Updated October 29, 2024

The Rocky Mountain region remains bifurcated, with the western Rockies better positioned to capitalize on winter price spikes due to its proximity to the West Coast and limited capacity in the basin moving east to west. Tame production growth shouldn’t threaten outbound pipeline capacity in the near future.

Price: Basis pricing in the Rockies has been improving over the past month even when taking out the effects of the contract rolling from October (end of Summer) to November (beginning of Winter). Both NWP Rockies basis and CIG Rockies basis has improved M-O-M in each of the next six seasons.

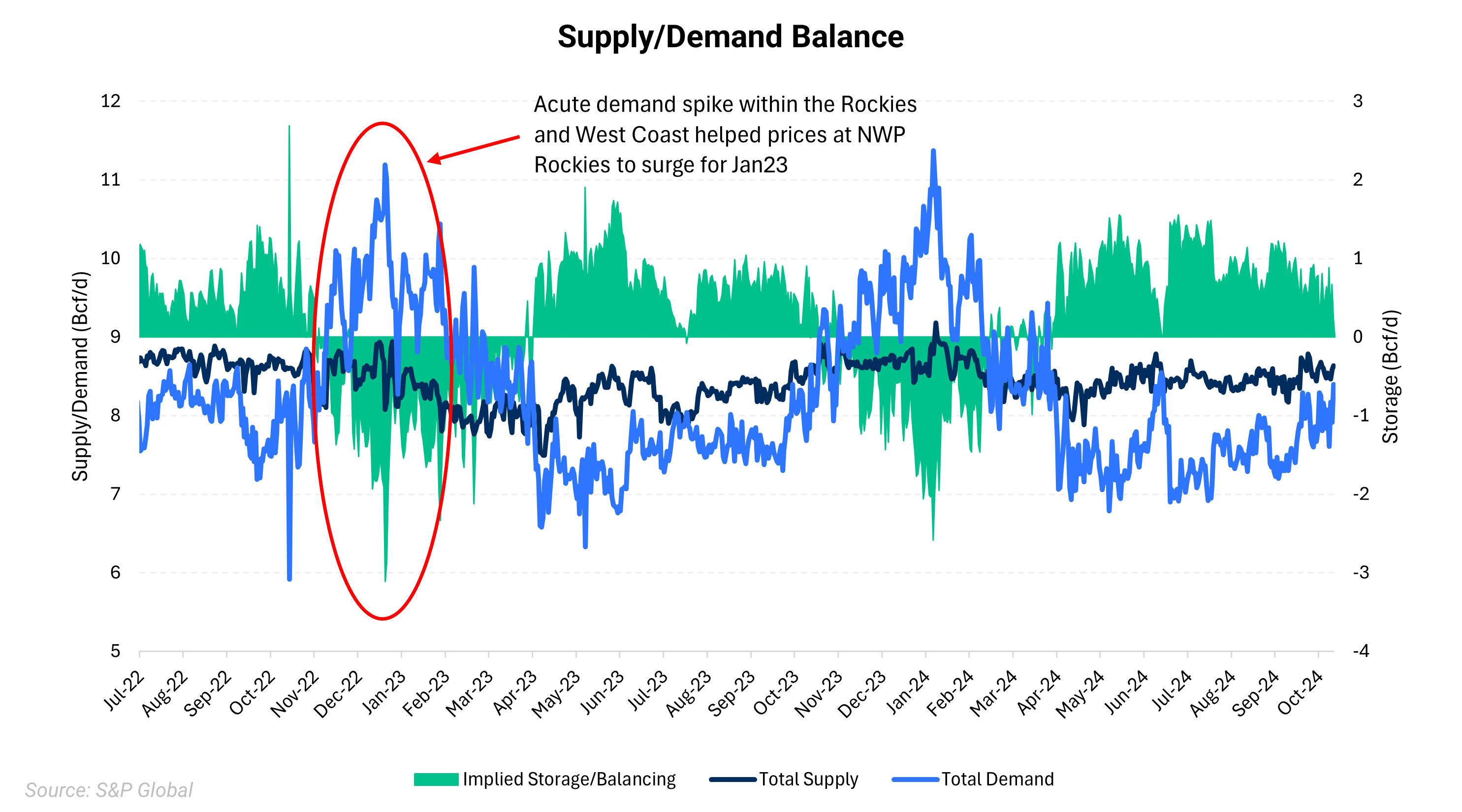

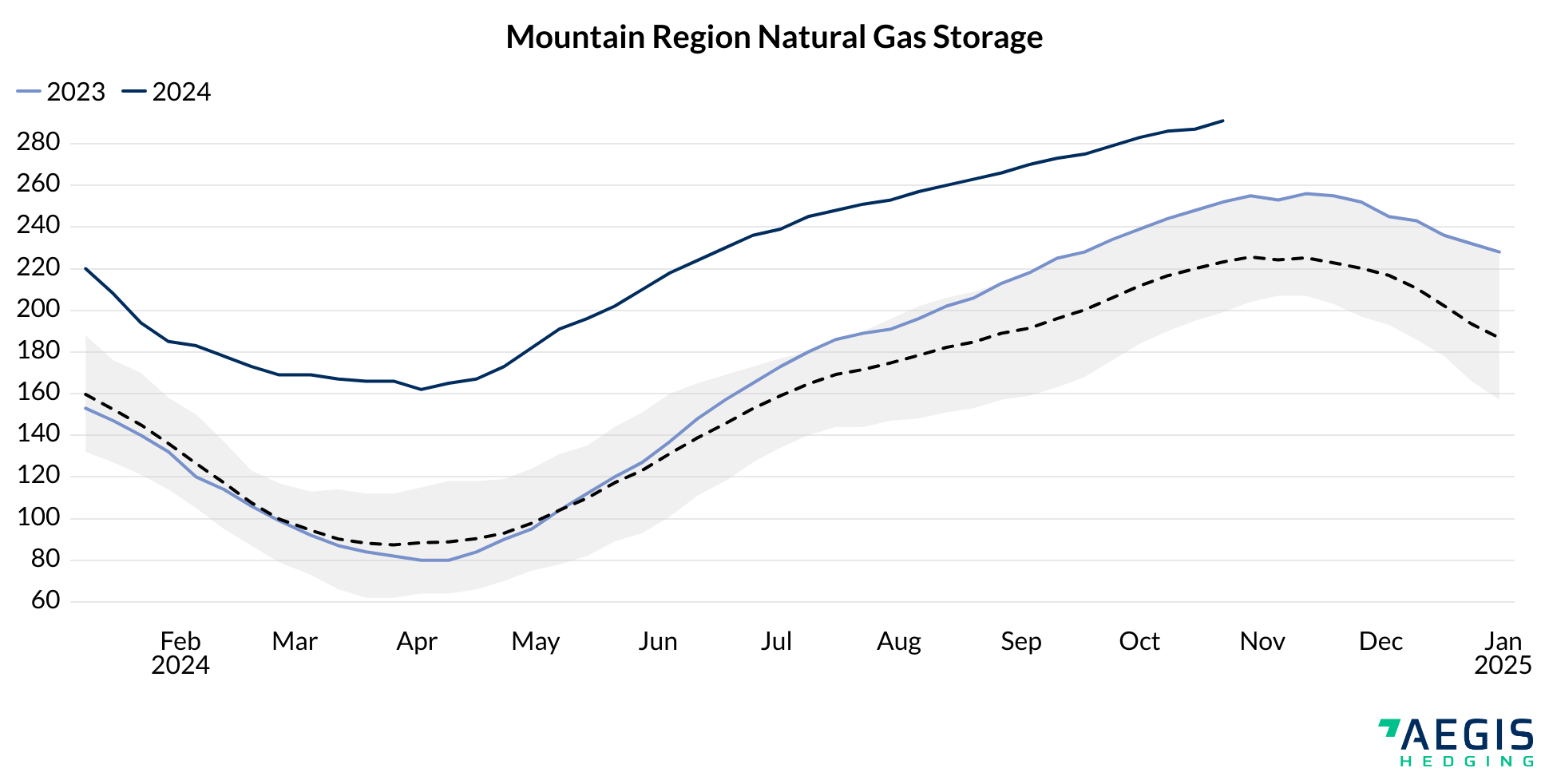

Risk: Supply-side risks should be relatively muted as production continues to lag available takeaway capacity. Following a lackluster Winter’23/’24, storage across the Rockies is elevated. The threat of a massive blowout like that in January 2023 has reduced in probability but remains a high-impact event for both producers and consumers.

News: 4/1/24 Kern River Gas Transmission completed the Delta Lateral Project. The project involved the construction of a 36-mile, 24-inch-diameter natural gas pipeline, which will “provide natural gas transportation from Kern River’s mainline near Holden, Utah, to a delivery point near Delta Utah,” according to the company’s website.

