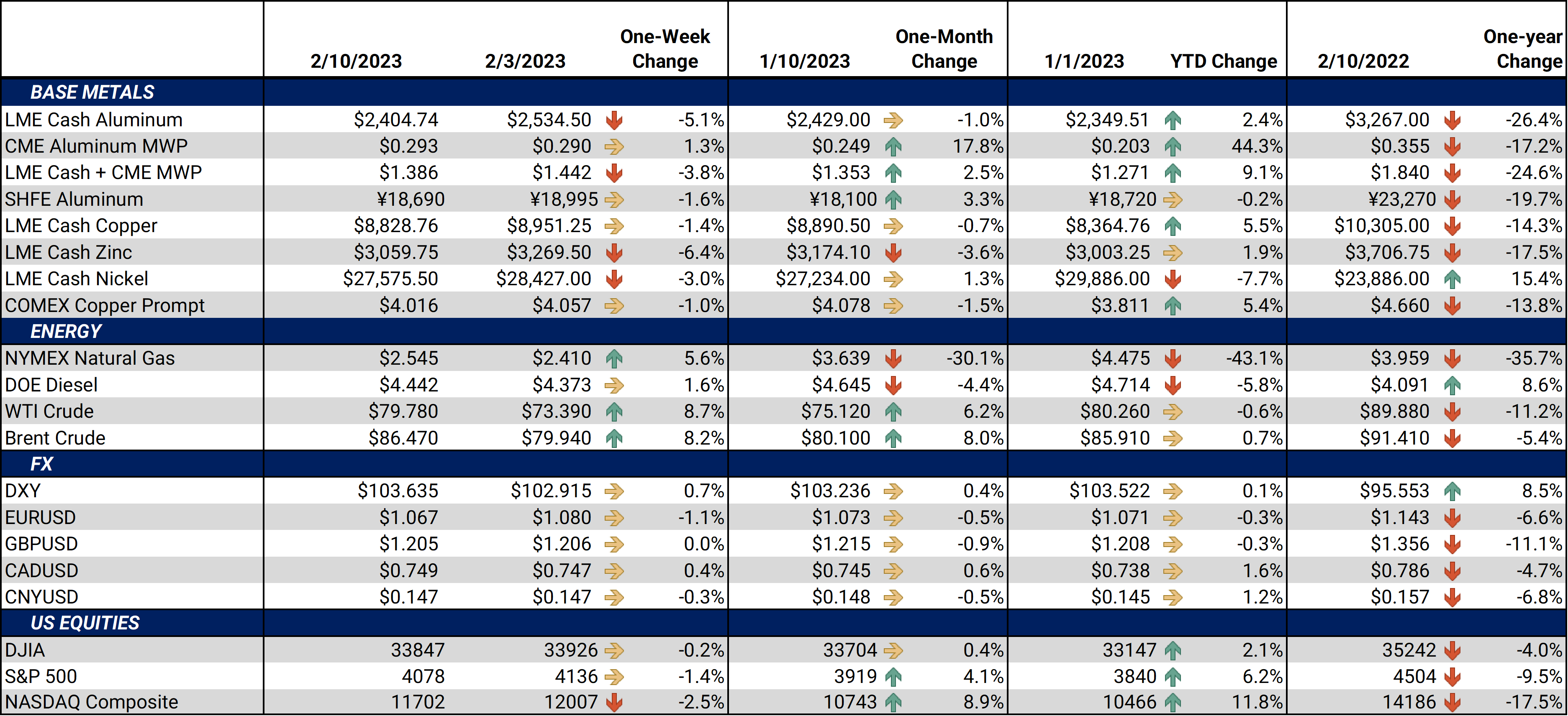

|

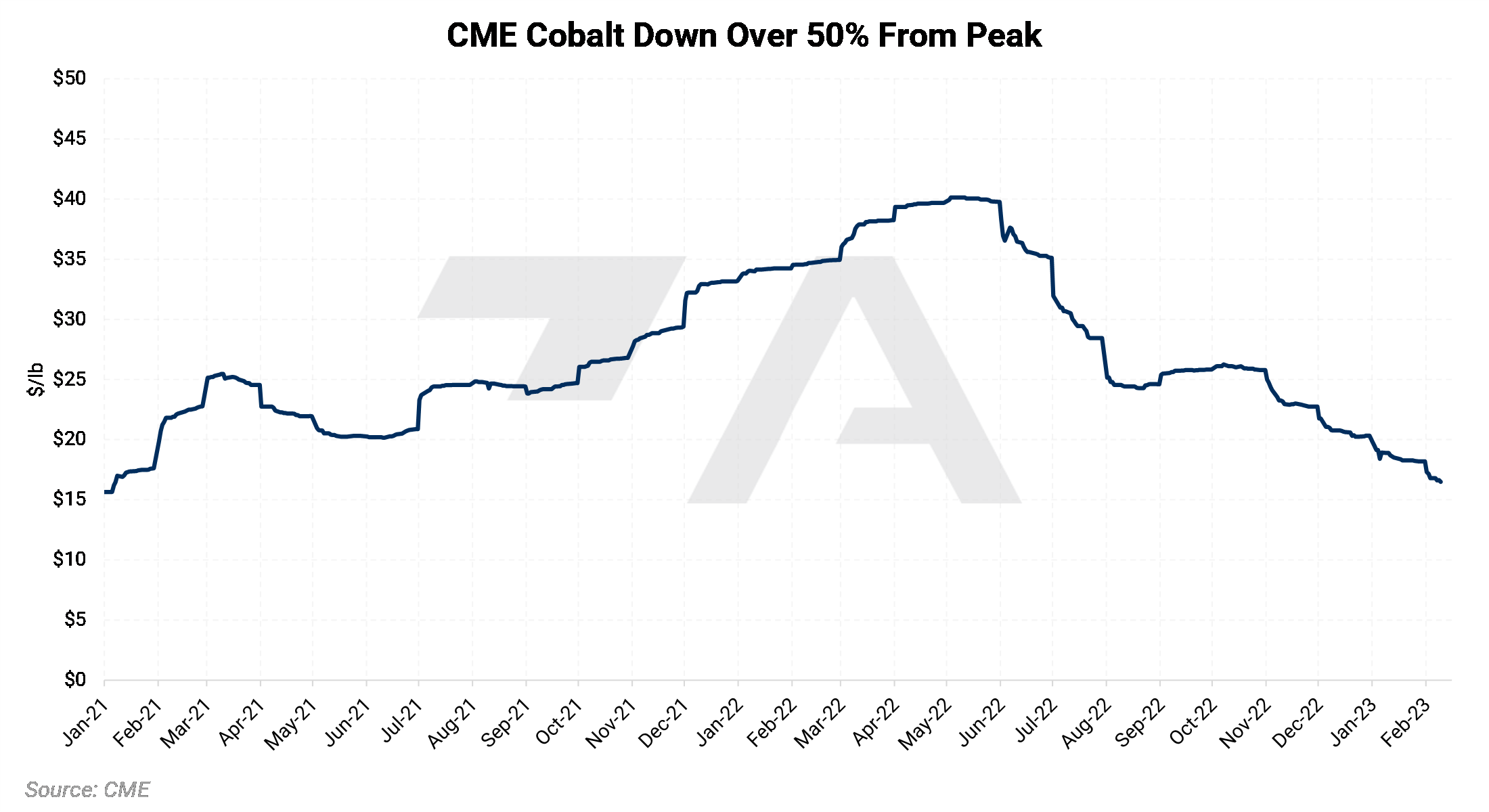

Cobalt After peaking at just over $40/lb in May 2022, CME cobalt prices have tumbled by nearly 60% due to falling Chinese demand. According to Rystad Energy, cobalt demand by China’s electronics sector has fallen by 30% to 40% over the last year. AEGIS notes that cobalt prices are especially susceptible to electronics demand. This is because electronics, such as laptops, cell phones, and tablets, require more cobalt on a “pound-for-pound” basis relative to electric vehicles. |

