|

Aluminum Last week, the US Commerce Department issued preliminary tariffs on aluminum extrusion imports from Mexico, China, Turkey, and Indonesia. The MWP market reacted little because the final tariff rates won’t be known until late July 2024 due to the US Commerce Department’s ongoing investigation. Also, it is currently unclear when these tariffs will go into effect. (Sources: Mining.com, Wiley Law) |

|

|

Century Aluminum and MX Holdings will soon build a plant for low-carbon secondary billet production, according to a press release from Wednesday. The companies expect production to begin in 2026 and will ultimately have an output of 250 million lbs/year. They are currently reviewing several locations in the Ohio Valley for the facility. (Source: Century Aluminum, MX Holdings) Chinese primary aluminum production surged in February and will jump again in March, according to estimates by Shanghai Metal Market. Last month, the country’s primary aluminum smelters produced 3.333 million mt, up 7.8% compared to February 2023. For March, SMM predicts that production will jump to 3.55 million mt, up 4.0% compared to last March. This increasing output is mainly due to a smelter in Mongolia ramping up production. Seasonally, demand increases after the Lunar New Year holiday, justifying this uptick in production. (Source: Shanghai Metal Market) At a recent industry conference, the China Nonferrous Metals Industry Association requested its members step up aluminum exports to relieve a supply glut amid subpar demand. Last year, unwrought aluminum exports fell by 14% compared to a year prior. In 2022, the country exported a record 6.6 million mt. Rising exports from China, the world’s largest producer, could be a burden on global prices. (Source: Bloomberg, China Customs) Finally, Alcoa has agreed to buy Alumina Ltd for $2.2 billion, the companies announced earlier this week. Alumina Ltd is the Australian joint-venture arm of Alcoa. When Alcoa made its initial bid in late February, it stated that this move would help consolidate and streamline Alcoa’s Australian operations and “enhance Alcoa’s position as of one of the world’s largest bauxite and alumina producers,” according to Alcoa’s earlier press release. The deal is expected to close by 3Q2024. (Sources: Bloomberg, Alcoa) |

|

Copper Copper prices rallied this week on Chinese production issues. According to anonymous sources, 19 Chinese copper smelters met on Wednesday and agreed to production cuts due to low profitability amid a collapse in treatment charges. These treatment charges are the fees that miners pay to have their raw copper concentrate processed into refined metal. The companies also reportedly discussed switching to more copper scrap, delaying projects, and rearranging maintenance schedules. (Source: Bloomberg) Hopes that Chinese demand will recover have also fueled the recent bullishness. In an annual government meeting last week, Chinese authorities provided little detail on how they plan to grow industries that are large metals consumers, but some analysts believe that demand will recover in the coming months. In a note late last week, Citigroup stated that Chinese demand “could be quickly revitalized by strong credit prints for February and March and/or meaningful detail of support for metals-intensive sectors like property and infrastructure.” Some supply issues have sprung up recently, further fueling the bullishness. (Source: Bloomberg) Several market analysts are becoming conservatively bullish on copper, mainly due to Chinese production issues and an expected increase in demand. In a note earlier this week, Jefferies stated, “The timing of the next bull market in copper has been pulled forward due to a better demand outlook than we had previously envisioned. Obviously there are still risks, and we are not raising our near-term copper price forecasts yet, but our current deck is increasingly conservative.” Others remain more skeptical, however, while red-hot inflation in the US could keep interest rates elevated. (Sources: Bloomberg) One of Codelco’s most important copper mines remains closed after a fatal accident. Last Friday, a trucking accident at the Radomiro Tomic mine caused one fatality, and the mine has been closed since. This latest issue adds to the myriad of problems that Codelco has had in recent years. Last year, the company’s production hit a 25-year low due to political strife and weather-related issues. Codelco is Chile’s state-owned copper miner and the world’s largest producer. |

|

Steel Nippon Steel’s potential buyout of US Steel will likely be a hot topic when President Joe Biden meets with Japanese Prime Minister Fumio Kishida next month. In a statement on Thursday, Biden proclaimed, “US Steel has been an iconic American steel company for more than a century, and it is vital for it to remain an American steel company that is domestically owned and operated. It is important that we maintain strong American steel companies powered by American steel workers. I told our steel workers I have their backs, and I meant it.” Lawmakers could reject the deal due to national security concerns and other issues. (Sources: Bloomberg, Reuters) Nippon Steel’s meeting with the United Steelworkers (USW) union last week Thursday lasted less than an hour. This signals the union does not support Nippon’s potential buyout of US Steel. In a letter released shortly after the meeting, the USW said as much, stating, “Nippon has still not earned the trust of the USW, and we remain convinced that the company does not fully understand its obligations to [the union]. We also continue to be concerned about issues involving national defense, critical infrastructure, and supply chains.” The union cannot block the transaction, but it does hold significant sway over lawmakers that could block the merger due to national security concerns. (Source: Bloomberg) Late last week, Cleveland Cliffs, one of America’s largest steel producers, set its minimum HRC price at $840/st. Although Cleveland’s press release stated this was a price increase, a quick survey of the company’s recent press releases suggests this was a substantial decrease. In January, Cleveland set its minimum HRC price at $1,150/st. Even though spot prices have fallen in recent months, American steelmakers are still highly profitable at these levels. (Source: Cleveland Cliffs) Outokumpu, Europe’s largest stainless steel producer, believes its stainless steel deliveries will be lower this quarter due to a port strike in Finland. They believe deliveries will be similar to last quarter. The port strike, which is expected to last two weeks through March 25, stems from political issues that are not directly related to Outokumpu. (Source: Bloomberg) Raw materials, prices for zinc, a key raw material for hot-dipped galvanized steel production, have jumped in recent weeks while investment funds cover their short position. At the end of February, investment funds, generally speculators in metals markets, had a net short position of approximately 19,000 contracts. As of last Friday, however, these funds had a net short position of only 6,900 contracts. Given that investment funds can have an oversized impact on metals markets, this is likely why LME zinc prices have rallied nearly 6% this month. (Source: LME) |