Supply/Demand Fundamentals: Tame production growth shouldn’t threaten outbound pipeline capacity in the near future. The basin continues to be split, as gas from the eastern half struggles to move westward. Production on the western half of the Rockies will continue to deal with more volatile pricing as it’s closely tied to western basin pricing.

Price |

||

|

The chart above displays basis (difference from Henry Hub), rather than outright price.

|

||

|

October 29, 2024 - The Nov24 NWP Rockies basis contract has seen a volatile couple of weeks as it heads into expiration. Prices traded as high as +$1.50 intraday 10/17 before selling off to +$0.60 on 10/25. As we stand currently, intraday on October 29, the November contract is trading +$0.85. The next handful of seasons have all gained over the past month from recent lows in mid-September. The full Winter 24-25 strip is currently $1.55, up 2.5% on the week and 13% since the beginning of October. The Summer 2025 strip has improved even more, gaining 26% W-o-W and 23% M-o-M, to trade -$0.235. Forward pricing on the eastern half of the basin continues to move higher. The prompt November contract is currently at its best prices in the past year, trading -$0.185 today. The full strips for Winter 24/25 and Summer 25 haven’t eclipsed price levels from the beginning of 2024, but both are well off their yearly lows in early June. Winter 24/25 is up to +$0.316 while Summer 25 is up to -$0.585.

