|

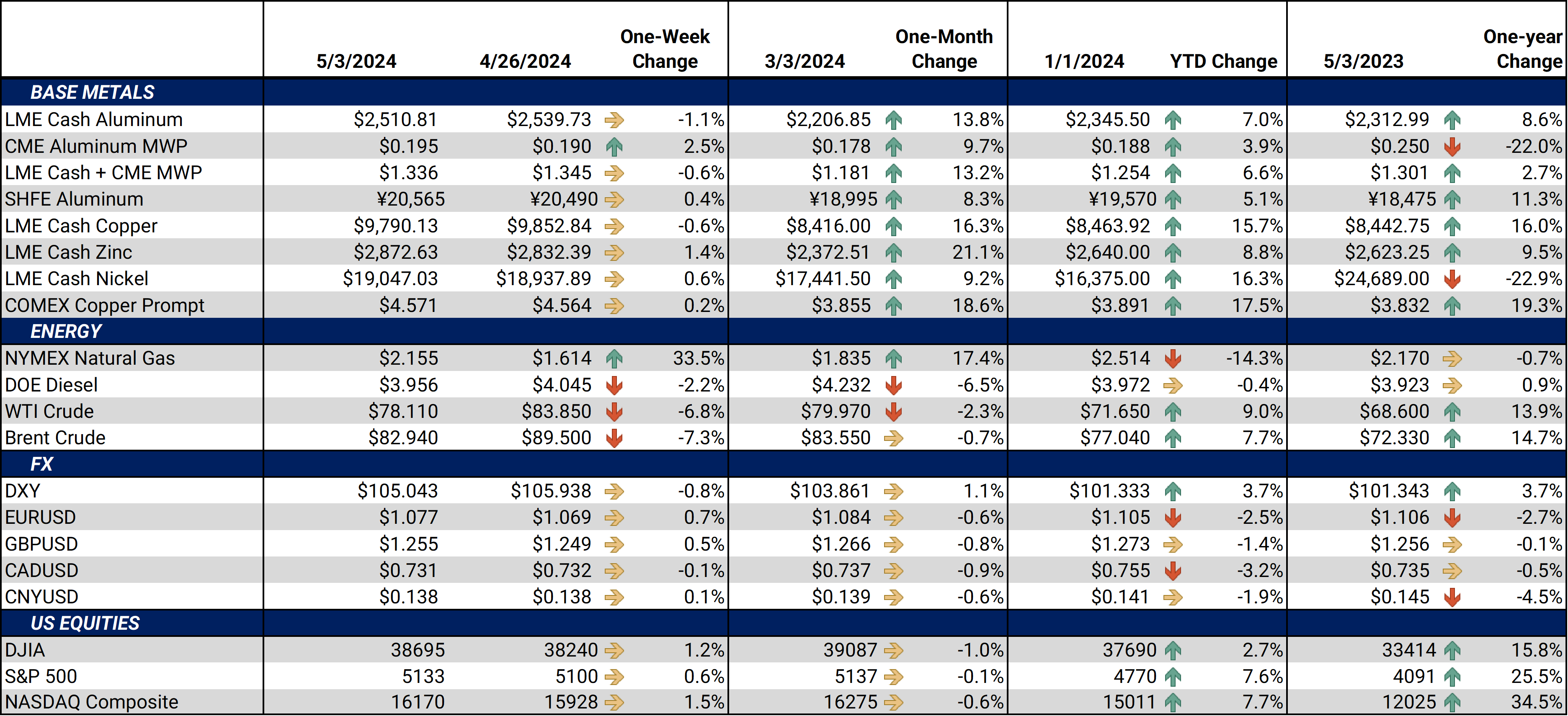

Aluminum Contrary to normal trading and price reaction, LME aluminum prices fell while spec traders increased their long position last week. As of last Friday, investment funds, generally speculators in metals markets, bought a net 9,200 contracts, bringing their total net long position to approximately 103,460 contracts. However, prices fell about 4% last week while funds were increasing their net long position. This is highly unusual, as investment fund positioning is usually positively correlated with price action. With prices falling this week, next Tuesday’s report will show if funds used this as another buying opportunity or if they liquidated positions. (Source: LME) |

