|

*Please note that our offices will be closed on Monday, December 26 due to the Christmas holiday. The LME and CME will be closed on Monday, December 26, and the LME will also be closed Tuesday, December 27. We will not produce the Metals First Look either morning. However, on Tuesday, December 27, our trading desk will provide CME coverage, and current clients can contact metals@aegis-hedging.com for indications. * |

|

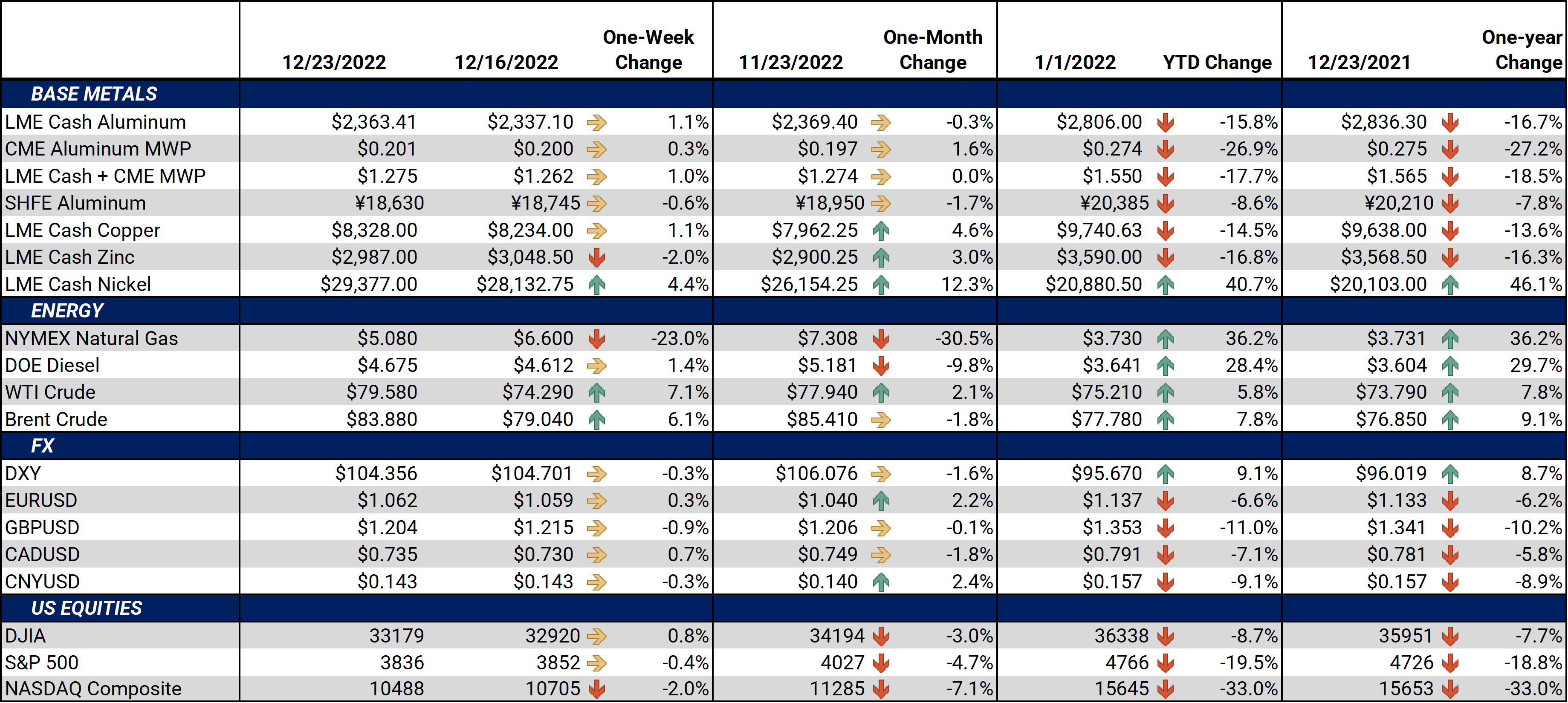

American Steel Supply & Demand Customers of American steel service centers will likely do more spot purchases in 2023, thus shifting away from longer-term contracts, according to Argus. This is an unusual move, as most service centers try to limit price exposure to the spot market. AEGIS notes that this increased spot-market exposure adds risk. However, if the spot market is tied to a hedgeable index (such as CME HRC), this risk can be easily mitigated. As for market impact, HRC prices fell throughout most of 2022, some steel buyers backed out of orders, forcing service centers to sell excess inventories at a discount. Some service centers are therefore reducing contract sizes for those customers who did not meet their contractual obligations. (Source: Argus) AEGIS agrees with Argus’s assessment that this shift to greater spot volumes could lead to greater volatility in steel prices. However, HRC end-users can mitigate this potential volatility by hedging with HRC swaps. Also, given that CME HRC prices are down over 50% from the highs of early 2022, this could be a good time for steel end-users to hedge future needs into 2023 by buying CME HRC swaps. Foreign Steel Supply & Demand India’s steel output has doubled in the past eight years, and its government would like domestic steelmakers to more than double production by the end of the decade. Currently, production is 120 million mt/yr, with an annual capacity of 154 million mt. However, the government wants domestic producers to double their production capacity to 300 million mt within the next eight years. According to their Steel Minister, India has a “tremendous” amount of infrastructure projects coming online within the next few years. Thus, steel production needs to grow rapidly. According to USGG data, India is now the world’s second-largest steel producer, bested only by China. (Source: Bloomberg, USGS) AEGIS notes that India’s appetite for steel is already growing. According to the Economic Times, steel consumption was 75.3 million mt between April and November, up 12% compared to the same period in 2021. Similarly, finished steel imports between April and November were 3.8 million mt, up 22.5% compared to the same period in 2021. Even though India normally imports little steel from the US, higher Indian demand could be bullish to CME HRC prices, if their demand for US finished-steel products increases over the coming years. Moreover, other major steel importers could be forced to look elsewhere for steel, especially if their cargoes are diverted to India. Aluminum China’s aluminum industry