|

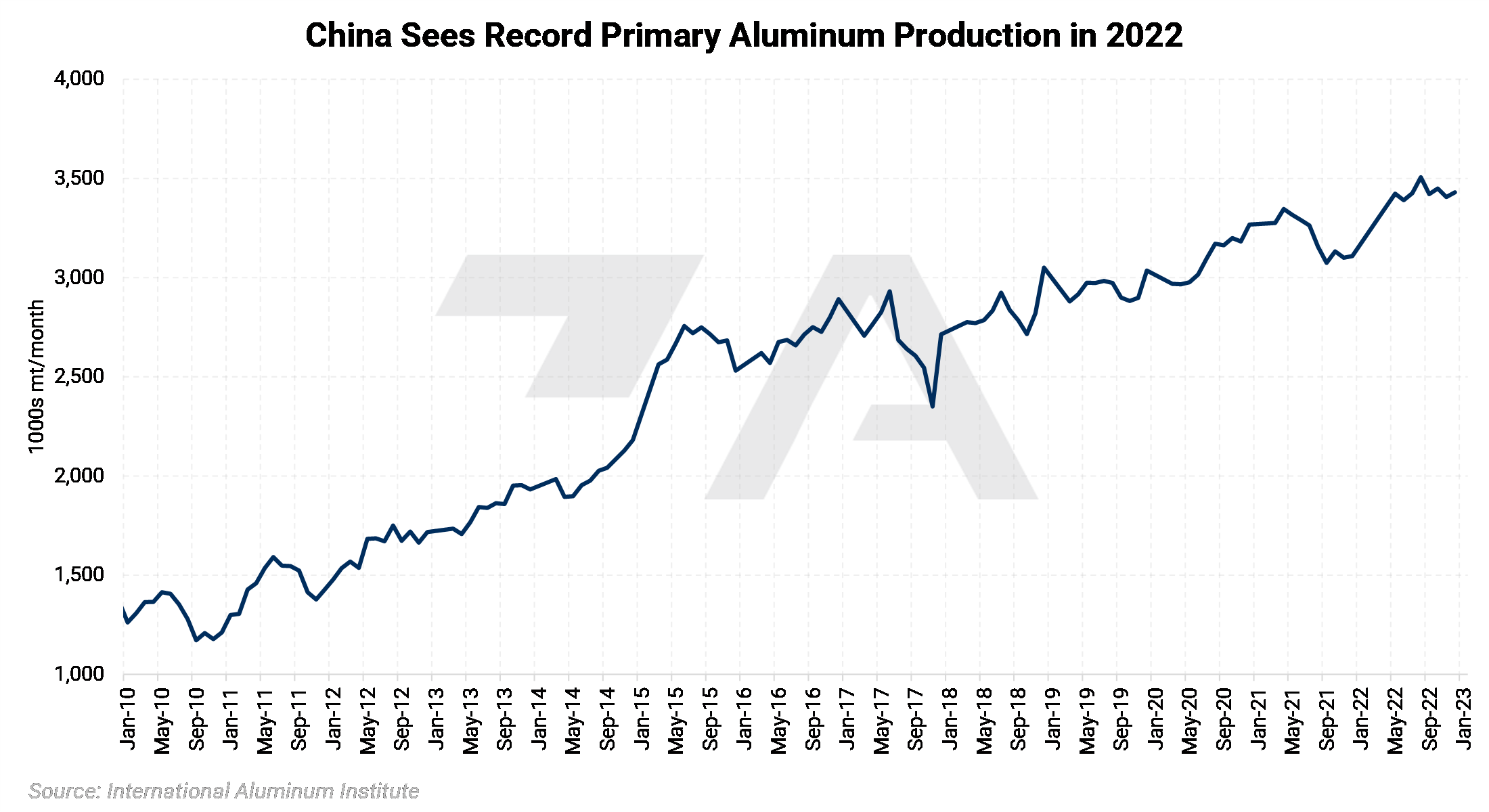

Aluminum China’s aluminum output is expected to grow in the coming years as the industry switches more production from coal to hydropower, according to Bloomberg. This expected production growth comes despite a government-mandated capacity cap of 45 million mt/yr. According to estimates, production could hit 43 million mt by 2025, up from a record 40.21 million mt in 2022. The recent aluminum supply growth was mainly due to loosened restrictions on electricity usage, as well as new smelters being brought online. The current 45 million mt/yr capacity cap was set in 2017 as part of a government effort to clamp down on emissions. |

|

|

|

AEGIS notes that China’s aluminum production expansion comes as its producers tap Indonesia for more alumina. Two Chinese metals producers, Tsingshan Group and Nanshan Group are building alumina smelters in Indonesia that will add approximately 750,000 mt to the country’s annual production capacity. Bloomberg expects Indonesia’s alumina output will hit 4 million mt this year, up 37% from 2022. (Source: Bloomberg, Reuters) We also note that the recent record in Chinese annual aluminum production comes as demand is expected to pick up this year. S&P Global believes that the country’s real estate sector will recover, and this could be a positive catalyst for aluminum demand and prices. This expected pick-up in aluminum demand is likely due to the real estate-related economic stimulus measures the Chinese government implemented earlier this month. (Source: S&P Global Insights, Reuters) |