The EV automotive sector’s cobalt demand is still rising but could wane in the future. According to Bloomberg, car manufacturers are switching to batteries that require less or no cobalt. Moreover, some analysts predict that the automotive sector’s demand for lithium will increase while cobalt usage will fall. (Source: Bloomberg)

AEGIS notes that the financial market for cobalt has boomed in recent months. For example, aggregate open interest for CME cobalt futures is currently about 17,000 contracts, up from a mere 2,000 contracts in April 2022. The open interest is steady throughout the forward curve into early 2024. Currently, the June 2023 through May 2024 contracts all have an open interest of between 730 to 840 contracts. Please contact AEGIS for specific strategies on how to navigate that growing, yet volatile market.

|

|

|

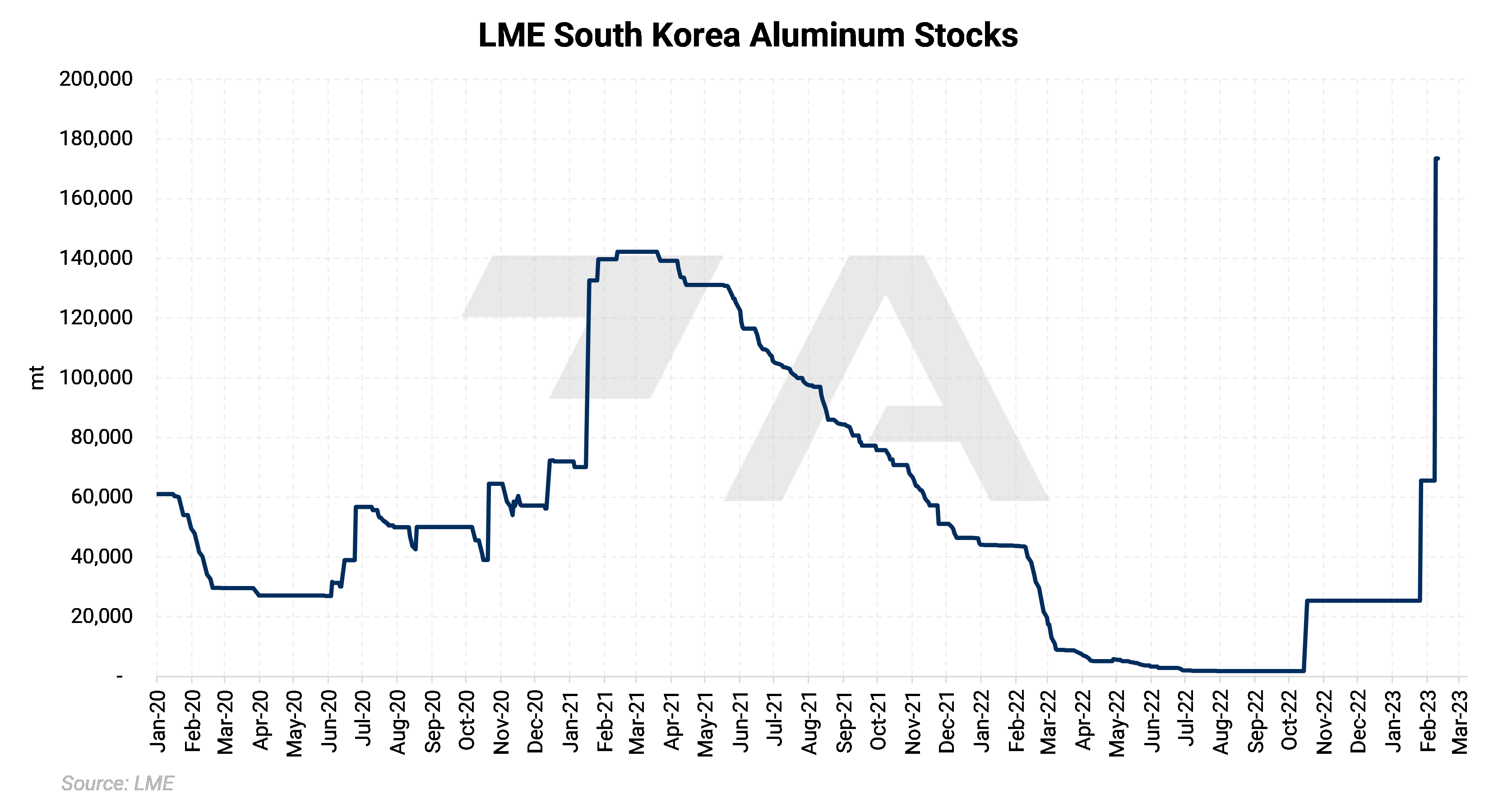

Aluminum Market participants speculate that large volumes of Russian aluminum are once again being shipped into LME warehouses in Southeast Asia. AEGIS closely monitors LME warehouse stocks, as they could represent changes in global demand. On Wednesday morning, warehouse stocks in South Korea surged to 173,500 mt, up from 65,600 the day prior. According to Bloomberg, the LME’s warehouses in South Korea are closely monitored due to their proximity to Russia’s main port for aluminum exports. Rusal, Russia’s top aluminum producer, has repeatedly denied that they would deliver into LME warehouses. However, market participants have expressed concerns that Glencore, Rusal’s top customer, could deliver large volumes into LME warehouses. |

|

|

|

AEGIS notes that Glencore was accused of similar deliveries of Russian aluminum into South Korean LME warehouses last October. At that time, AEGIS and other market participants felt that Glencore and others could have been offloading Russian aluminum due to fears the LME would ban Russian metal from the exchange. However, in November, the LME decided against such a ban, and fears that large volumes of Russian metals would be continually dumped onto the exchange eventually subsided, until recently. (Sources: Bloomberg, Reuters, LME) As stated above, large changes in LME warehouse stocks could signal shifts in global demand. If global demand slows, then traders like Glencore could unload excess inventories onto the exchange. To do this, such a trader would have to develop a sizable short position, which could pressure prices. |

