|

Aluminum The premium for 1Q 2023 aluminum deliveries into Japan will likely be approximately $95/mt, a 4% price drop from 4Q 2022 and the lowest since 2020, according to Bloomberg. This is the premium over the London Metal Exchange (LME) cash price that Japanese importers agree to pay for primary aluminum shipments. These premiums, which are set on a quarterly basis, are negotiated directly between Japanese end-users and global aluminum producers. At least one Japanese aluminum producer offered this $95/mt premium, thereby signaling what pricing other buyers are likely to pay. This premium has dropped in recent quarters as demand, specifically from the automotive sector, has softened, according to Bloomberg. Japan imported approximately 2.793 million mt of aluminum in 2021, or about 4% of global production, according to the Japan Ministry of Finance and USGS data. (Sources: Bloomberg, Japan Ministry of Finance, USGS) |

|

US aluminum consumers should watch closely what is happening in Japan because it could foretell changing trade flows and weakening prices. Already, Japan's premiums (over LME pricing) are shrinking, signaling that manufacturing is turning away the supply of metal. The displacement is likely to send the metal to other importing countries. As aluminum shipments are rerouted, the immediate result could be lower premiums in North America, represented most commonly by MWP. More broadly, AEGIS wonders if these shrinking premiums are a sign of emerging, persistent oversupply. |

|

|

The bearish aluminum news continues in China. Bloomberg reports that rising production in China will lead to a global aluminum market surplus of 156,000 mt, potentially weighing on prices into 2023. This “small” surplus compares to an expected deficit of 560,000 mt this year. Bloomberg expects aluminum prices to range between $2,200 to $2,500/mt in 2023, a similar range in 2H 2022. Production will grow in China, Canada, Indonesia, and India; however, currently curtailed production in Europe will remain offline through at least 2023. Beyond 2023, Bloomberg expects a surplus of 238,000/mt in 2024 and 156,000 mt in 2025. Aluminum demand will increase in 2023 through 2025; however, at a slower pace than the increasing production. The uptick in demand will mainly come from increasing electric vehicle production. (Source: Bloomberg)

Copper

For more info on copper, please check out our latest article, Does the Copper Rally Have Legs?

How bullish are the prospects for copper? Largely due to China easing its COVID restrictions, Goldman Sachs has lifted its 2023 average price forecast to $9,750/mt, from $8,325/mt. They also upped their 3/6/12 months price targets to $9,500/$10,000/$11,000/mt, compared to $6,700/$7,600/$9,000/mt previously. According to their note, “China’s stockpiles of the metal is almost entirely depleted” as we enter 2023, the bank anticipates improved buyer demand as stockpiles increase. (Source: Bloomberg)

The bullish views also go beyond 2023. Due to increasing demand from the energy transition, miner Glencore now predicts a cumulative copper shortfall of nearly 50 million mt by 2030. Despite the expected deficit, Glencore does not currently plan to increase production. Earlier this week, Glencore stated “we want to see that deficit,” later declaring that they will only increase production when buyers are “screaming” for copper. According to the company, current production hovers near 1 million mt but could be increased by 60% with the current assets. (Sources: Bloomberg, Glencore)

Steel

Due to a government stimulus-driven economic recovery, China's steel sector output will grow next year, according to BHP. Moreover, they feel that "all fundamentals are in place" for China’s economy to grow over the next 20 years. The company is also bullish on metals demand related to global decarbonization efforts, stating “the world is going to require roughly four times as much nickel over the next 30 years as it did in the past three years, two times as much copper and steel.” These comments were made by BHP CEO Mike Henry at the Reuters NEXT conference held last week. (Source: Reuters)

Import Tariffs

The EU and US are contemplating new, “first-of-its-kind” climate-based tariffs on Chinese aluminum and steel, according to Bloomberg. The proposed tariffs are an attempt to combat carbon emissions from China’s aluminum and steel industries. Both governments have also accused China of creating “overcapacity” that hampers the EU’s and US’s steel and aluminum industries, according to Reuters. However, the tariffs are currently just an “idea,” and not formally proposed by the EU or US. Moreover, an agreement with the EU isn't likely until late 2023 “at the earliest,” according to Reuters’ sources.

