|

**AEGIS is attending the SMU Steel Summit Conference 2022 at the Georgia International Conference Center in College Park on August 22 – 24. If you would like to schedule a meeting during the summit, please contact Patrick McCrann at pmccrann@aegis-hedging.com or (713) 936-2806. **

|

Steel

Compared to 2021, finished steel exports from China are expected to dip by 0.7% this year to 66.19 million mt, according to Platts Analytics. The slight drop in exports is largely due to weaker global demand, as well as a decrease in domestic production because of COVID lockdowns. Production issues in Russia and Ukraine as a result of the ongoing war led to a surge in Chinese exports. Exports jumped in May and June; however, volumes have dropped since then.

Aluminum

On Wednesday, Norsk Hydro announced it will shutter its Slovakia-based aluminum smelter, Slovalco, at the end of September due to high electricity prices. The 175,000 mt/year capacity smelter is currently operating at 60% capacity; however, the company estimates it would experience significant losses if operations continued in 2023. This was Norsk’s second production cut announcement this week, as the company stated that 20% of production at the Norway-based Sunndal plant will be taken offline due to an upcoming worker strike. Both of these shutdowns add to a growing list of European smelter curtailments, as nearly 50% of the region’s smelter capacity has been lost, according to Bloomberg estimates.

Regarding raw materials, China’s alumina exports could stay above 100,000 mt/month in 2H 2022, according to Bloomberg estimates. This is an increase from the record 570,000 mt the country exported in 1H. Exports have increased in recent months due to ample domestic supplies and increasing international prices. Rusal, which is Russia’s largest aluminum producer, is grappling with sanctions and logistical issues and has received most of China’s recent alumina shipments. According to Bloomberg, Chinese annual production could increase by 8% to 78 million mt this year, and another 5% to 82 million mt next year, as new capacity is brought online.

Zinc

Zinc’s supply issues continue. Zinc prices surged over 6% Tuesday morning after Trafigura announced it will be shutting down one of Europe’s largest smelters beginning next month due to high electricity prices. Even prior to this announcement, analysts were increasing their zinc price forecasts. Earlier this week, Citigroup predicted that despite falling demand, further smelter curtailments in Europe due to an ongoing power crunch could lead to a rebound in zinc prices over the next 12 months. The bank has thus raised its three-month price target to $3,200/mt, and its six-to-twelve-month target to $3,400/mt. Both targets are up $400/mt from their prior forecast. However, the bank remains “marginally bearish,” as the power crisis in Europe could also suppress demand.

Cobalt

Finally, regarding cobalt, prices at the CME are nearing 11-month lows due to weak demand from a variety of sectors, according to S&P Global. However, several anonymous sources interviewed by S&P Global late last week suggest that China could begin stockpiling 2,300 mt of cobalt for its strategic metals reserve. Prices for metals normally rally as China starts its stockpiling efforts. However, others feel that battery demand needs to recover to see a sustained rally. Likewise, COVID lockdowns, which shut down manufacturing activity, could hinder any price gains. China has made similar purchases in the past, purchasing approximately 2,000 mt in 4Q 2020, and a rumored 3,000 mt in early 2021. Global cobalt mine production was 170,000 mt in 2021, according to the USGS.

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

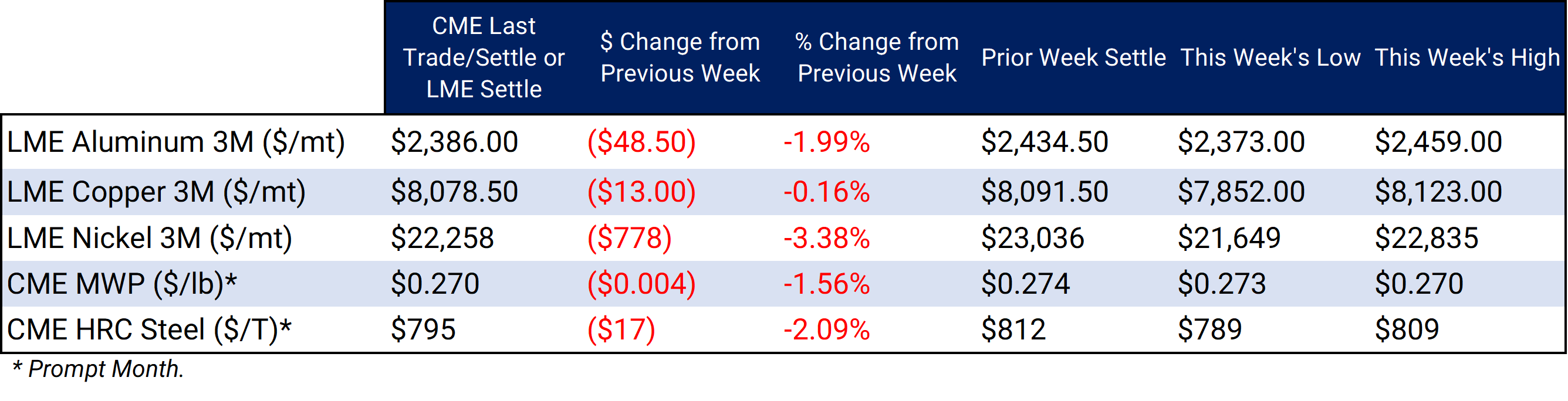

LME Aluminum 3M settled at $2,386.00/mt, down $48.50/mt on the week. Aluminum prices were down this week, so the forward curve has shifted lower by approximately $50/mt, but its shape continues to look the same. It remains in contango, meaning that spot prices are lower than futures prices. Aluminum consumers that are concerned about increasing prices might consider hedging future needs by buying swaps or call options. If you are an end-user, you might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 27.0¢/lb this week. The CME Midwest Premium contract was steady this week and remains in backwardation. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,078.50/mt, down $13/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted slightly lower. It remains backwardated, meaning that spot prices are higher than futures prices. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $22,258/mt, down $778/mt on the week. Nickel’s forward curve shifted significantly lower this week, by about $800/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded at $795/T, down $17/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with strategically placed limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

8/17/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 8/16/2022: Zinc Prices Are On The Rebound Due To Supply Issues 8/9/2022: Aluminum prices are finding support: Consumers can lock in lower costs in 2023 and beyond 8/2/2022: Russia Finds New Alumina Supply |

|||||

Notable News |

|||||

|

8/19/2022: China demand doubts darken mood as miners baulk at energy costs 8/18/2022: China's power shortages disrupt nonferrous operations 8/17/2022: US steel mill outages unlikely to shift market 8/17/2022: Slovalco will stop primary aluminium production 8/16/2022: Nyrstar to put Budel zinc operations on care and maintenance on Sept 1 8/16/2022: China's Tsingshan considers selling Indonesian assets to Baowu 8/15/2022: Green steel still decades away: BlueScope 8/15/2022: Commodity Tracker: 4 charts to watch this week 8/12/2022: Sky-high energy costs to fan fire under aluminium and zinc prices |

|||||