|

|

|

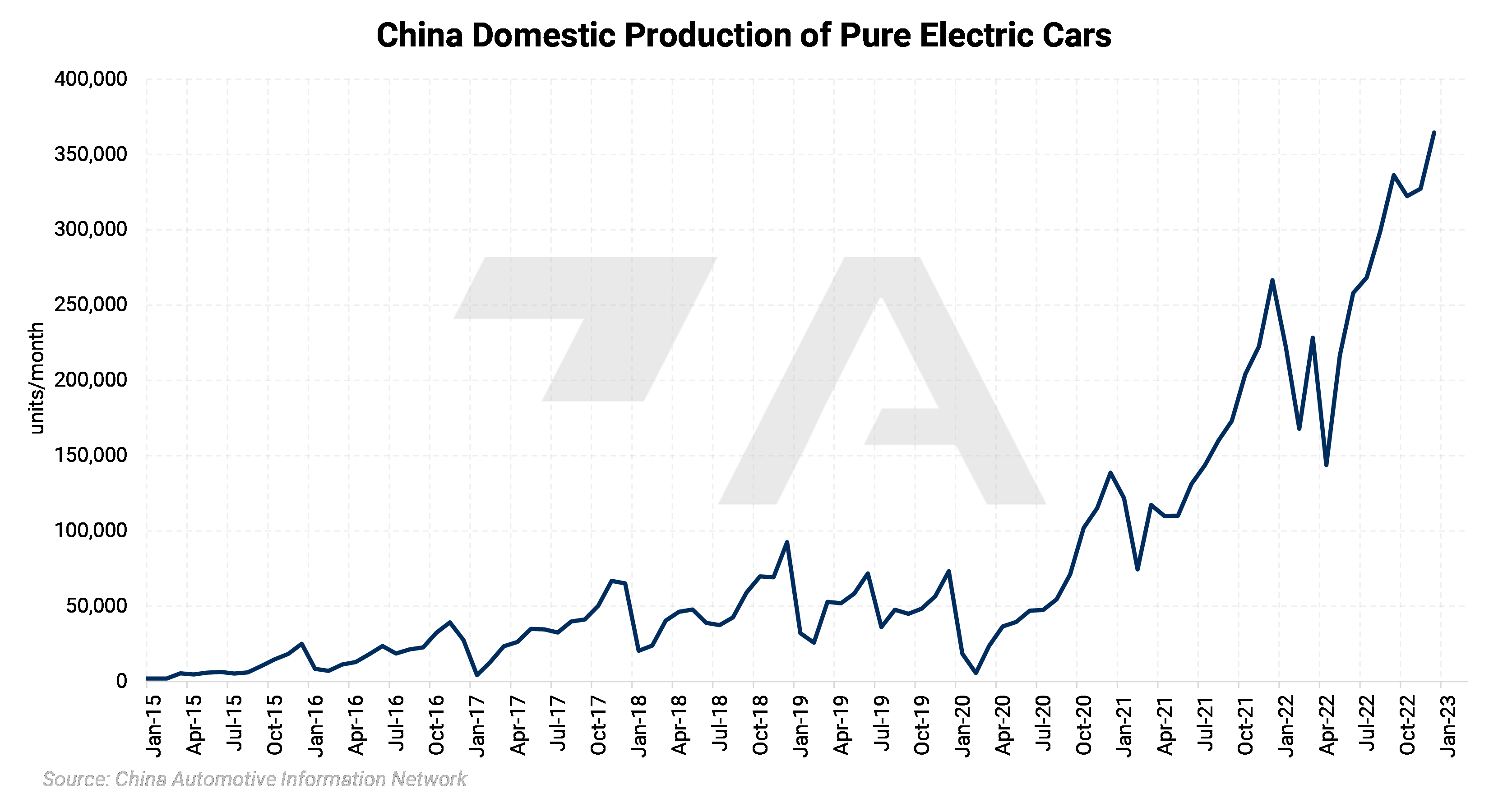

Despite growing demand, China’s aluminum market will remain in a surplus through 2025, according to Bloomberg. AEGIS notes that China produced a record 40.21 million mt of aluminum last year, and production is expected to increase in the coming years, eventually nearing the 45 million mt capacity cap. According to Bloomberg’s estimates, the expected surplus will be 768,000 mt this year. Demand growth will come from every major economic sector, except for consumer durables, thereby pushing total aluminum demand to 40.59 million mt, up 2% compared to 2022. AEGIS would like to point out one key growth area for Chinese aluminum demand. Bloomberg predicts that electric vehicle (EV) production will likely be the fastest-growing area for China’s aluminum demand. Aluminum usage for electric vehicles will grow to 2.4 million mt by 2025, up 135% from 2022. EV market share could double to 6% by 2025, and usage per vehicle is also set to increase. According to the China Automotive Information Network, the country produced over 3.15 million pure electric cars, up over 70% compared to 2021. (Source: Bloomberg) |