could have trouble sourcing raw materials starting next year. On Wednesday, Indonesian President Joko Widodo announced that the country will ban bauxite exports starting in June 2023. Bauxite is the ore that is refined into alumina, and alumina is then converted into aluminum. Most of the country’s bauxite exports go to China. The export ban on bauxite is meant to help Indonesia’s domestic processing and refining industries, according to President Widodo. Based on data from Reuters, the USGS, and Chinese Customs, China imported 17.8 million mt of Indonesian bauxite in 2021. Indonesia mined 18 million mt of bauxite that year, thus, nearly all their production was exported to China. As for Chinese imports, the country imported 107.4 million mt in 2021. That year, China’s bauxite imports mainly came from Guinea (54.84 million mt), followed by Australia (34.08 million), and Indonesia. (Sources: Bloomberg, S&P Global, USGS, Reuters, Chinese Customs) AEGIS notes that Indonesia made a similar announcement in 2021 but did not follow through on banning bauxite exports in 2022. That said, LME aluminum rallied on the more recent news, and could remain supportive if the Indonesian government stays true to its word. Nickel Russian miner Norilsk Nickel is considering lowering their output by 10% next year. The company estimates 2022 production will be 205,000 to 215,000 mt, thus, output in 2023 could range between 184,500 to 193,500 mt. Norilsk claims the potential drop in production is due to falling European demand for Russian metals. Based on USGS data, Russia is the world’s third largest nickel miner, responsible for approximately 9.3% of global nickel mine production. Production elsewhere could be on the rise. Tsingshan Holding Group Co., which is the world’s largest nickel producer, plans to open a 50,000 mt/yr plant in Sulawesi, Indonesia by July 2023. According to unnamed sources recently interviewed by Bloomberg; Tsingshan may decide to double the size of the plant to 100,000 mt/yr. Refined nickel production in the region could grow further, as two other Chinese producers, CNGR Advanced Material Co., and Zhejiang Huayou Cobalt Co. are proposing similar operations in Indonesia and China, respectively. Indonesia is the world’s largest nickel producer, according to USGS data. (Source: Bloomberg, USGS) Copper The Panamanian government has closed the Cobre Panama copper mine after the mine’s owner failed to reach an agreement over royalty payments to the government. Despite months of negotiations, the mine’s parent company, First Quantum Minerals, missed a deadline last week to agree to a $375 million/yr royalty to the government. However, First Quantum stated they are open to further dialogue. The Cobra Panama mine began operations in 2019 and is one of the largest projects brought online in recent years. According to company estimates, the mine will produce 340,000 to 350,000 mt of copper in 2022. Based on USGS figures, this equates to approximately 1.5% of global production. (Sources: Bloomberg, Reuters, USGS) |