|

|

|

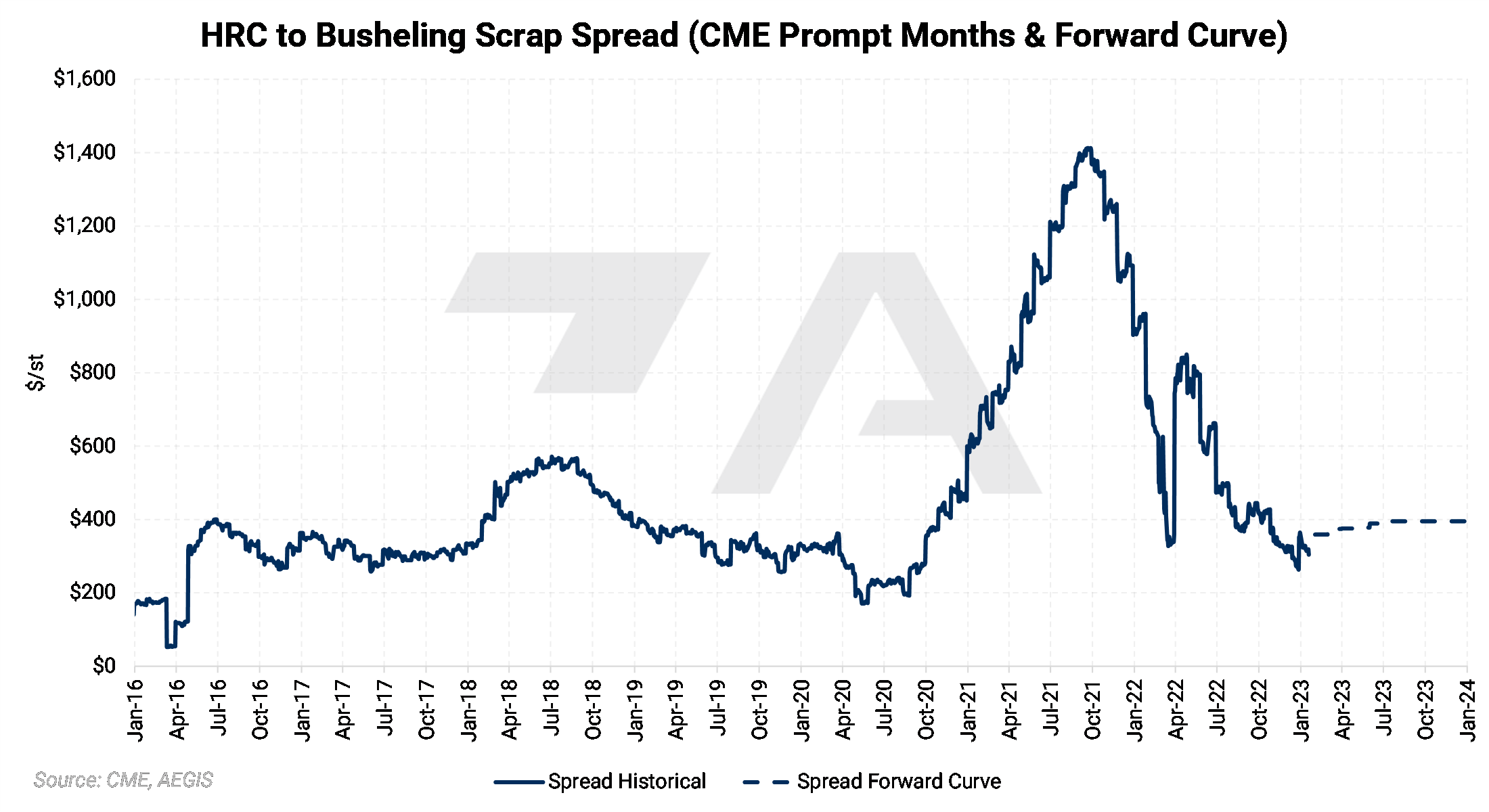

Steel Market prices for steel show that mill profitability has eroded, and forward prices don’t look much better. The HRC to busheling scrap spread was last $377/st, based on Argus’s most recent HRC and #1 busheling ferrous scrap price assessments from earlier this week. The price spread between HRC steel and busheling ferrous scrap is often used as a gauge for steel mill profitability. AEGIS notes this spread continues to drop even after the usual seasonal slowdown in November and December, as the spread sat near $424/st in mid-October. We also note that this drop in steel mill profitability comes as some large producers such as Cleveland Cliffs and Nucor are hiking prices on certain products and implementing minimum spot prices for HRC. After reaching a record $1,441/st in September 2021, this spread has steadily dropped throughout 2022 and early 2023. Based on today’s forward curves, this spread averages about $398/st throughout 2023, up slightly from the $390/st average in mid-October. (Source: Argus) |