|

||

Risk |

||

|

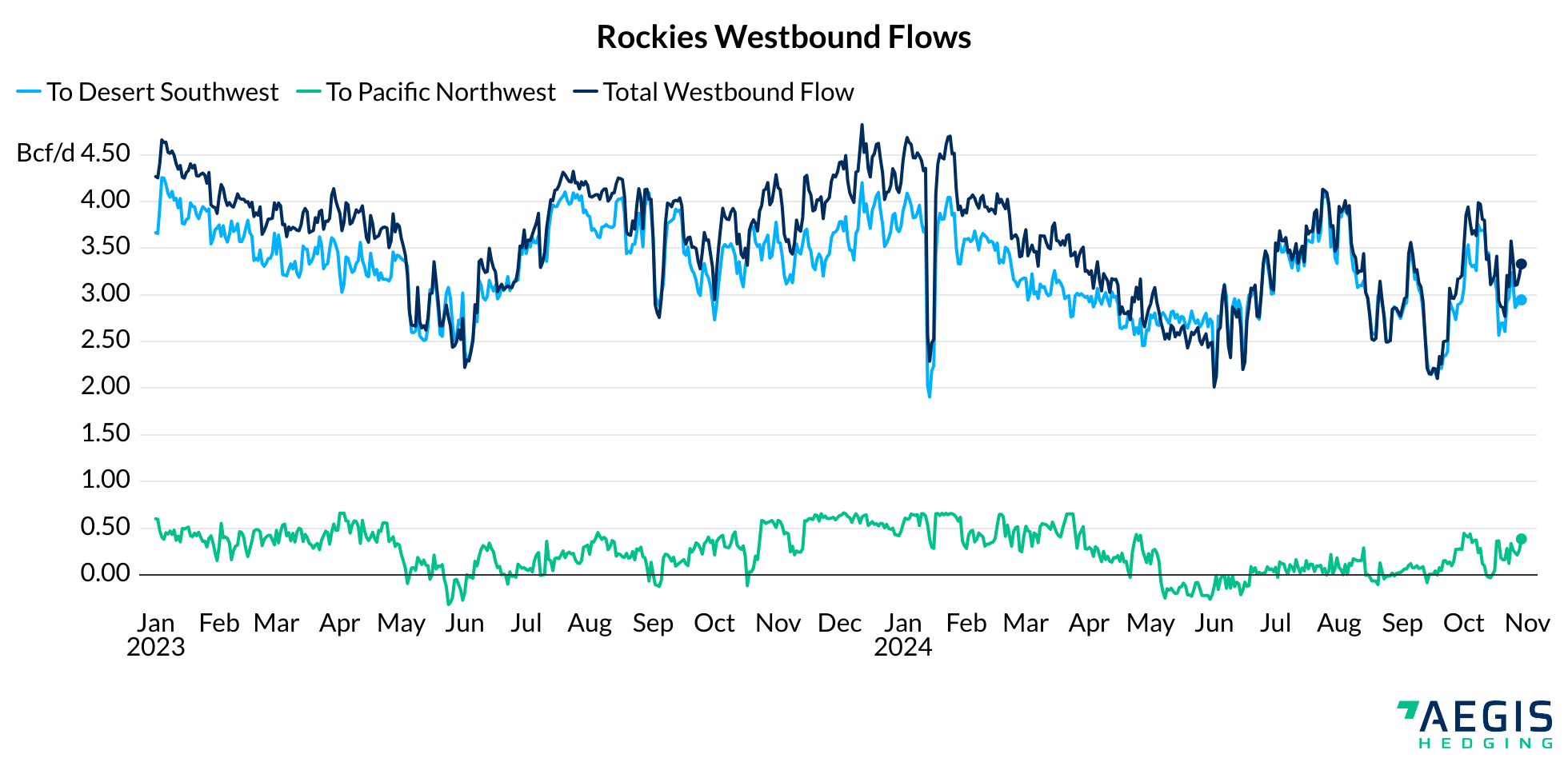

NWP-CIG Dynamics: Operators who produce in the western part of the Rockies near Opal, Wyoming, are typically exposed to pricing on Northwest Pipeline (NWP); the associated basis location is, known as NWP-Rox. The eastern half of the basin is primarily exposed to CIG/Cheyenne pricing. Both sides of the basin typically trade at a premium in the winter months and a discount in the summer. The major difference between NWP-Rox and CIG is that NWP-Rox can better participate in California and Pacific-Northwest (PacNW). There is a constraint for gas produced on the eastern Rockies to flow westward; therefore, NWP-Rox can trade at a material premium to CIG when there is an acute need for gas in the west and PacNW markets. |

||

| Rocky Mountain Gas Overview | ||

|

||

|

|

||

News |

||

|

||

Supply/Demand Fundamentals |

||

|

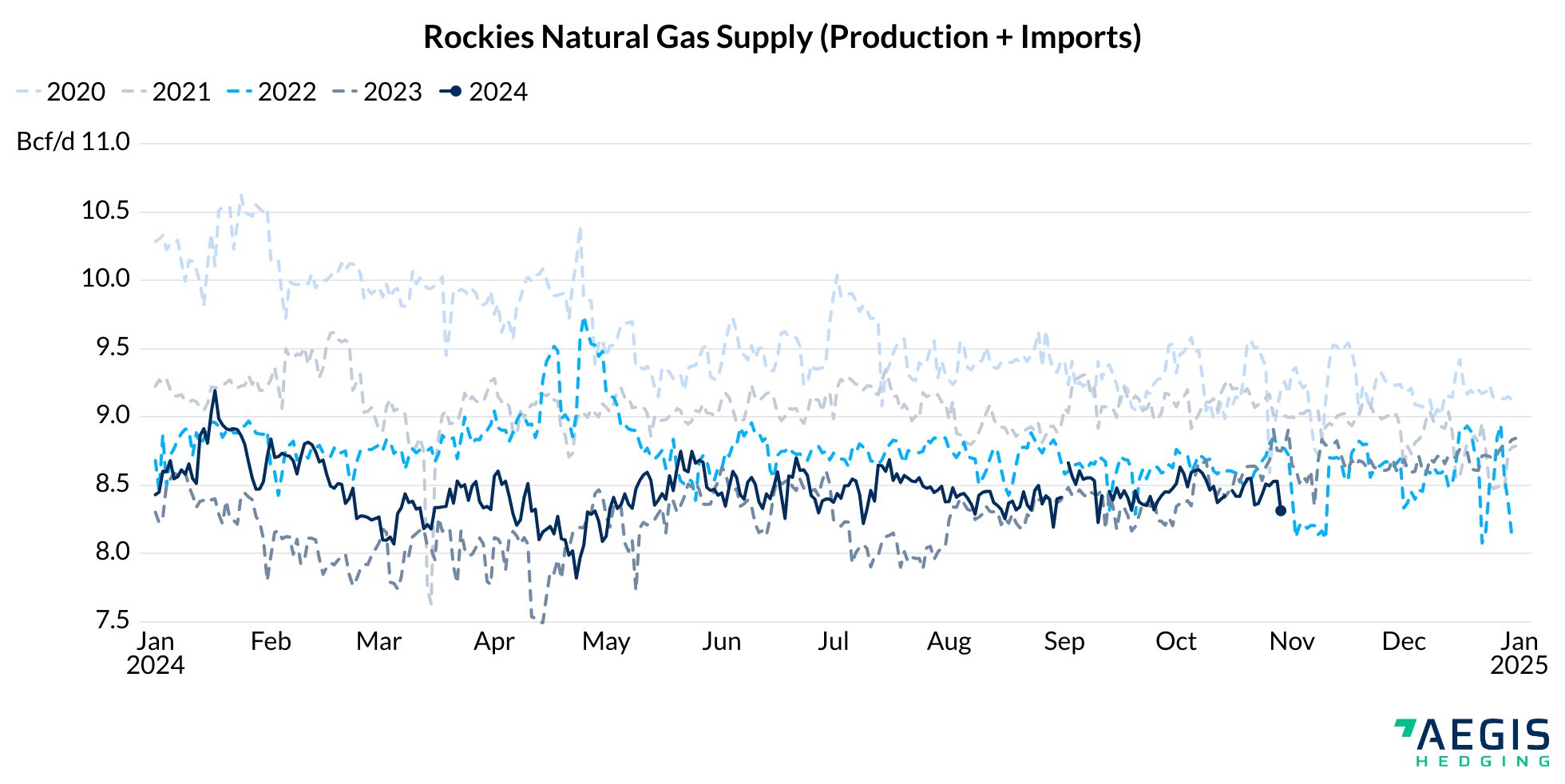

Supply/Demand Balance: Since the beginning of the year, the Rocky Mountain region has been oversupplied compared to recent history. Poor demand has been the major driver, as both production and Canadian imports have been muted for most of the year. The result has been regional storage levels tracking well above the 5-year and 10-year average. Currently storage levels are 31% higher than the 5-year average and 15% above the 5-year maximum. Historically, the supply/demand balance fluctuates throughout the year, with production outpacing demand in Summer (April-October) and flipping into a deficit in Winter (November-March). The seasonal nature of the supply/demand balance is seen in the basis pricing as Winter trades at a premium to Henry Hub and Summers at a discount. |

