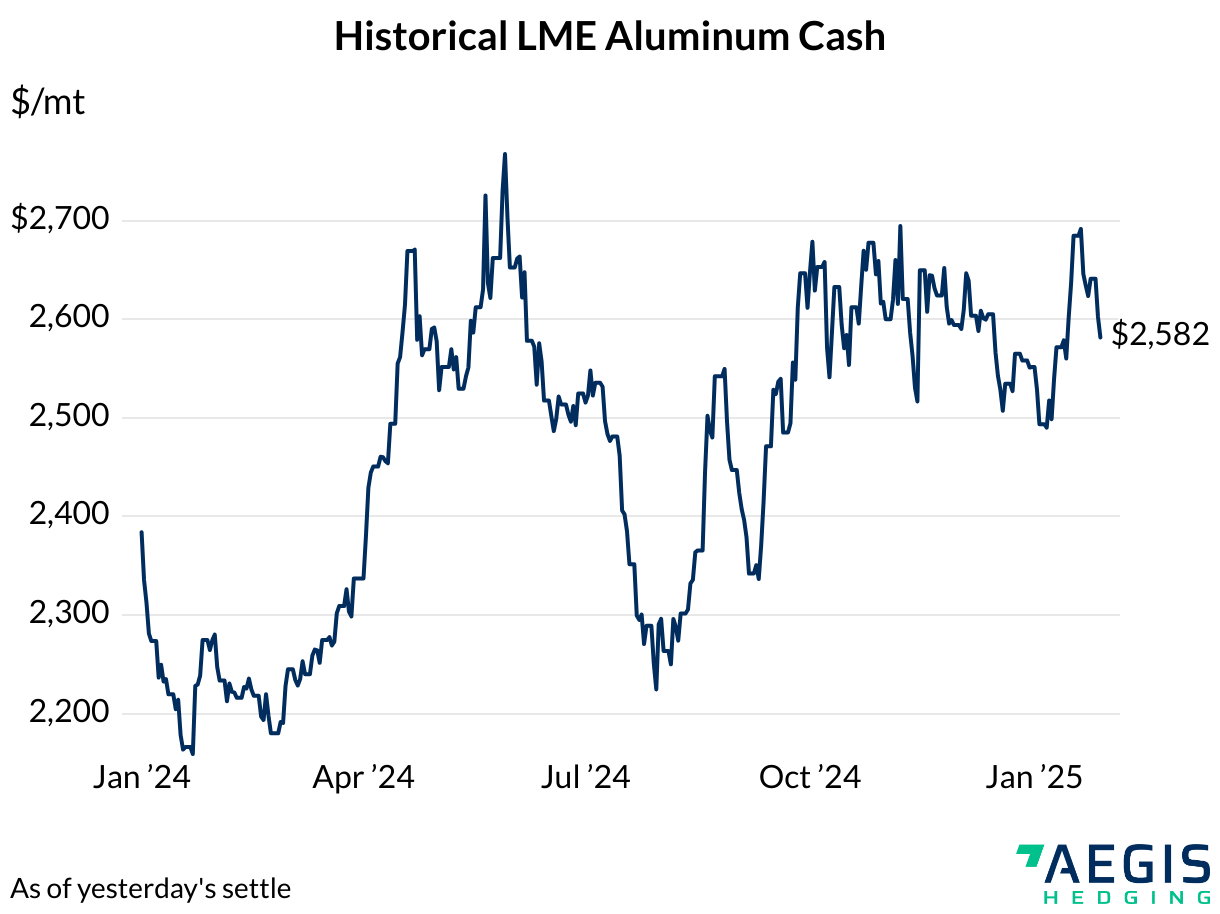

- LME Aluminum 3M Select is trading $50.87 lower to $2,479.5/mt, as prices erase some of last week's gains (9:15 AM CDT)

- Aluminum prices fell from a two-month high as inventories rose in China, the world’s largest market, signaling weak demand amid the country's economic challenges. Despite a nearly 10% gain in August, driven by a weakening US dollar and anticipation of Federal Reserve rate cuts, aluminum stockpiles in China have reached their highest level for this time of year since 2019, with a 0.5% increase to 807,000 tons. This rise halted a prior decline in inventories, pushing prices down 1.7% on the LME. Broader declines in industrial metals were observed as Chinese demand struggled due to a property market slowdown and weak economic confidence. Expectations remain for demand to pick up as manufacturing activity increases in the coming months. (Bloomberg)

- Meanwhile, market participants are closely watching potential responses from the LME to complaints about sharp fee hikes at a major warehouse operator, which some traders believe are distorting the global aluminum market.