The US currently imports little steel and aluminum from China, so these tariffs, if implemented, would likely have little impact on US steel prices or aluminum import premiums. However, the tariffs could also target “large polluting nations,” according to Bloomberg. (Sources: Bloomberg, Reuters)

|

|

|||||

LME Aluminum |

|||||

|

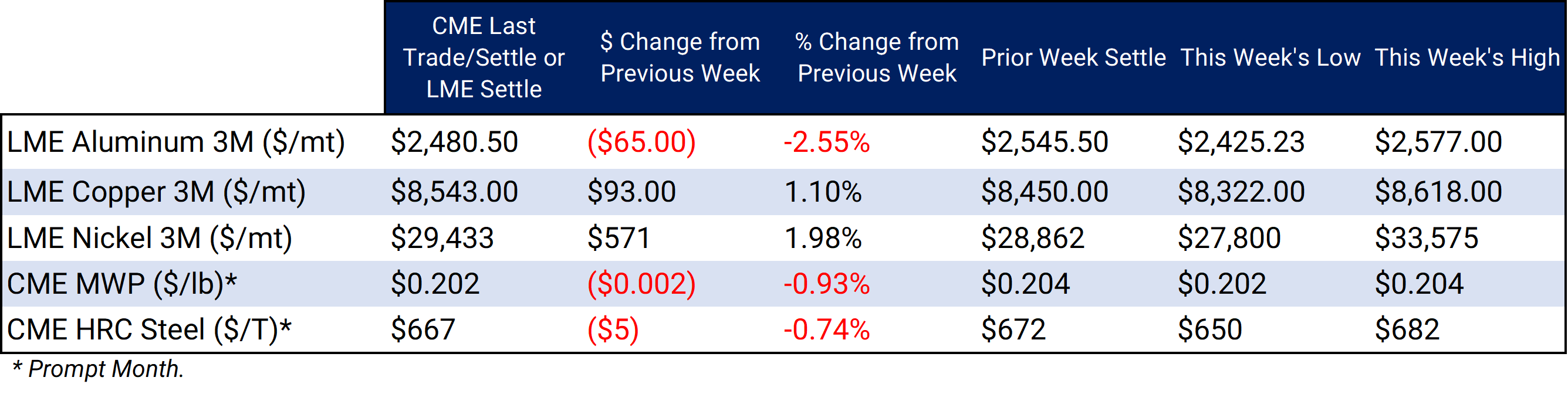

LME Aluminum 3M settled at $2,480.50/mt, down $65.00/mt on the week. Aluminum prices were down this week. Compared to last Friday, the forward curve has shifted vertically lower by about $60/mt; however, its shape remains the same. It remains in contango, meaning that nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. End-users might consider strategies that use only swaps or options or a combination of both, depending on risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 20.2¢/lb this week. The CME Midwest Premium market is in contango from the prompt month contract (December) through January 2024. Prices are flat throughout the remainder of 2024. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only.* |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,543.00/mt, up $93.00/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted higher by about $90/mt. Prices are very flat throughout the curve. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon their risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $29,433/mt, up $571/mt on the week. As prices rallied this week, nickel’s forward curve has also shifted higher, by about $570/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last settled at $667/T, down $5/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

12/07/2022: Does the Copper Rally Have Legs? 12/07/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 12/01/2022: What's Been Driving Aluminum Prices Lately? 11/17/2022: Do Chinese Aluminum Import and Export Flows Affect LME Prices? 11/07/2022: AEGIS Primer on LME Aluminum Price History |

|||||

Notable News |

|||||

|

12/9/2022: U.S. bid for battery metals has Africa blind spot 12/8/2022: WTO rules against U.S. steel, aluminium tariffs, Norway says 12/8/2022: US steel imports may fall to February '21 levels 12/8/2022: Anglo American cuts 2023 copper output target on poor Chilean ore grades 12/8/2022: Column: Copper mine supply wave arrives but will it be the last? 12/7/2022: U.S. floats new steel, aluminum tariffs based on carbon emissions 12/7/2022: Nyrstar's Auby zinc plant on care and maintenance until further notice 12/6/2022: US HRC: Prices jump on mill price hikes 12/6/2022: Glencore 2023 production outlook disappoints, shares fall 12/5/2022: US, EU weigh climate-based tariffs on Chinese steel, aluminium -Bloomberg News 12/5/2022: Volkswagen resumes production at China plants 12/2/2022: HSBC resigns as LME member after exiting industrial metals |

|||||