|

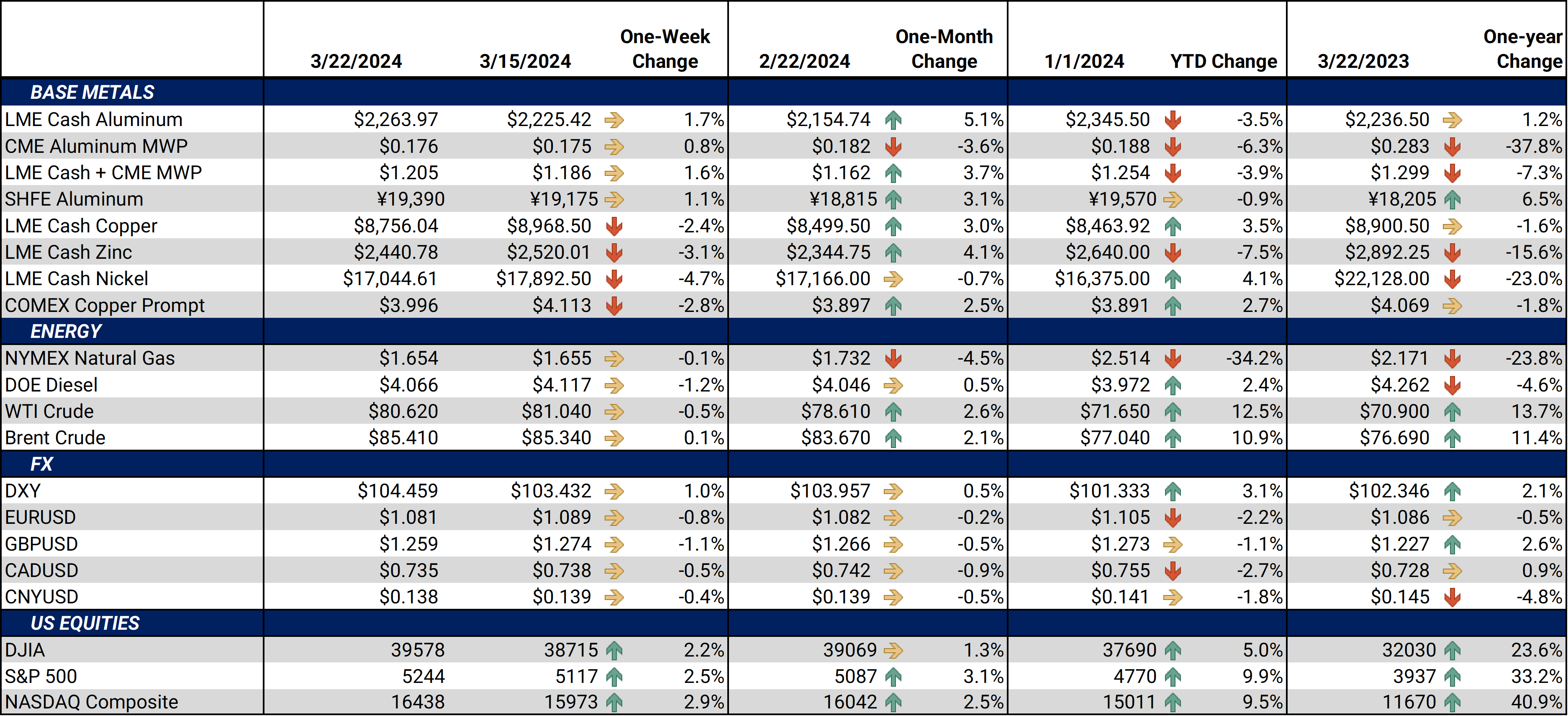

Aluminum Speculators are essentially flat LME aluminum, according to the LME’s most recent COT report, out Tuesday. As of last Friday’s close, investment funds, generally speculators in metals markets, are net short only about 1,680 contracts, down from being short over 22,000 contracts on March 1. The prior position was these funds' largest short position since late last year. This short covering likely stems from an anticipated increase in Chinese aluminum demand and stabilizing demand in the US. (Source: LME) |