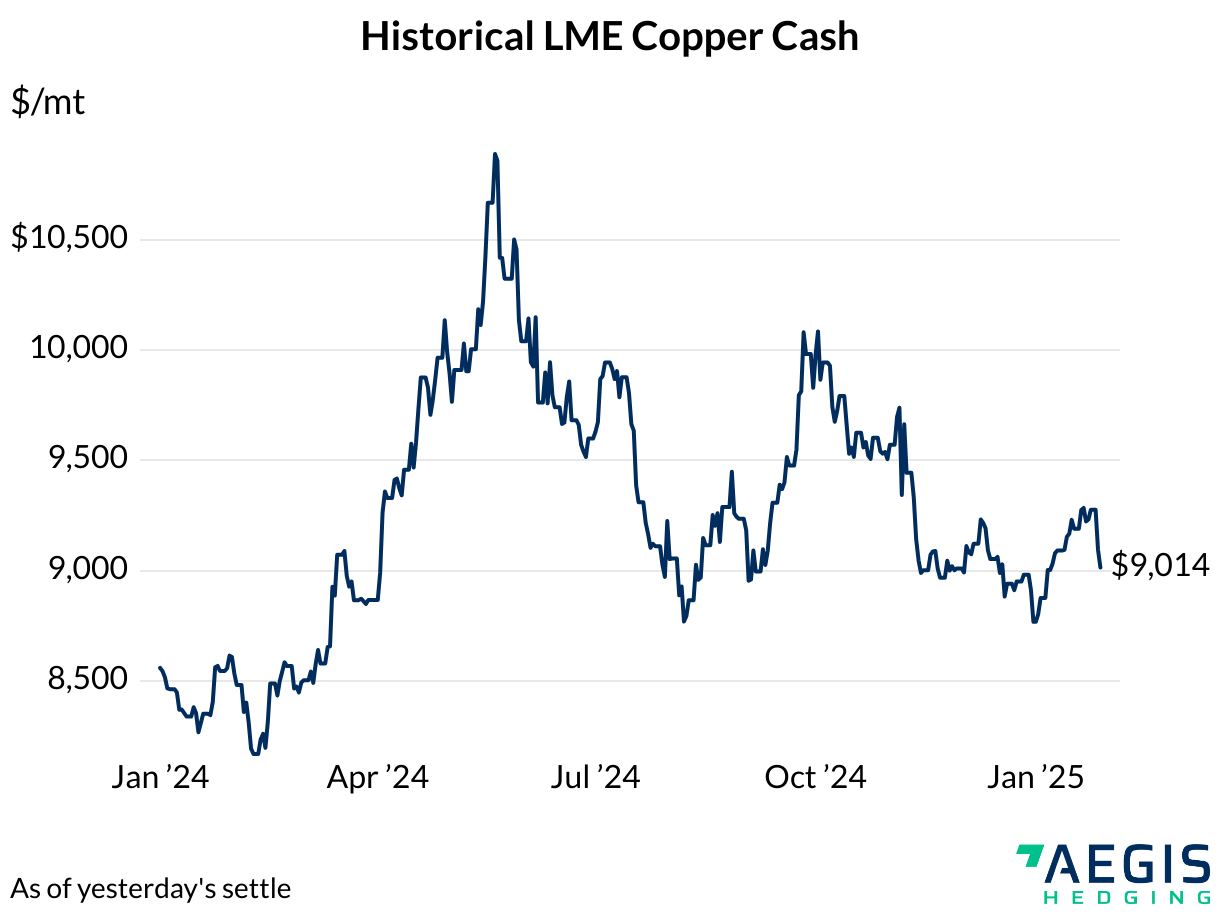

- LME Copper 3M Select trades $191.52 lower at $9,135/mt, reversing yesterday's gains (9:15 AM CDT)

- Jiangxi Copper, China's largest refined copper producer, expects the global copper ore shortage to persist into the second half of the year, maintaining downward pressure on processing fees. The company highlights that Chinese smelters, which produce over half of the world’s refined copper supply, are facing rising certainty of prolonged mine supply constraints as processing capacity outstrips ore availability. This has driven processing fees to near or below zero since April. Despite higher copper prices boosting its first-half net income, the company anticipates that the tight ore supply and low fees will remain challenges in the coming months, affecting the broader industry outlook.(Bloomberg)

