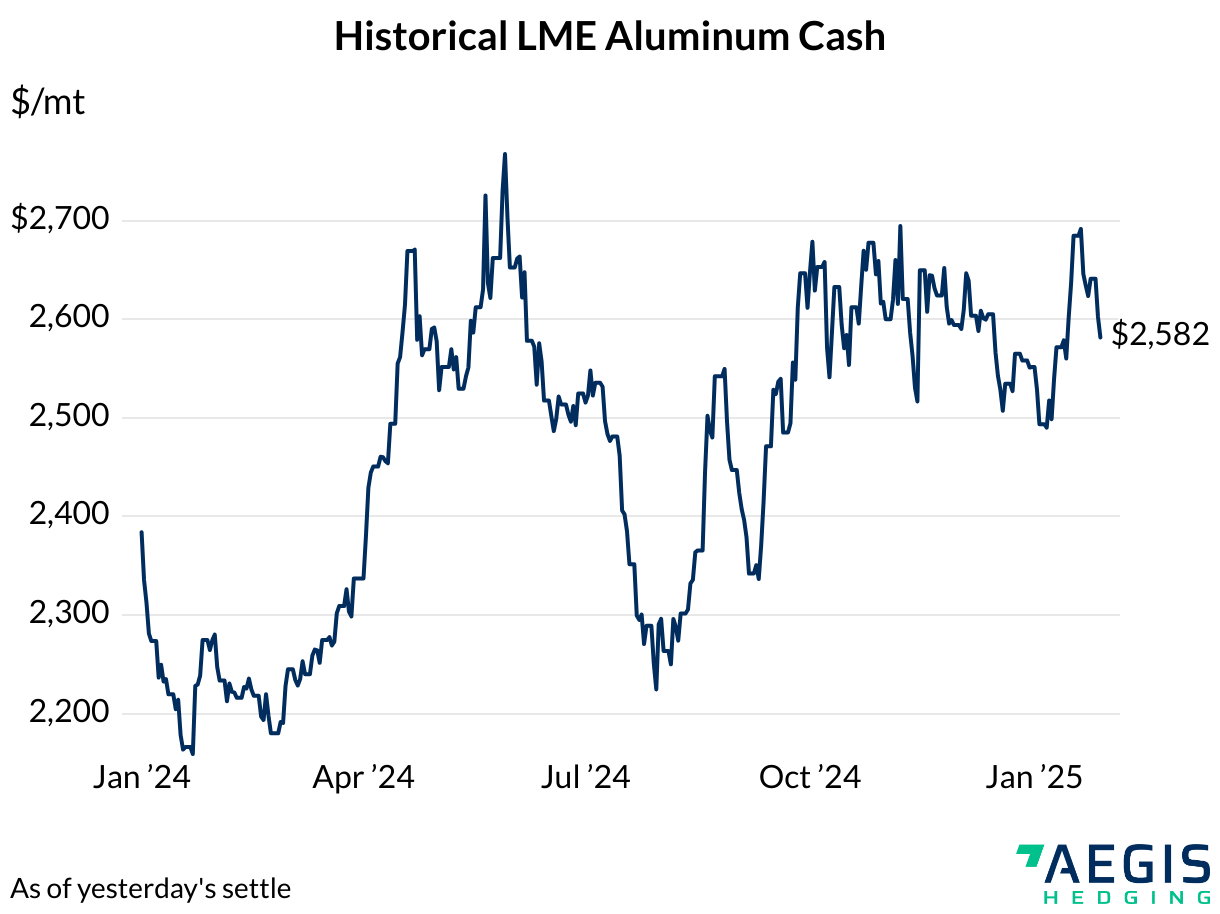

- LME Aluminum 3M Select is modestly up $17.96/mt to $2,297/mt, extending Tuesday's gains (8:30 AM CST)

- Base metal prices, including copper and aluminum, have declined following a strong rally earlier in 2024 due to weak demand and economic uncertainty. However, BofA Securities suggests that further downside is likely limited, with factors such as potential Federal Reserve rate cuts, a post-summer demand rebound, and resolution of trade disputes expected to support prices into 2025. Despite a global slowdown in manufacturing activity, physical markets remain tight, with high copper premiums in the U.S. and Europe. BofA anticipates that easing monetary policy and sustained investment in green technologies will provide additional support for base metal prices. (Investing.com)