|

|

|||||

|

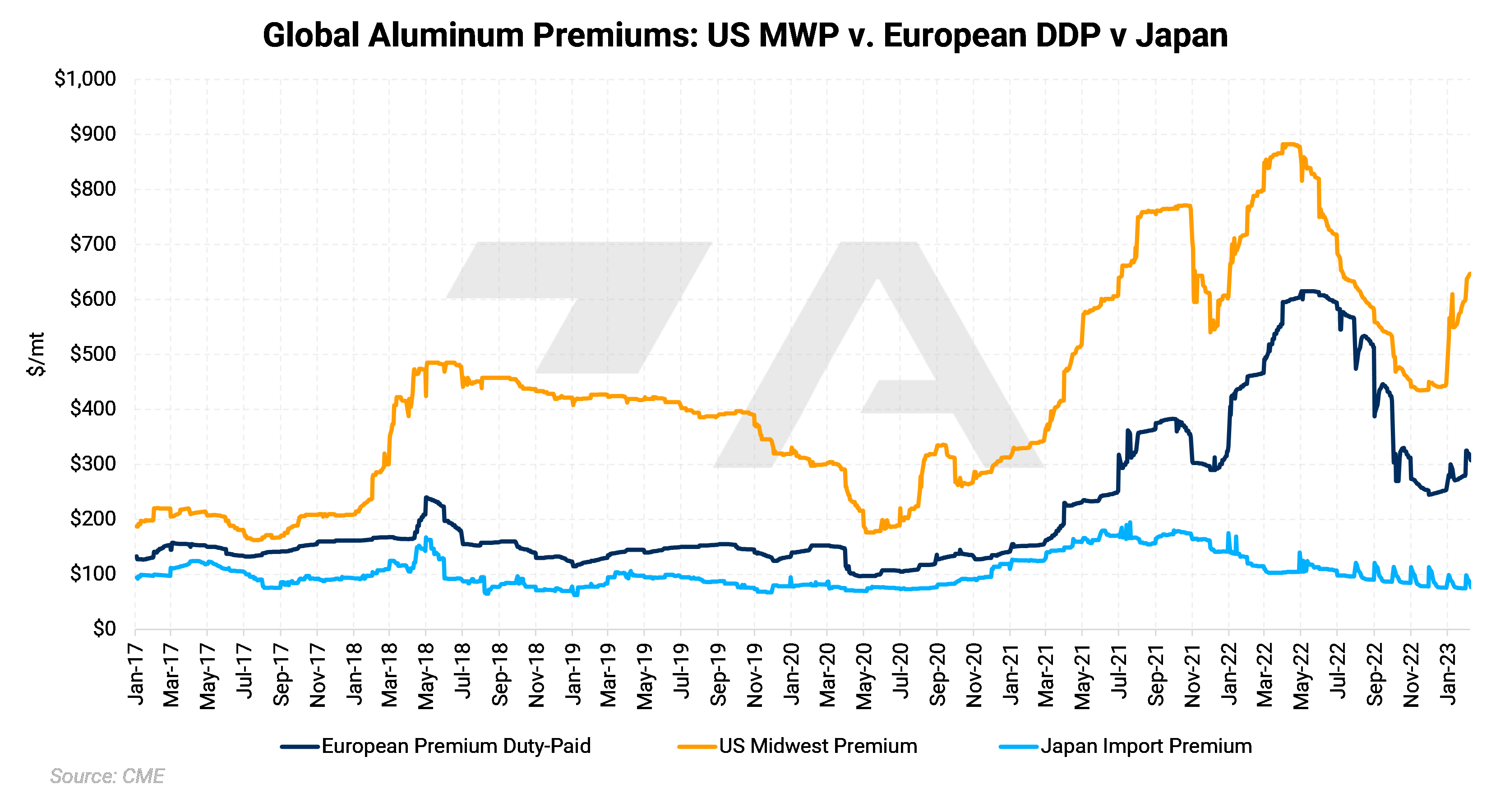

The landscape for US aluminum imports could change over the coming years. According to Bloomberg reports, the Biden administration is contemplating raising the current 35% tariff on imports of Russian aluminum into the US to 200%. AEGIS notes that Russia was the sixth-largest supplier of aluminum to the US in 2022; however, this move could effectively shut off imports from Russia. According to Bloomberg, the Biden administration had been considering the tax hike for several months but had never implemented it due to “collateral damage on US industries.” However, as the Russia-Ukraine conflict nears its one-year anniversary, the Biden administration could increase economic and political pressure on Vladimir Putin. The US imported approximately 194,000 mt of aluminum from Russia last year, down from 207,000 mt in 2021. In both 2021 and 2022, Russian volumes were approximately 3% of US aluminum imports. (Sources: Bloomberg, US Dept. of Commerce) AEGIS notes that the proposed tariff could impact aluminum prices here in the US, specifically that of the MWP. If Russian supplies drop to near zero, then US importers will need to fill the void by purchasing from other suppliers. To entice cargoes that would otherwise go to other major aluminum importers, American buyers will likely need to bid up import premiums into the US. This has already occurred before, as CME MWP prices surged after the onset of the Russia-Ukraine conflict. In fact, in late March and April 2022, the CME MWP kept climbing as global (LME) aluminum prices were falling. Shortages of high-purity aluminum and competition over units have led to a surge in international import premiums in early 2023. Several traders recently