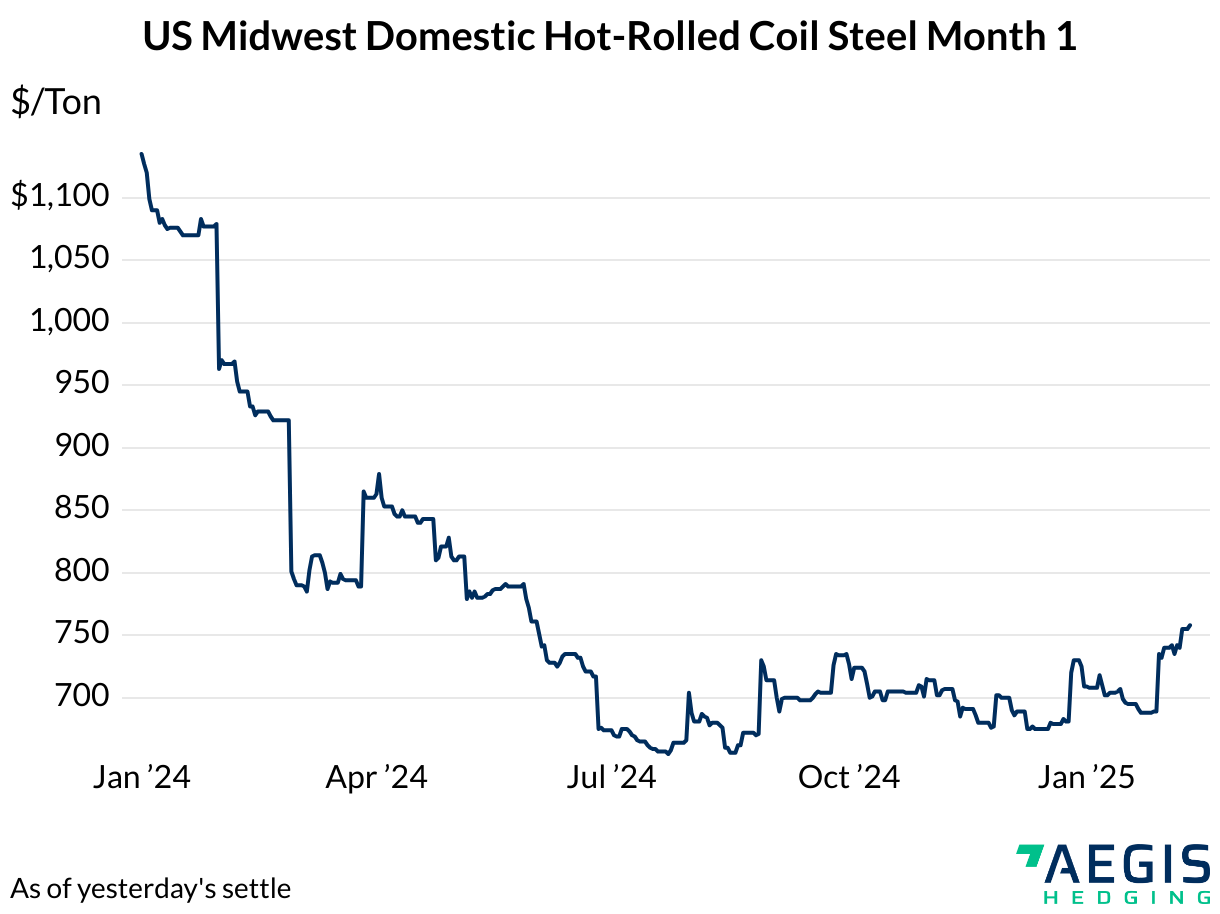

- Prompt month CME HRC Steel last traded at $730/st, as prices rallied $59 to highest since June

- China's steel industry is expected to face worsening challenges as both BHP Group, the world's largest miner, and China Baowu Group, the top iron ore buyer, express concerns over declining demand. The slowdown, driven by a prolonged property crisis and weakening economic conditions, has already led to a more than 10% drop in steel demand since 2020, marking an end to a decades-long boom. Benchmark steel prices have plunged to multi-year lows, with Chinese mills struggling amid oversupply, high costs, and fierce competition. BHP maintains that China’s steel production has plateaued above 1 billion tons and expects this trend to continue into the mid-2020s. As a result, BHP is shifting focus towards copper, anticipating increased demand due to the energy transition. Despite relatively stable profits in the first half, both BHP and Baosteel are bracing for further difficulties, particularly for smaller, higher-cost producers who are likely to bear the brunt of the downturn. (Bloomberg)

|

|

Important Disclosure: Indicative prices are provided for information purposes only, and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee to the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as “edge,” “advantage,” “opportunity,” “believe” or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.

|