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

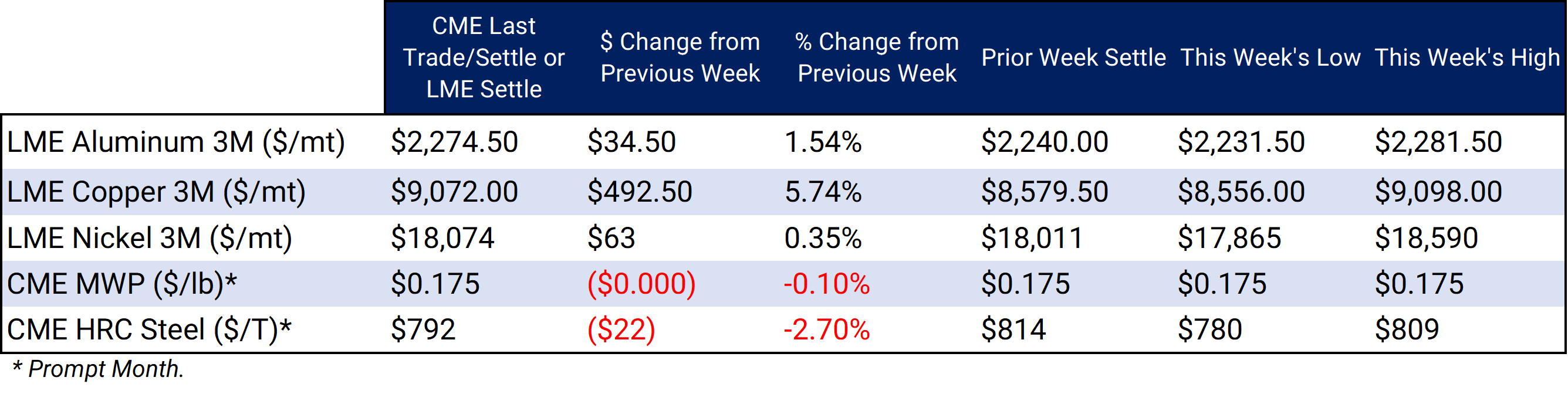

LME Aluminum 3M settled at $2,274.5/mt, up $34.5/mt on the week. Aluminum prices were up this week. Compared to last week, the futures forward curve has shifted vertically higher by approximately $35/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 17.5¢/lb this week. The CME Midwest Premium market is now in a contango from the March ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $9,072/mt, up $492.5/mt on the week. Compared to last Friday, LME Copper's forward curve has risen vertically by approximately $500/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $18,074/mt, up $63/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $60/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $792/T, down $22/T on the week. Steel mill profit margins improved dramatically throughout 3Q and 4Q2023 and are also starting 2024 on a good note. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $405/st, up from about $320/st on September 1. This is mainly due to decreasing scrap prices. Thus, steel mills should consider hedging production and raw material usage for 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

3/14/2024: Important US Economic Data (AEGIS Reference) 3/13/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 2/27/2024: Aluminum Consumers Should Still Implement Hedges, Even Though Russia Sanctions Mean Little 2/2/2024: China's Real Estate Woes Provide Opportunity for Copper Consumers 1/25/2024: Aluminum Starts 2024 On a Down Note, But Potential Supply Shocks Give Consumers a Reason to Hedge |

|||||

Notable News |

|||||

|

3/14/2024: Nippon Steel says no layoffs, no plant closures at US Steel till 2026 3/14/2024: Raw materials squeeze jolts copper out of its torpor 3/14/2024: Nippon Steel's $14.9 bln takeover deal for U.S. Steel under scrutiny 3/13/2024: Biden to express concern over Nippon Steel's deal for U.S. Steel, source says 3/13/2024: China's top copper smelters agree on rare joint production cuts, sources say 3/13/2024: Toyota agrees to biggest wage hike in 25 years, paves way for BOJ shift 3/13/2024: China coal group says US curbs on Russia to keep prices high, hurt exports 3/13/2024: Australia's Wyloo says industry will turn from LME without green nickel 3/12/2024: Tin supply trapped in resource nationalism squeeze |

|||||