- China's aluminum output surged to 3.68 million metric tons in July, marking the highest monthly production in over two decades, as producers ramped up operations to capitalize on strong profits despite recent price declines. This 6% year-on-year increase was driven by new projects in Inner Mongolia and sustained production in other key regions. The aluminum industry saw profits peak at 4,000 yuan per ton in June, the highest since early 2022, prompting smelters to boost output. Although prices have since fallen due to profit-taking and weak demand, production is expected to continue rising in the coming months. (Reuters)

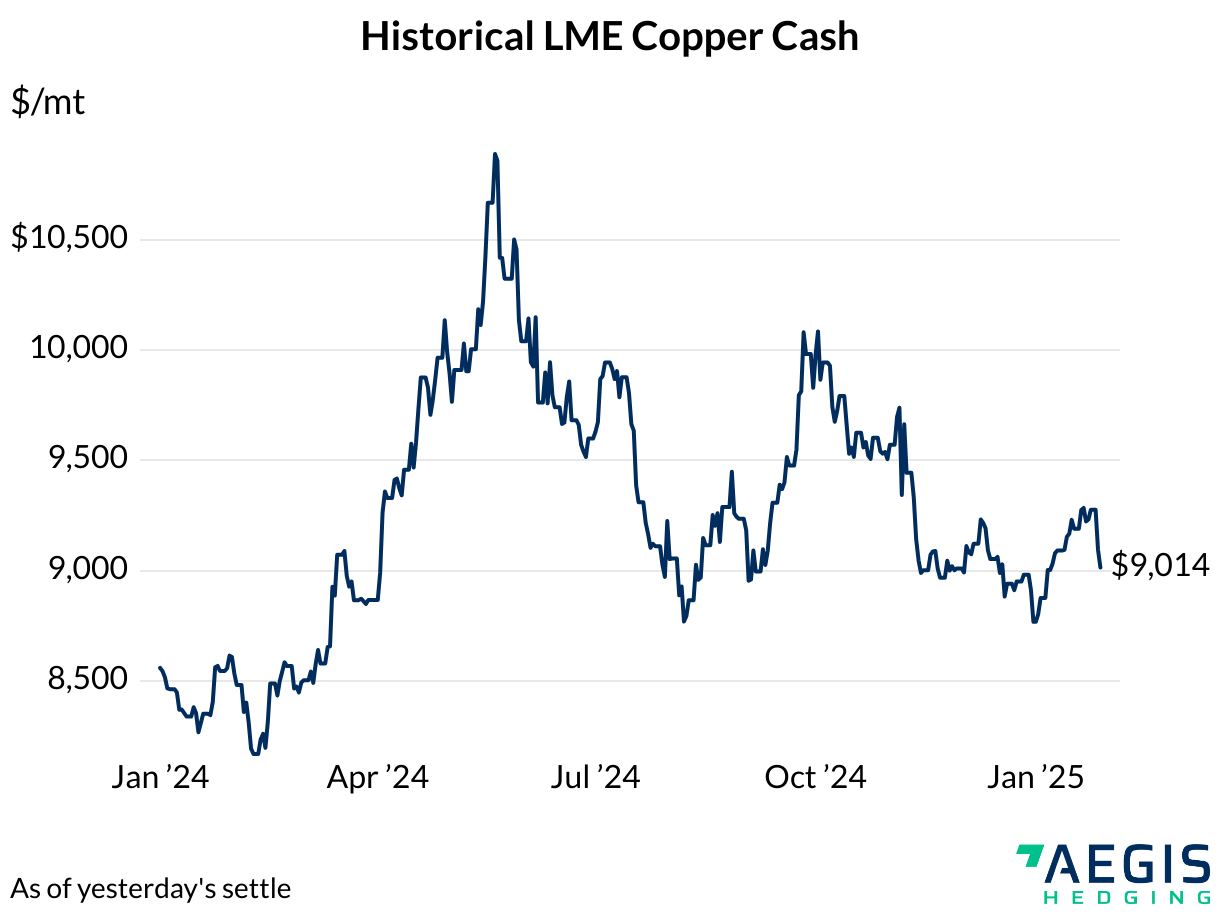

- LME Copper 3M Select is up $153.2/mt to $9,017/mt, as prices trade higher from yesterday (8:30 AM CST)

-

-

Copper prices climbed for a second day, rising 1.4% to $9,095.50 a ton on the London Metal Exchange, as traders balanced weak Chinese economic data against supply disruptions from the ongoing strike at BHP Group’s Escondida mine in Chile, the world’s largest copper mine. Despite China's industrial output slowing and retail sales growth remaining tepid, the risk of unplanned supply disruptions from unresolved wage discussions in Chile is supporting prices. Meanwhile, China’s property market showed slight improvement in July, and aluminum output hit a record high as smelters increased production. (Source: Bloomberg)

