through 2023 8/31/2022: Will Chilean Production Issues Drive Copper Prices Higher? |

||

|

|

||

| Important Headlines | ||

|

11/3/2022: Alcoa sent three letters to the LME requesting action on Russian metal 11/2/2022: UK sanctions four Russian steel and petrochemical tycoons 11/1/2022: US HRC: Prices continue to fall, market weak 10/31/2022: China shows the LME there are still buyers for Russian metal 10/31/2022: LME Week: Nickel market looks for stability 10/28/2022: Ford North American sales fall sequentially 10/28/2022: Glencore cuts zinc output guidance after production drops 18% in nine months 10/27/2022: US Steel earnings, steel production drop 10/27/2022: Glencore to stick with Rusal's aluminium in 2023 -sources |

||

|

|

||

|

Important Disclosure: Indicative prices are provided for information purposes only, and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee to the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as “edge,” “advantage,” “opportunity,” “believe” or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.

|

||