|

|

China’s top aluminum production region, Yunnan province, could have lower output this year due to continued hydropower issues, according to a report from China’s state-owned Kunming Power Exchange Center. Yunnan province has experienced a severe drought that has hampered hydroelectricity production in recent years, and those issues could persist into 2024, according to the report. It is unclear how much production could be curtailed, but according to industry sources, the most recent mandatory curtailment in November 2023 was for 1.1 million mt/year. Yunnan province has approximately 5.7 million mt per year of primary aluminum production capacity. (Source: S&P Global) China could soon require the country’s primary aluminum smelters to participate in a carbon trading program to reduce the industry’s emissions. Market sources told S&P Global that such a program could raise costs for smelters that rely on fossil fuels and push the industry to greener technologies. About 60% of Chinese primary aluminum producers use fossil fuels such as coal for electricity generation, while the remainder use renewable sources such as hydropower. These sources also stated that such a program would benefit secondary aluminum producers who use scrap as a raw material and, therefore, are less energy intensive. The consultation period in which the country’s aluminum smelters can opine on the potential carbon trading programs ends on March 31. Given that this is still in the debate stage, it is unclear how much of an impact this could have on Chinese primary aluminum production. (Source: S&P Global) Last year, 23% of Rusal’s primary aluminum sales went to China, up from 8% in 2022. This surge in exports to China is mainly due to stellar demand and Rusal’s implementation of steep discounts relative to global prices. China is now the top buyer of Russian aluminum, and similarly, nearly all of China’s primary aluminum imports come from Russia. Rusal’s European sales fell from 36% to 28%, and America only represented 1%. Russian aluminum has become a taboo subject since the start of the Russia-Ukraine conflict nearly two years ago, with most Western buyers trying to shun Russian metal. In February 2023, the Biden administration initiated a 200% tariff on Russian aluminum, effectively shutting Russia out of the US market. These sales figures were taken from Rusal’s 2023 earnings report, out Friday (March 15). (Source: Bloomberg) |

|

Copper Like aluminum, investment funds have been significant buyers of LME copper in recent weeks. As of last Friday’s close, investment funds are net long 37,860 contracts, their largest long position in over two years. This action has helped rally prices nearly 10% off the lows of early February and could stem from production issues in China. (Source: LME) According to recent statements from copper producer Freeport McMoran, the US needs to overhaul its mine permitting process to meet its ambitious energy transition goals. "The U.S. government needs to stop giving lip service to permitting. The question is, given our political system that we have today and the dysfunctionality of it, how do you go from getting a project verbally accepted to getting actions done?”, Freeport McMoran CEO Richard Adkerson stated at the CERAWeek energy conference earlier this week. (Source: Reuters) Chinese economic data continues to be mixed. On Monday, government data showed that industrial output for January and February combined jumped by 7% compared to a year ago. Meanwhile, property development investment fell by 9% compared to last year. Despite the production issues that have rallied global copper prices, China’s lackluster property sector could remain a burden. (Source: Bloomberg) The production and profitability issues that Chinese copper smelters have faced recently have been a boon for the country’s copper miners. According to an analysis by Citigroup, if copper prices rise by 5% in 2024, the net profit for Zijin/CMOC/Jiangxi Copper should increase by 6%/10%/11%, respectively. Treatment charges, which are the fees that smelters charge for processing raw copper into refined metal, have collapsed in recent months due to low available feedstock, thereby pressuring profitability. (Source: Bloomberg) |

|

Steel Late last Thursday, Nippon Steel proclaimed that should its buyout of US Steel be approved, Nippon would not close any plants or perform layoffs until September 2026. Nippon also stated that the potential acquisition is going through the regulatory review process, and they are determined to see it through. This potential deal has become a hot-button issue in recent weeks, with some lawmakers and President Biden balking at the transition due to political and national security concerns. (Source: Reuters) Late last week, Cleveland Cliffs proclaimed it would make another offer for US Steel if Nippon Steel’s potential buyout falls through. Cleveland Cliffs’ offer would be only $30/share, far lower than Nippon’s $55/share offer. It’s unclear if this tactic would work, but it would alleviate one concern many US lawmakers and President Biden have raised. Recently, President Biden stated that US Steel should remain a US-owned and operated company, and several other government officials have echoed similar comments. (Source: Reuters) After a nearly 40% drop so far this year, iron ore prices could be on the mend, according to industry sources. As Shanghai-based Chaos Ternary Research Institute stated earlier this week, “Chinese mills are conducting more unscheduled maintenance in March due to widening losses and rising steel-product inventories. While that’s reduced the need to replenish ore inventories, purchases may pick up after the recent slide in prices.” (Source: Bloomberg) Australian iron ore producers could be forced to seek out new buyers while top importer China aims to decarbonize its high-polluting steel industry, according to Reuters. Historically, Australia has been the world’s largest iron exporter, with 80% going to China. Most of China’s steel production uses iron ore as a raw material, but annual steel production has hovered near 1 billion mt for the past five years, suggesting that steel and iron ore demand has flatlined. As Reuters recently suggested, Australian iron ore miners could switch to other Southeast Asian buyers, but their demand will likely pale in comparison to that of China. Reuters also indicated that Australia could ramp up its own steel production, but this would take significant investment. (Source: Reuters) |