||

|

|

||

|

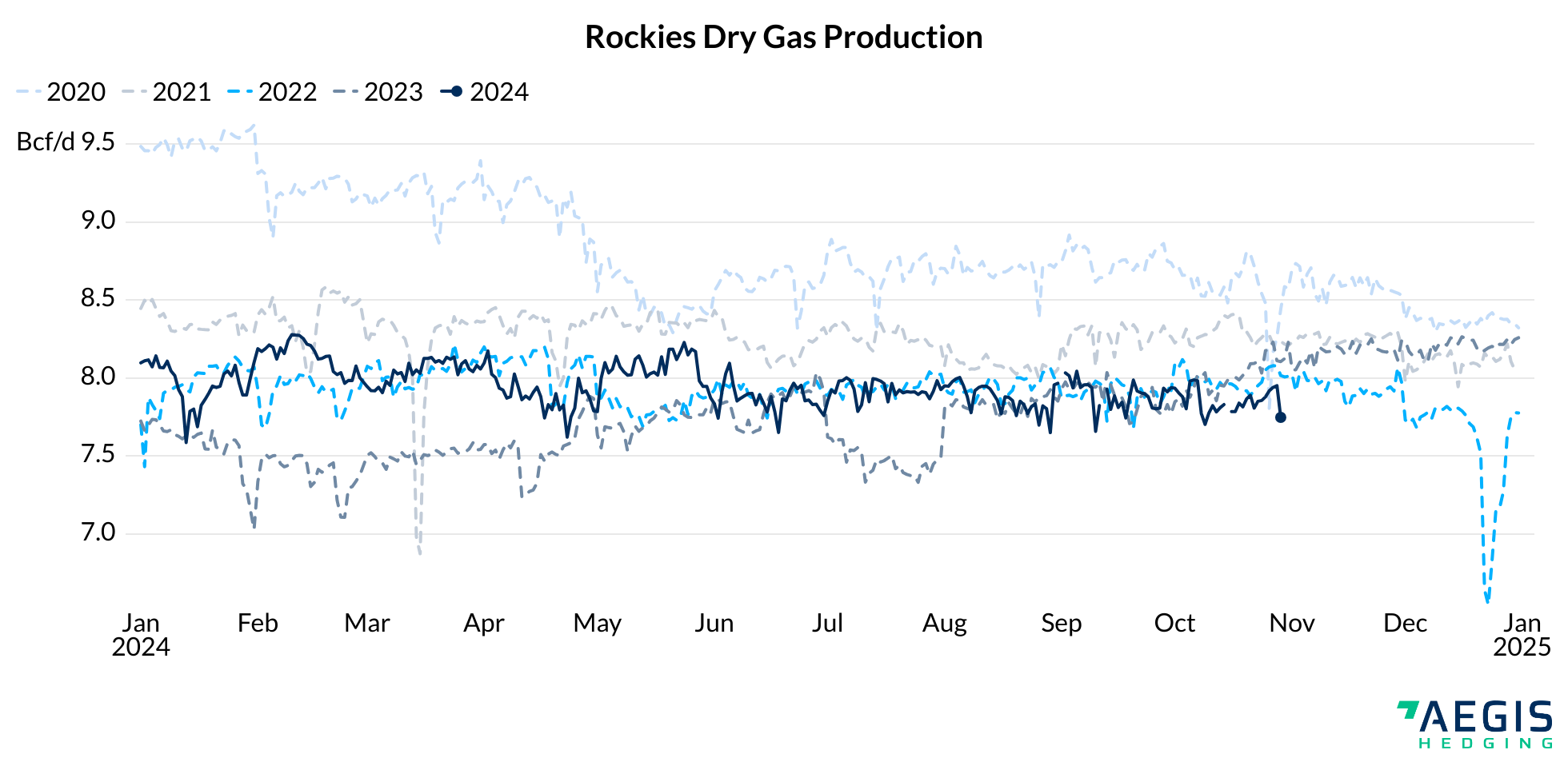

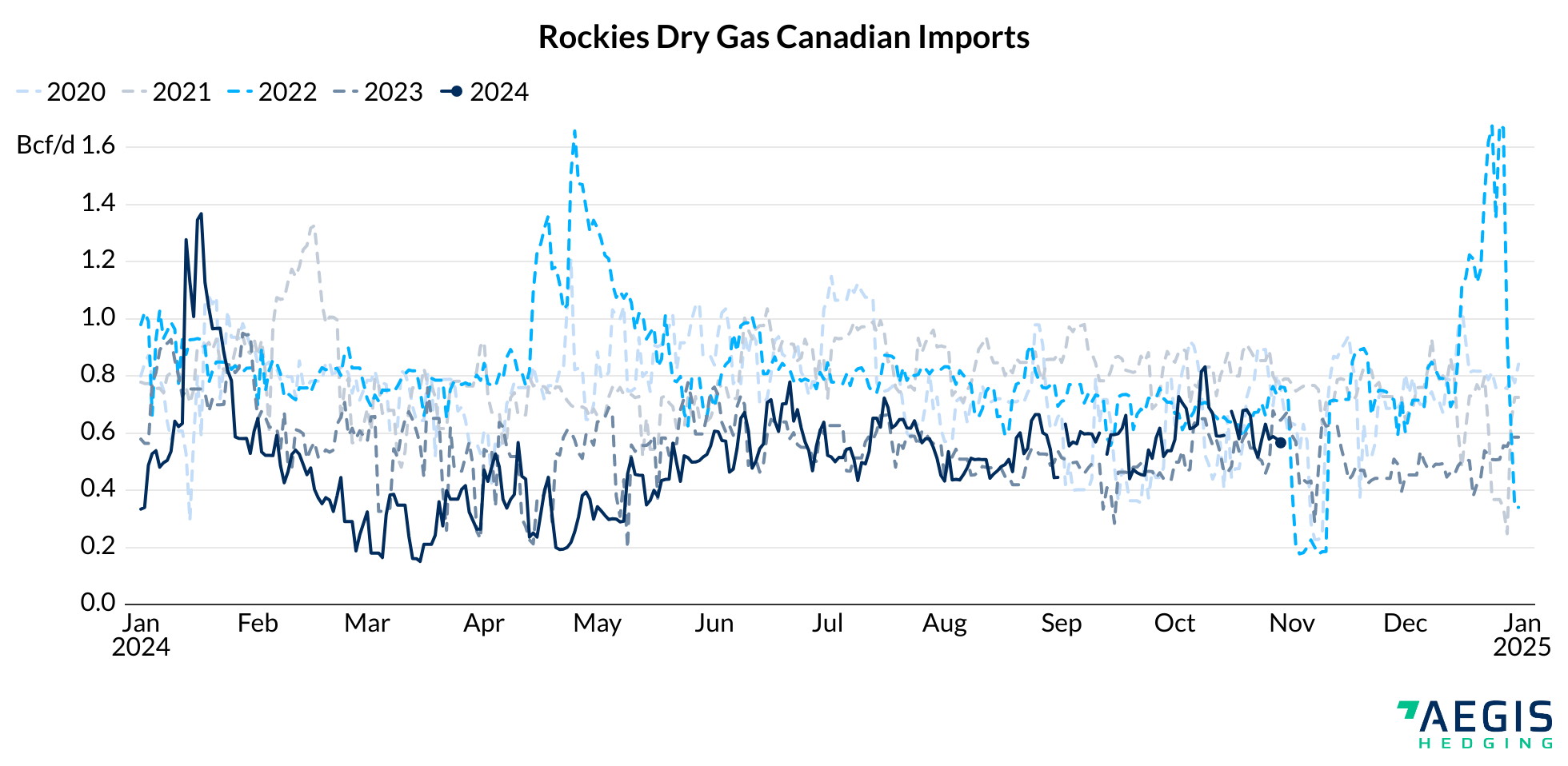

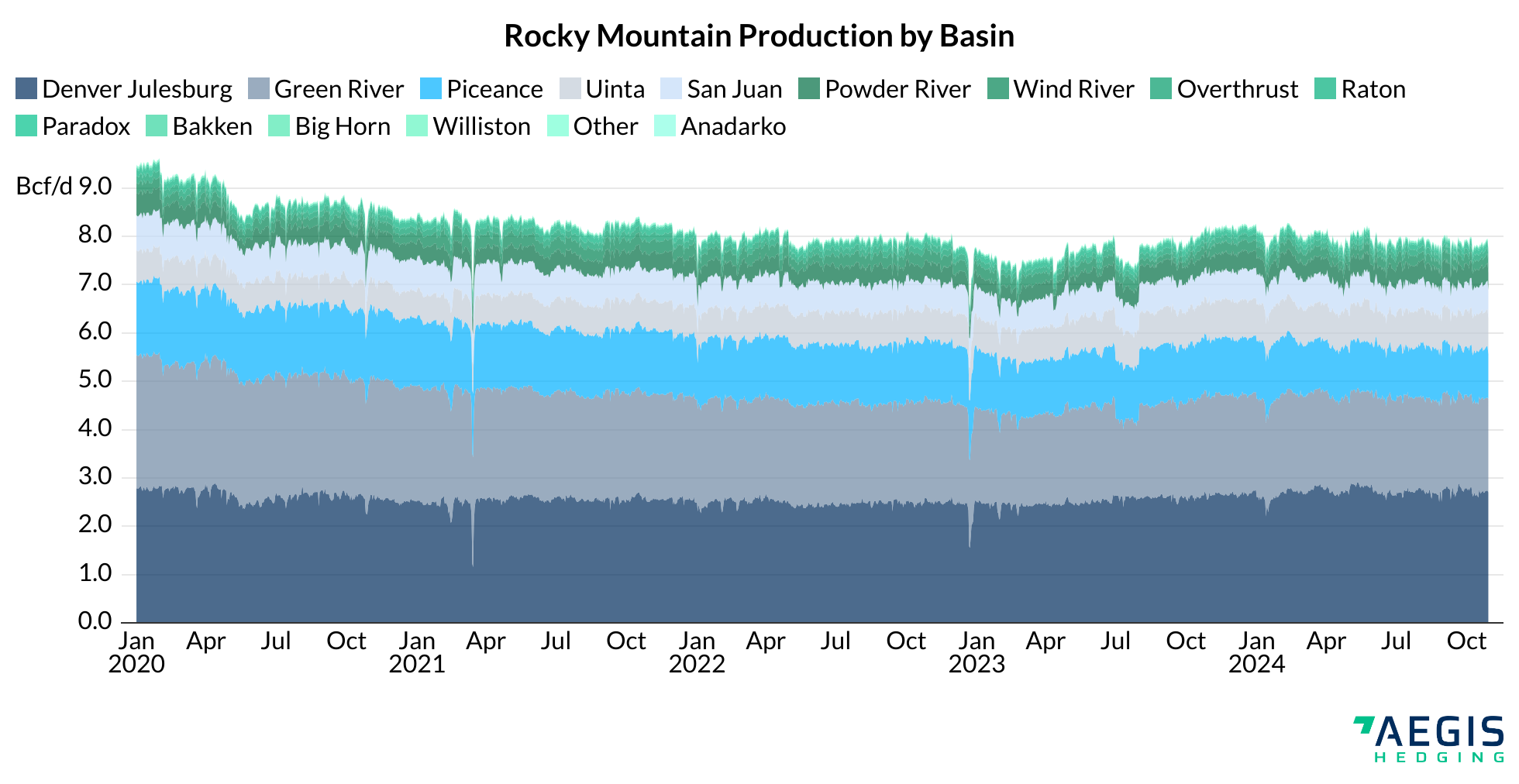

Gas Production: Total supply in the Mountain region continues to fluctuate around the 8.5 Bcf/d mark. Imports from Canada have ticked higher the past month, averaging 0.65 Bcf/d in October vs. 0.56 Bcf/d in September although these levels remain low compared to years past. Dry gas production has been very stable through much of the summer. October production has averaged 7.9 Bcf/d compared to an average of 7.88 Bcf/d from April 1 through October 25. Overall, Rockies dry gas production had been in decline since early 2020, as COVID-19-induced price declines caused operators to scale back activity. By the end of 2023, production had once again eclipsed 8 Bcf/d and continues near that level throughout 2024. The Denver Julesburg contributed to the largest growth over the past year, followed by the Uinta. |

||

|

Production is shown above by major producing regions in the Rockies. The increased focus on the DJ in the past few years has led to the shale play accounting for the largest portion of gas production in the region.

|

||

| Rig Count: Active rigs in the Rockies have generally been declining since 2009. The last three oil-price crashes have contributed to lower capital investment and, therefore, rig activity in the Rockies. The investment focus has turned to other basins. |