|

|

Due to higher aluminum prices elsewhere, Rusal could seek out new Asian buyers outside China, according to Shanghai Metal Market (SMM). Even though this is possible, SMM still believes that China’s domestic aluminum prices will remain supported due to stimulus measures and improving demand. China is the top buyer of Russian aluminum, and similarly, nearly all of China’s primary aluminum imports come from Russia, according to Rusal and Chinese government data. (Source: Bloomberg, China Customs, Rusal) Continuing on Chinese demand, last quarter, the Aluminum Corporation of China (Chalco), the world's largest aluminum producer, reported a 39.6% increase in profits compared to a year ago, even though revenue dropped by 26%. Aluminum production jumped by 16% to 1.78 million mt, while operating costs fell by 31%. They also stated that operating costs should continue to fall while Chalco continues to build self-sufficiency in bauxite supplies. (Source: Bloomberg) Indonesia’s Shandong Nanshan Aluminum Company plans to more than double its alumina production capacity to 4.5 million mt/year, up from 2 million mt/year. The company cites rising demand and ample local bauxite supplies for the expansion. They are building a 250,000 mt/year capacity aluminum smelter. The alumina plant is expected to cost $870 million and is pending approval from local authorities. (Source: Bloomberg) Finally, the LME is considering having its branded, deliverable aluminum producers submit carbon data to the exchange starting in early 2025. According to the LME, this would “align [the] aluminium market with the requirement of Europe's Carbon-Border Adjustment Mechanism (CBAM) which applies a carbon-related cost to certain imported products.” If the proposal is enacted, aluminum producers must report their emissions to the exchange data by March 15, 2025, and report updates annually. Any brand that fails to comply will be delisted. Since this is in the proposal and consultation stage, it is unclear how this would impact LME prices or warehousing. (Source: Reuters) |

|

Copper In the copper market, both prices and investment funds’ long position increased last week. Investment funds purchased about 4,950 net contracts, while prices rose by roughly 1%. This should be considered normal, positively-correlated action. Investment funds are now net long 55,660 contracts, reaching another new all-time high last week. Given that prices fell this week, it’s possible that investment funds have taken some money off the table. (Source: LME) Continuing on price action, Chinese copper demand is now back into focus as global prices hover near $10,000/mt. Factory activity in China expanded for a second straight month, beating analyst expectations. However, fabricators are still struggling to pass along higher costs to end-users, which is suppressing demand. This could potentially cap global prices. (Source: Bloomberg) Due to high global copper prices, China could export up to 100,000 mt in the coming weeks, according to anonymous sources interviewed by Reuters earlier this week. The sources also stated that this metal will likely be shipped to LME warehouses. Currently, only 1,150 mt, or about 1%, of LME On-Warrant copper inventories are from China. (Source: Reuters) Late last week, BHP made an offer to buy rival miner Anglo American for $38.9 billion. However, Anglo American rejected the offer, stating it undervalued the company. As Bloomberg suggested, this could potentially set off a bidding war for Anglo American. Anglo-American has been performing relatively poorly lately, so Anglo’s shareholders are incentivized to push for a deal. (Source: Bloomberg) Finally, India’s Vedanta Resources is seeking $1.4 billion to revive its Konkola Copper Mines (KCM) operation, according to reports from earlier this week. Vedanta has approached several trading houses, including Mercuria, for offtake agreements that would ensure sales and cash flow. The funding would be used to pay off creditors and expand operations. Vedanta recently resolved a dispute with the country and is also working to resolve ongoing debt issues with creditors. Resolving these issues would help bolster Zambia's position as an emerging copper mining country. Zambia is Africa's second-largest copper miner, behind the neighboring Democratic Republic of the Congo. (Sources: Bloomberg, USGS) |