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

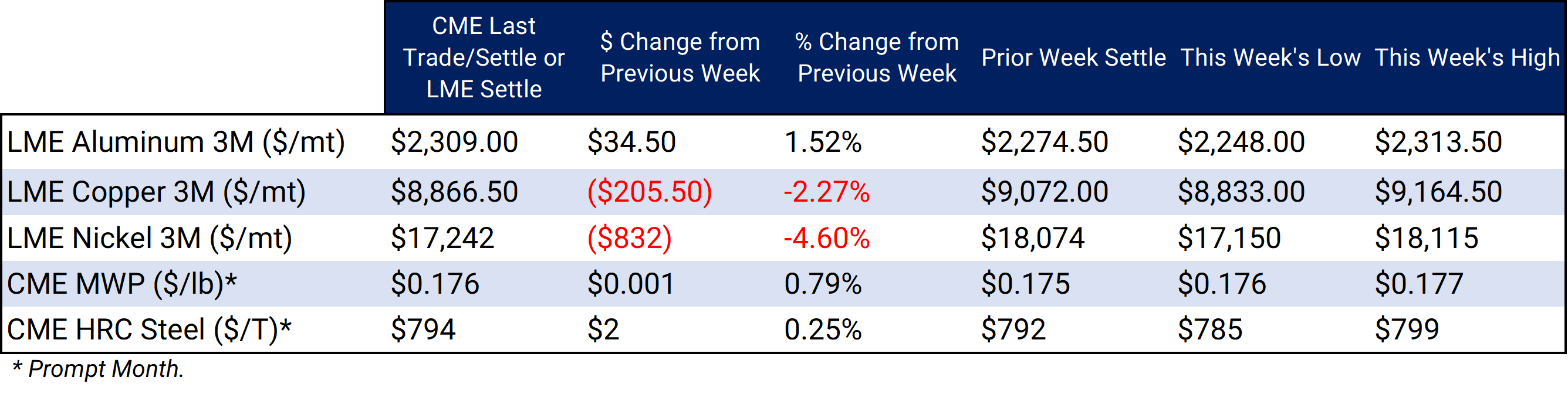

LME Aluminum 3M settled at $2,309/mt, up $34.5/mt on the week. Aluminum prices were up this week. Compared to last week, the futures forward curve has shifted vertically higher by approximately $35/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 17.6¢/lb this week. The CME Midwest Premium market is now in a contango from the March ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,866/mt, down $205.5/mt on the week. Compared to last Friday, LME Copper's forward curve has fallen vertically by approximately $200/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $17,242/mt, down $832/mt on the week. As prices were down this week, nickel’s forward curve has also shifted vertically lower by about $830/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $794/T, up $2/T on the week. Steel mill profit margins improved dramatically throughout 3Q and 4Q2023 and are also starting 2024 on a good note. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $410/st, up from about $320/st on September 1. This is mainly due to decreasing scrap prices. Thus, steel mills should consider hedging production and raw material usage for 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

3/20/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 3/14/2024: Important US Economic Data (AEGIS Reference) 2/27/2024: Aluminum Consumers Should Still Implement Hedges, Even Though Russia Sanctions Mean Little 2/2/2024: China's Real Estate Woes Provide Opportunity for Copper Consumers 1/25/2024: Aluminum Starts 2024 On a Down Note, But Potential Supply Shocks Give Consumers a Reason to Hedge |

|||||

Notable News |

|||||

|

3/21/2024: France sets end March deadline for New Caledonia nickel deal 3/20/2024: Barrick looks to explore new gold, copper deposits in DR Congo 3/20/2024: US eases tailpipe rules, slows EV transition through 2030 3/20/2024: China, decarbonisation present Australia's iron ore miners with costly choices 3/19/2024: Vista Metals to invest $60 Million in Aluminum Casting Facility in Bowling Green 3/19/2024: BYD sees NEV share reaching 50% in the next 3 months in China as EV price war heats up 3/19/2024: China's Yunnan struggles with power supply, stokes fear among aluminum sector 3/18/2024: China starts consultation for enrolling aluminum smelters into compliance carbon market 3/18/2024: Indonesia says nickel miner Vale to build another $2 bln HPAL plant 3/17/2024: Tesla Vs. BYD: Tesla Plunges As Analysts Slash Estimates; BYD Rebounds In EV Price War 3/15/2024: Cleveland-Cliffs CEO mulls much lower bid for US Steel if Nippon deal falls apart |

|||||