|

Source: Baker Hughes |

|

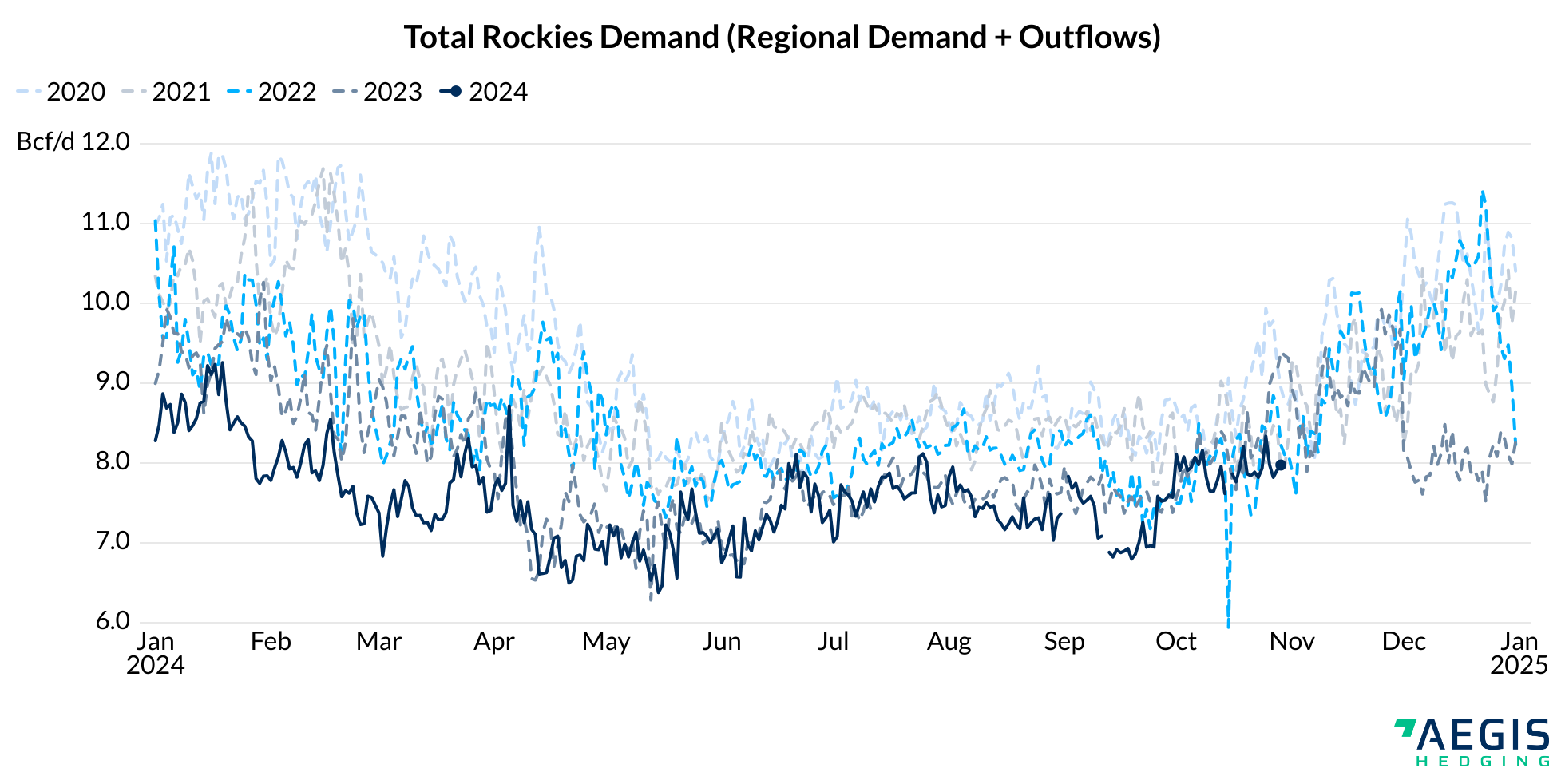

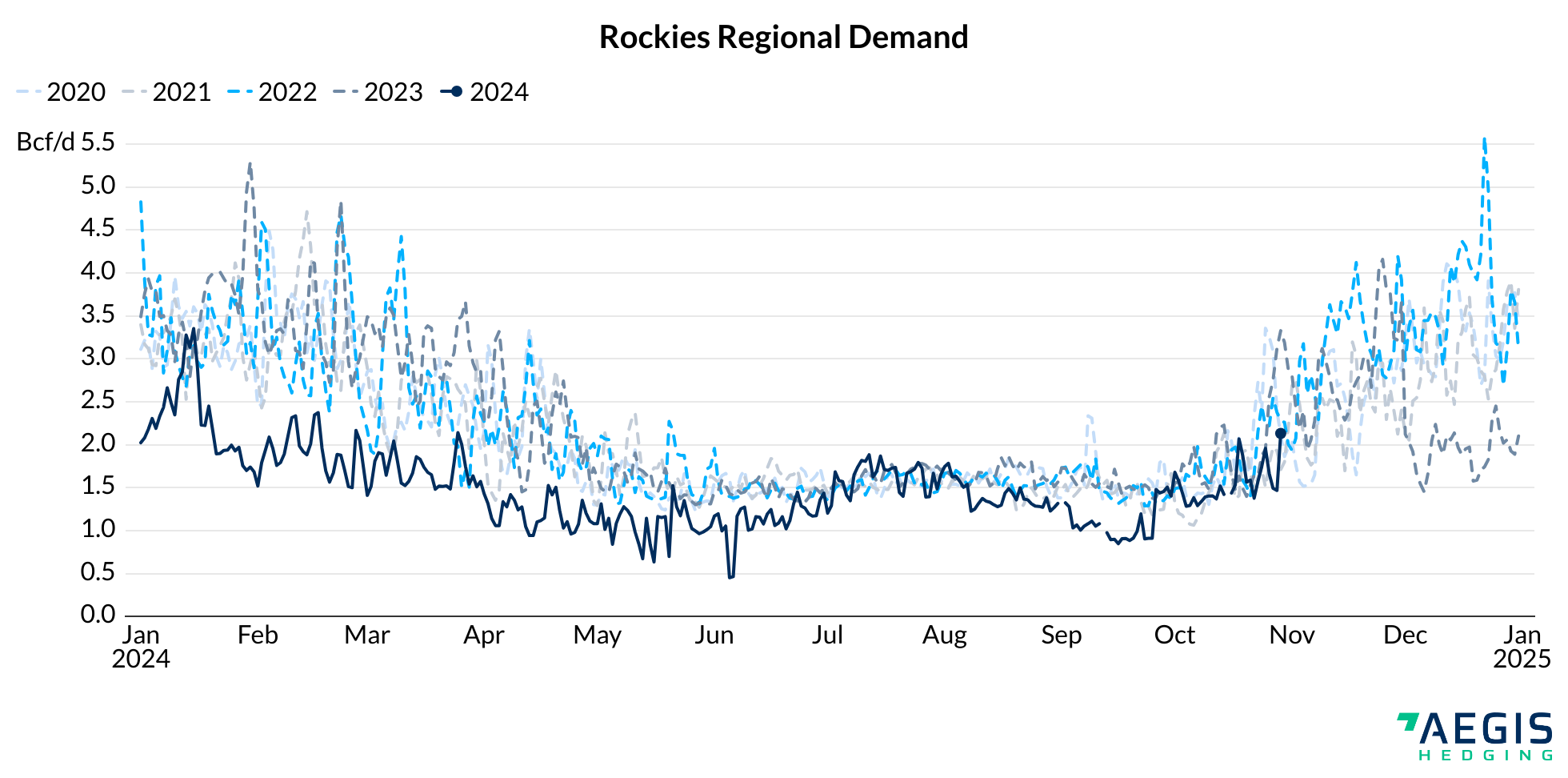

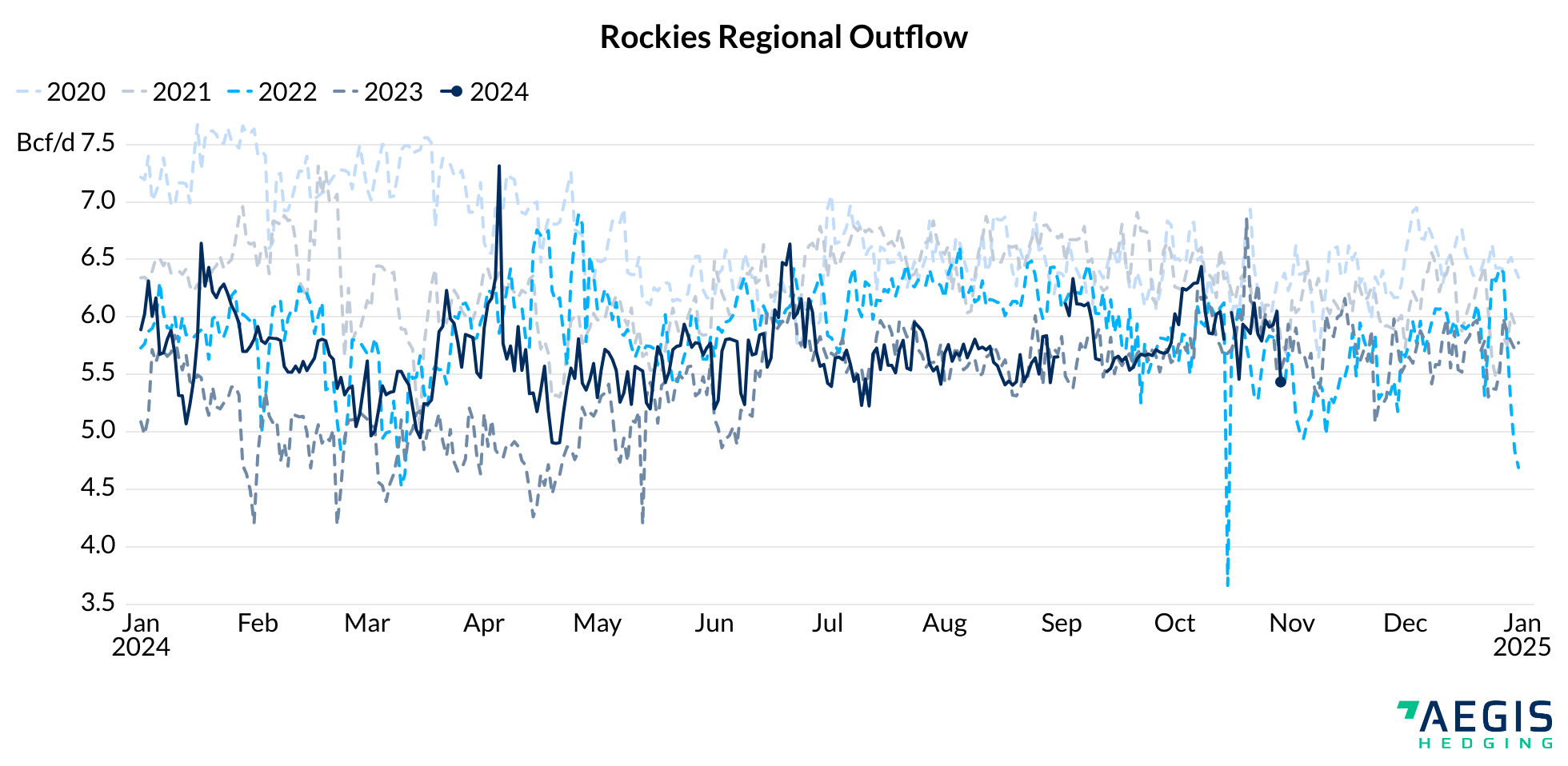

Gas Demand: Demand has started to increase as is the seasonal norm. Regional consumption for the month of October averaged 1.5 Bcf/d and just eclipsed the 2.0 Bcf/d mark October 25. Regional outflows continue around 5.8 Bcf/d on a daily basis. Overall, total demand of 8.0 Bcf/d remains low compared to the past couple of years but is increasing.