|

Other Important LME and CME Metals & Markets

|

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

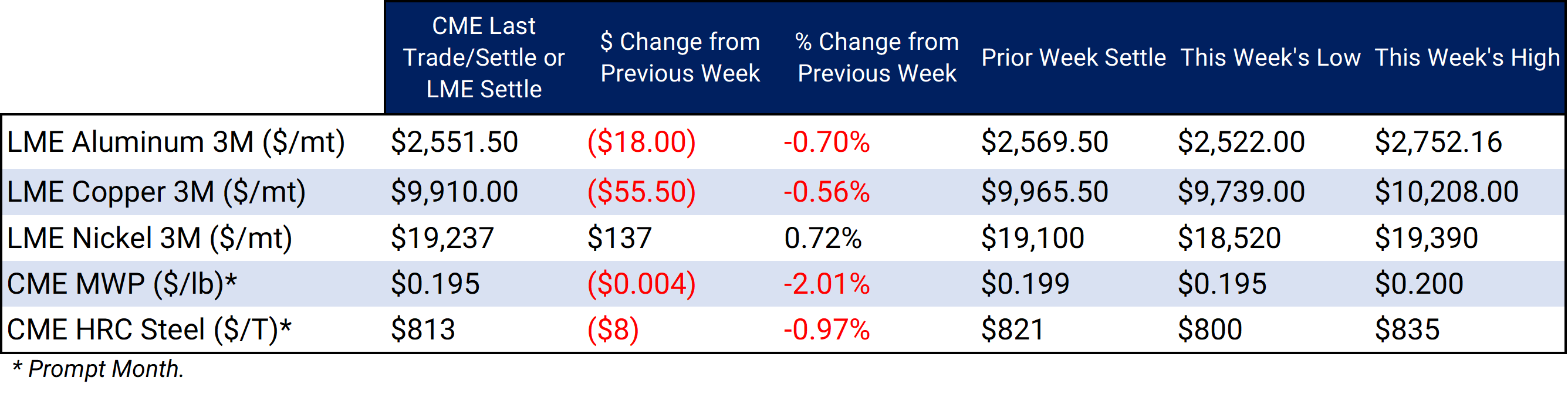

LME Aluminum 3M settled at $2,551.5/mt, down $18/mt on the week. Aluminum prices were down this week. Compared to last week, the futures forward curve has shifted vertically lower by approximately $20/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 19.5¢/lb this week. The CME Midwest Premium market is now in a contango from the May ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $9,910/mt, down $55.5/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted vertically lower by approximately $55/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $19,237/mt, up $137/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $140/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $813/T, down $8/T on the week. Steel mill profit margins improved dramatically throughout 3Q and 4Q2023 and are also starting 2024 on a good note. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $415/st, up from about $320/st on September 1. This is mainly due to decreasing scrap prices. Thus, steel mills should consider hedging production and raw material usage for 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

5/1/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 4/25/2024: Mexico's New Tariffs on Steel and Aluminum Imports Create Uncertainty in US Markets 4/3/2024: Important US Economic Data (AEGIS Reference) 2/27/2024: Aluminum Consumers Should Still Implement Hedges, Even Though Russia Sanctions Mean Little 2/2/2024: China's Real Estate Woes Provide Opportunity for Copper Consumers 1/25/2024: Aluminum Starts 2024 On a Down Note, But Potential Supply Shocks Give Consumers a Reason to Hedge |

|||||

Notable News |

|||||

|

5/1/2024: Exclusive: Near-record high LME prices a magnet for Chinese copper exports | Reuters 4/30/2024: Anglo to meet top shareholders on BHP bid as takeover rules restrain AGM 4/28/2024: Saudi Arabia set on securing lithium for EV ambitions 4/27/2024: BHP considering improved proposal for Anglo American after bid rejected, source says 4/26/2024: Beer can maker Ball Corp lags sales estimates on slowing demand | Reuters |

|||||