|

|

|||||

LME Aluminum |

|||||

|

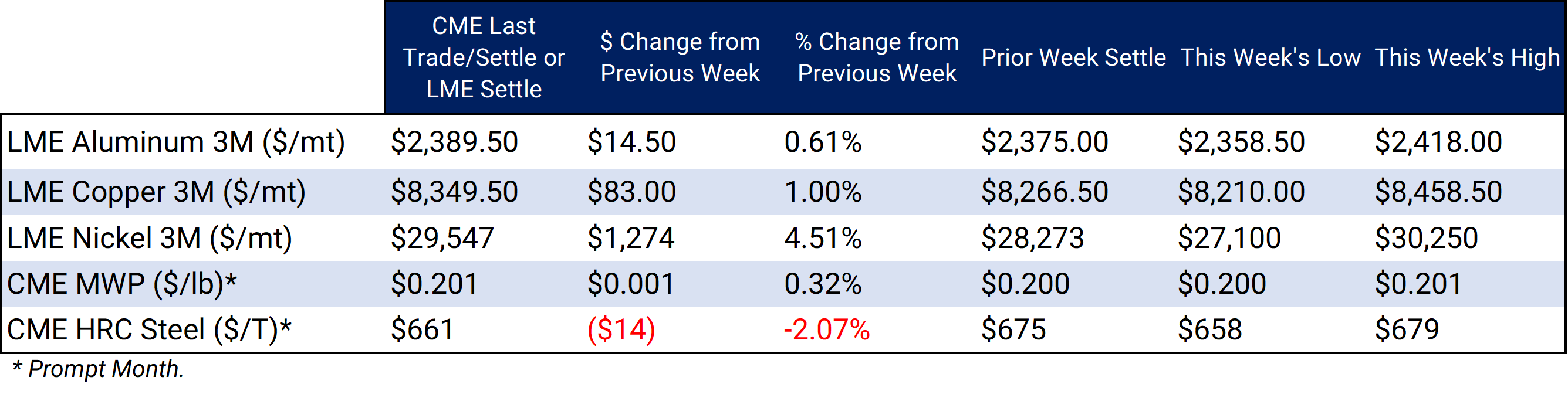

LME Aluminum 3M settled at $2,389.50/mt, up $14.50/mt on the week. Aluminum prices were up this week. However, the shape and position of the forward curve remain essentially the same as last week. It remains in contango, meaning that nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. End-users might consider strategies that use only swaps or options or a combination of both, depending on risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 20.1¢/lb this week. The CME Midwest Premium market is in contango throughout early 2023, flat between July and Dec ‘23, and then goes flat beyond Jan. ’24. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,349.50/mt, up $83/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted higher by about $80/mt. The forward curve is now in contango through June 2023 but becomes backwardated after that contract. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon their risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $29,547/mt, up $1,274/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher, by about $1,200/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last settled at $661/T, down $14/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

12/21/2022: Nickel Prices Rally While 2023 Supply Picture Remains Unclear 12/21/2022: AEGIS Factor Matrices: Most important variables affecting metals prices 12/14/2022: Could Peruvian Protests Affect Zinc Production or Prices? 12/07/2022: Does the Copper Rally Have Legs? 12/01/2022: What's Been Driving Aluminum Prices Lately? |

|||||

Notable News |

|||||

|

12/23/2022: Judge dismisses demands for LME disclosures on cancelled nickel trades 12/23/2022: East-West battleground will shift to metals 12/23/2022: Chile fires hit port and coastal city, two dead 12/21/2022: Indonesia confirms bauxite export ban to proceed as scheduled 12/20/2022: Who’s in the driver’s seat: U.S. steel and scrap dynamics 12/20/2022: USW approves new contract with US Steel 12/20/2022: US HRC: Prices rise, demand slows 12/20/2022: Column: Zinc stocks at historic lows after a year of smelter woes 12/19/2022: Tesla hits 3,000 cars a week in Berlin, Austin later than planned 12/19/2022: Norway's Hydro plans wind farm to power industrial plants 12/18/2022: China November aluminium imports fall amid rising domestic supply 12/16/2022: First Quantum mulling all legal options after Panama halts flagship mine |

|||||