|

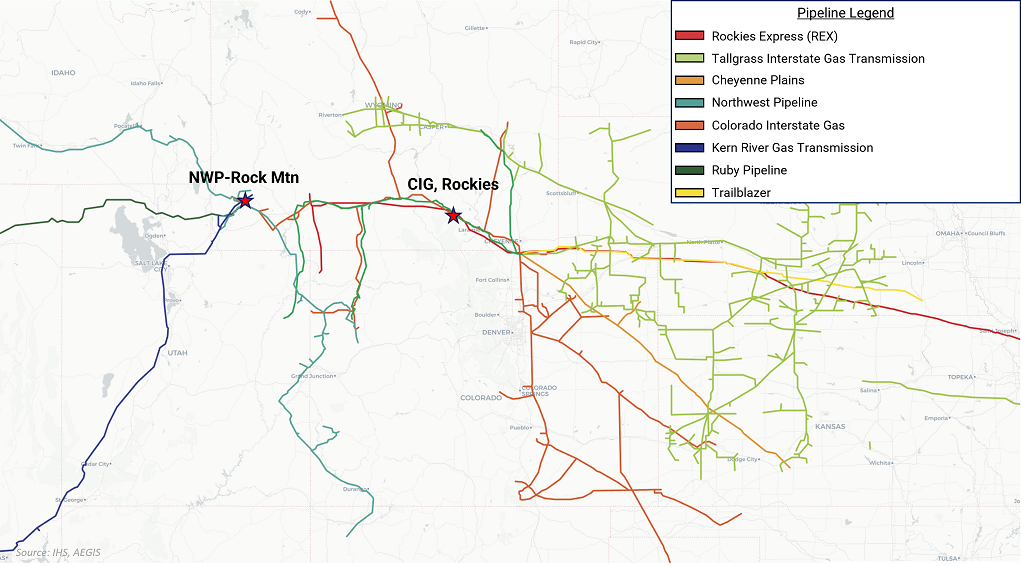

| Major Pipelines: |

|

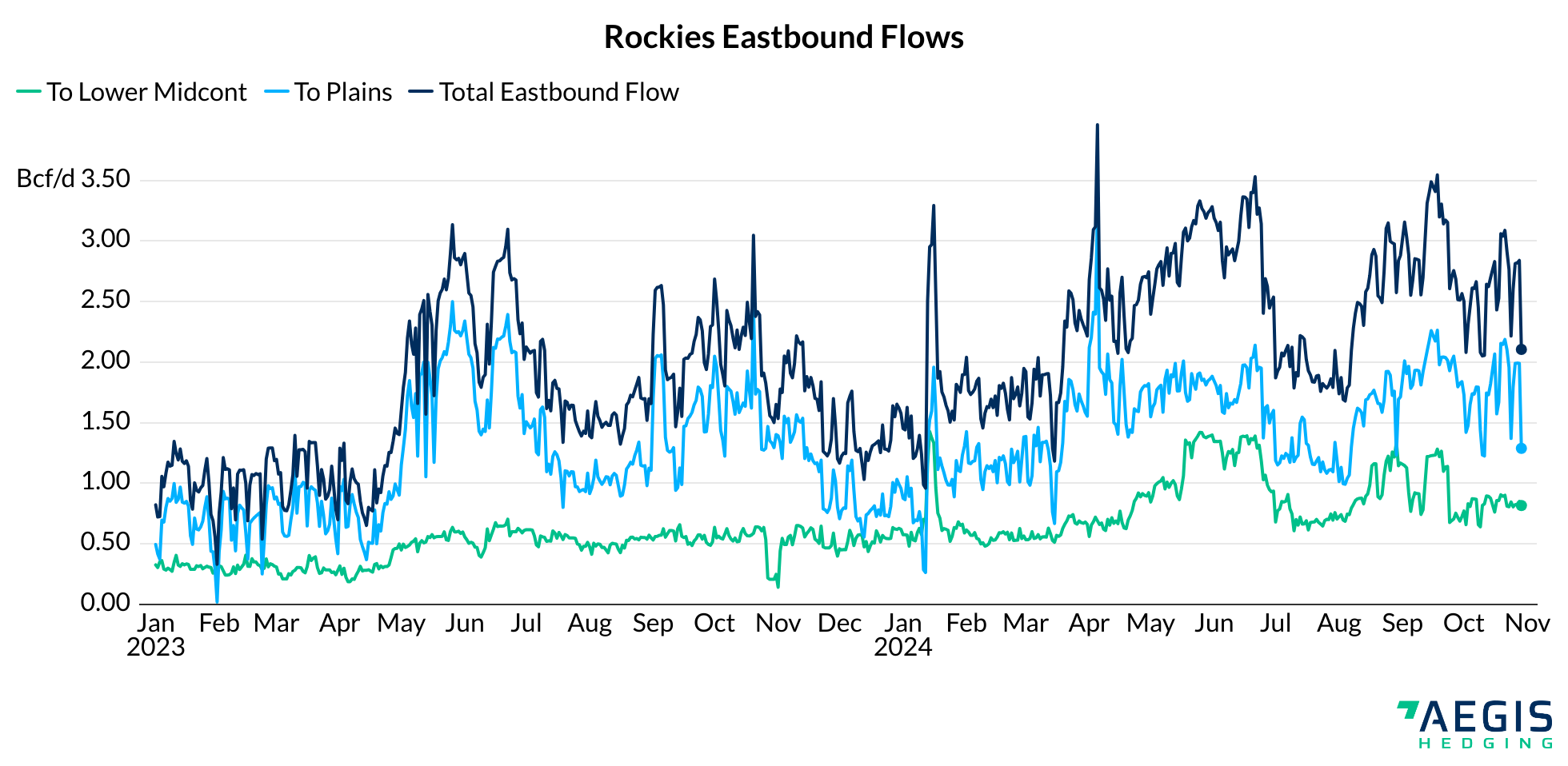

East - Eastbound capacity headed out of the Rockies is about 4.5 Bcf/d among CIG, REX, Southern Star, Trailblazer, Cheyenne Plains, and Tallgrass Interstate Pipelines. These pipelines typically serve Midwest demand via other Mid-Continent interconnects. REX reaches the furthest east, able to deliver gas as far as eastern Ohio. Gas flows on this eastern corridor are very seasonal. For example, eastbound flows on REX, measured by rates from Colorado to Nebraska, can vary between 1.75 Bcf/d in the spring or early summer but close to zero in the winter as gas stays home in the Rockies for local demand or reaches a more premium Opal and West market.

Colorado Interstate Gas (CIG) - Kinder Morgan's 4,350-mile pipeline system transports gas from supply areas in the D-J, Powder River, and other parts of the Rockies to customers in the Rockies, the Midwest, the Southwest, the Pacific Northwest, and California. Rockies Express (REX) is a 1,679-mile natural gas pipeline system that runs from southwest Wyoming and northwestern Colorado to eastern Ohio. Originally, REX was built to transport up to 1.8 Bcf/d from the Rockies to demand centers in the Midwest and Northeast. After the rise of Appalachian production, REX owner Tallgrass Energy decided to make the eastern part of REX bi-directional to allow westbound (Appalachian) flows into Illinois. REX is segmented into three rate zones.

Trailblazer Pipeline - A Tallgrass pipeline that runs from Cheyenne, Wyoming, to southeastern Nebraska. The pipeline travels 436 miles and provides an outlet for Rockies gas, seeking Midwest and East Coast markets via other pipeline interconnects. Cheyenne Plains Gas Pipeline - A pipeline that transports gas from the Rocky Mountains to the Midwest. The system consists of a 36-inch diameter pipe spanning 410 miles. The Tallgrass Interstate Gas Transmission system - A spiderweb of pipelines that consists of about 4,650 miles of natural gas transport. Most of the system resides in Kansas and Nebraska, with some in central and southeastern Wyoming and northeastern Colorado. Wyoming Interstate Co. - Another Kinder Morgan-owned pipeline that encompasses an 850-mile gas system whose mainline runs from western Wyoming to the REX Cheyenne Hub in northeastern Colorado.

South - Gas headed south competes with growing "associated" gas (produced by oil wells) from in the Permian. A bottleneck exists when looking at the south/southwest corridor, where the Kern River pipeline usually runs near or at capacity. Both El Paso and Transwestern take gas to the Arizona and California markets, but these two are often constrained, full of competing Permian supply. West - The Ruby and Northwest pipeline transport gas from the Opal hub to the Pacific Northwest (PacNW). Demand in the PacNW, including California, has been shrinking and has little prospects for demand growth. Further, the region receives Canadian gas that competes with the Rockies supply. Kern River is typically lumped in with the West market, but it delivers gas into southern California near the terminus of El Paso and Transwestern. However, the Kern pipeline sources gas from Opal at the same hub Northwest pipeline, so it is probably better classified as "westbound."

|

|

Hedging considerations CIG or NWRox basis can be hedged with swaps. Both are usually hedged as part of a complete natural gas hedge. The general recommendation is to hedge NYMEX Henry Hub natural gas and basis in two steps but simultaneously. Contact us at info@aegis-hedging.com if you need to work through the details. |