|

|

|

The research firm AutoForecast Solutions believes that the ongoing semiconductor shortage will weigh on global automotive production this year, and there are potential consequences for both the steel and aluminum markets. AutoForecast estimates that North American vehicle production will be down 900,000 units, while European production could drop by over 800,000. As for Asia, they expect Chinese production to be down by nearly 200,000, while the rest of Asia could be lower by 700,000. This brings the total estimated global loss to at least 2.6 million units. These estimated losses for 2023 add to the nearly 8.1 million vehicles since January 2021. According to AutoForecast’s estimates, North American production has been hit the hardest, with 3.29 million total vehicles lost in 2021 and 2022. According to the American Iron and Steel Institute's (AISI) Automotive Program, the average North American vehicle contains 1,980 lbs of steel, of which approximately 1,480 lbs are flat-rolled products. Approximately 486 lbs of aluminum are used in each vehicle as well. (Source: Argus) |

|

|

|||||

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

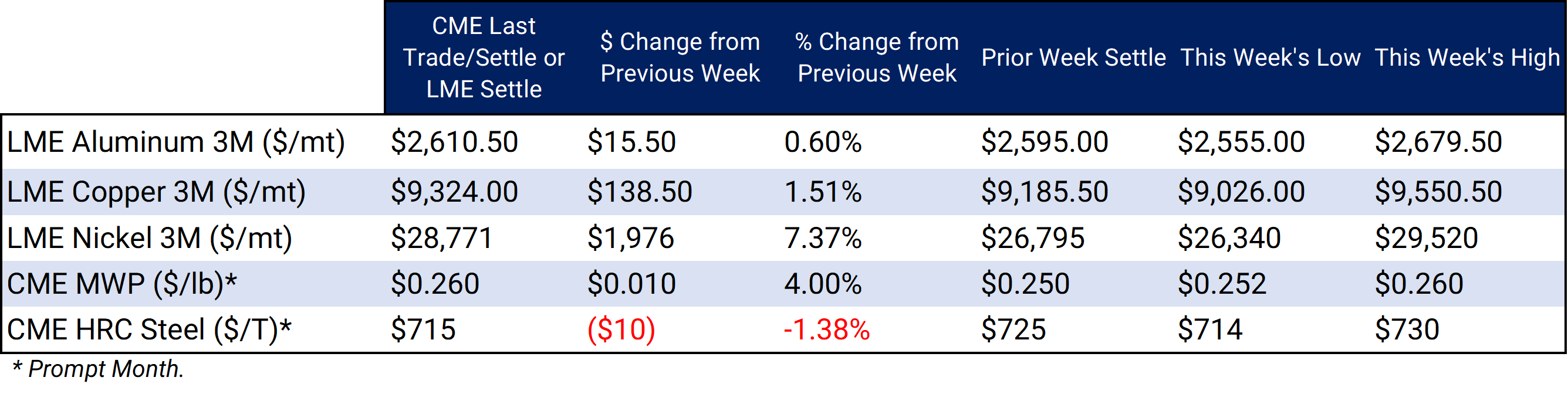

LME Aluminum 3M settled at $2,610.50/mt, up $15.50/mt on the week. Aluminum prices were up this week; however, the shape and position of the forward curve are mostly unchanged this week. It remains in contango, meaning that nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. End-users might consider strategies that use only swaps or options or a combination of both, depending on risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 26.0¢/lb this week. The CME Midwest Premium market is in contango through March 2023 but then largely goes flat for the remainder of this year. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $9,324/mt, up $138.50/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted higher by about $100/mt. The forward curve is now relatively flat throughout 2023 but becomes backwardated in 2024 and beyond. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon their risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $28,771/mt, up $1,976/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher, by about $2,000/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last settled at $715/T, down $10/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

01/18/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 01/11/2023: Nickel Prices Could Remain Volatile Into 2023 12/21/2022: Nickel Prices Rally While 2023 Supply Picture Remains Unclear 12/14/2022: Could Peruvian Protests Affect Zinc Production or Prices? 12/07/2022: Does the Copper Rally Have Legs? |

|||||

Notable News |

|||||

|

1/20/2023: Thousands march on Peru's capital as unrest spreads, building set ablaze 1/19/2023: Column: Exchanges diversify as base metals trade shrinks in 2022: Andy Home 1/19/2023: Viewpoint: India's domestic steel demand set to rebound 1/19/2023: Davos 2023: LME CEO says nickel reforms to be implemented 'relatively quickly' 1/17/2023: US HRC: Prices rise with higher offer levels 1/17/2023: EU, US resume talks on Al, steel decarb deal 1/16/2023: China's 2022 aluminium output hits record high of 40.21 mln tonnes 1/16/2023: Indonesia deploys security forces after nickel smelter protest turns deadly 1/15/2023: Column: Base metals start the new year with depleted inventory 1/13/2023: Thousands march in Peru capital demanding president step down |

|||||