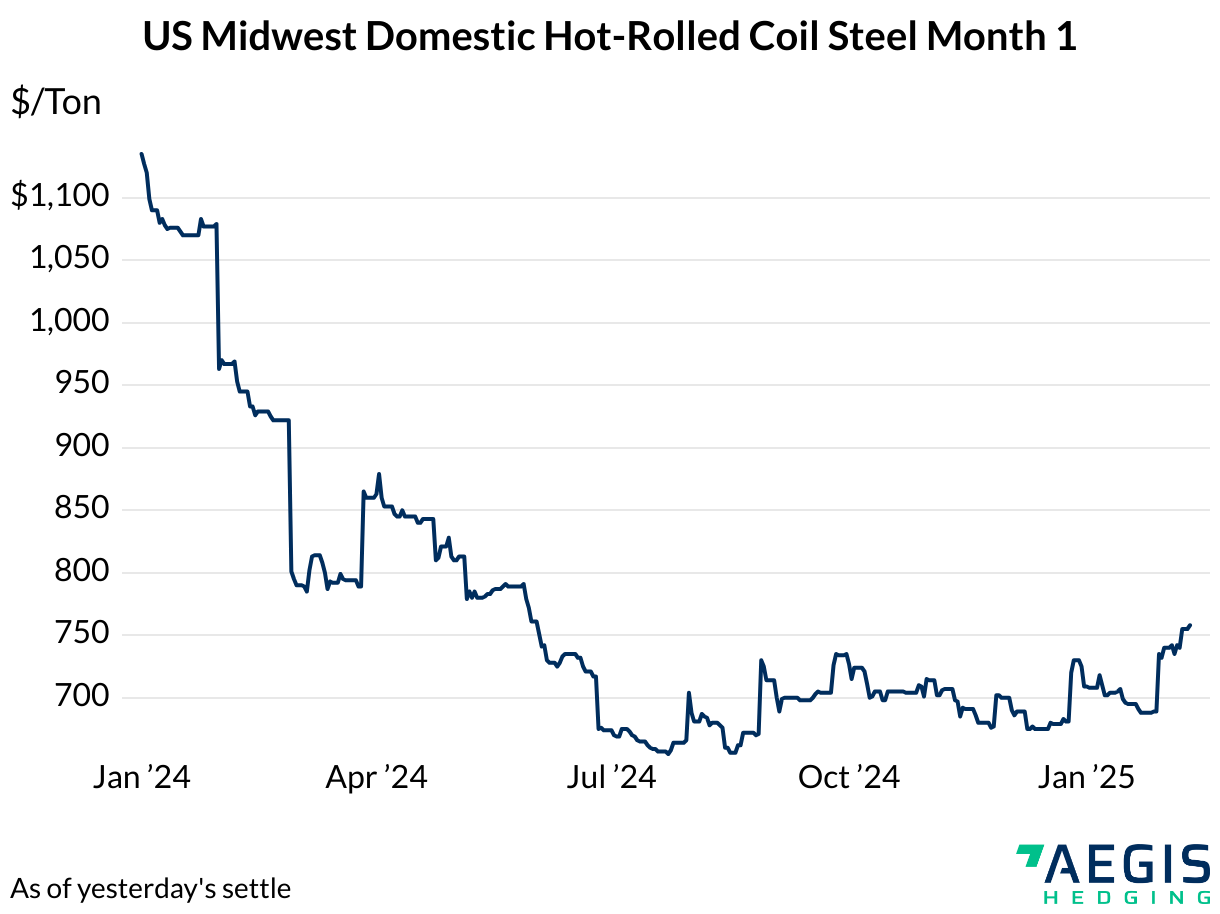

- Prompt month CME HRC Steel last traded at $656/st, extending losses for a fourth straight day

- Chinese steelmakers cut production by 9% in July, the lowest level reported in 2024, as plummeting demand and collapsing margins forced the industry to scale back. The ongoing real estate downturn and shrinking factory activity have driven domestic steel prices to multi-year lows, sparking trade tensions as Chinese metal floods global markets. With new quality standards and government efforts to cap production, further output cuts are expected in August. Meanwhile, oil refiners face similar challenges as Beijing pivots to renewable energy, and hydropower's rise continues to pressure thermal generation, lifting aluminum production in hydro-rich regions. (Source: Bloomberg)

|

|

Important Disclosure: Indicative prices are provided for information purposes only, and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee to the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as “edge,” “advantage,” “opportunity,” “believe” or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.

|