interviewed by Fastmarkets claim that most of Europe is in short supply of high-purity P0610 aluminum, and those that do have inventory are holding back sales in anticipation of higher prices. This shortage in Europe has led to a scramble to buy from international suppliers, thereby pushing up the spot European delivered duty-paid premium to $307.50/mt, up $54.50/mt since January 1. To compete for the cargoes that might otherwise go to Europe, American buyers have rallied the US aluminum Midwest Premium (MWP) to nearly $646/mt, up $198/mt since January 1. (Source: CME, Fastmarkets) |

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

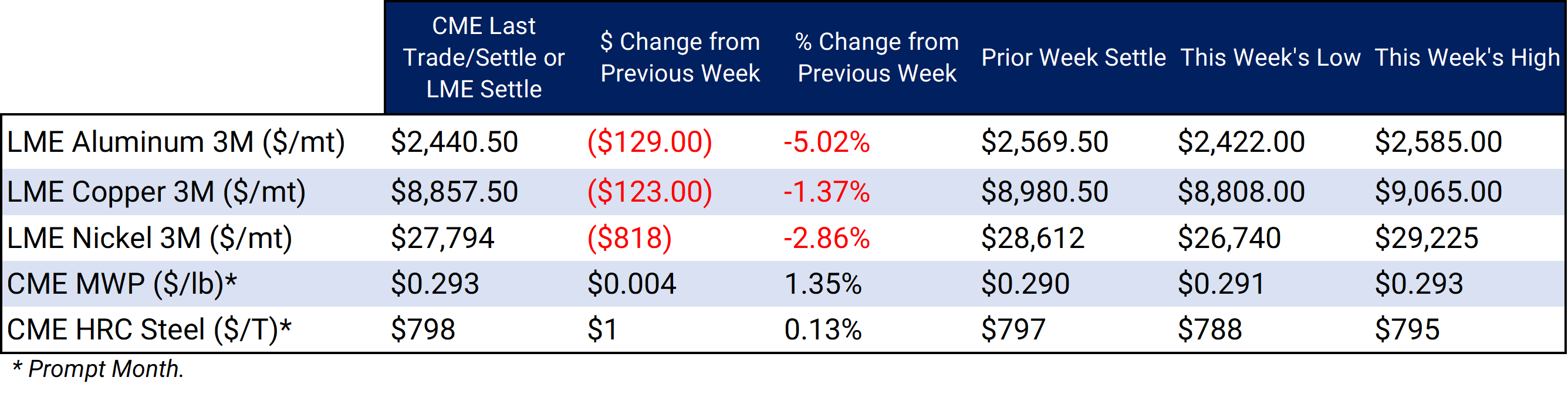

LME Aluminum 3M settled at $2,440.50/mt, down $129/mt on the week. Aluminum prices were down this week. This has caused most of the forward curve to shift vertically lower by approximately $100/mt. It remains in contango, meaning that nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. End-users might consider strategies that use only swaps or options or a combination of both, depending on risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 29.3¢/lb this week. The CME Midwest Premium market is backwardated through April 2023 but then becomes largely flat for the remainder of this year. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,857.50/mt, down $123/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted lower by about $100/mt. The forward curve is now relatively flat throughout 2023 but becomes backwardated in 2024 and beyond. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon their risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $27,794/mt, down $818/mt on the week. As prices were down this week, nickel’s forward curve has also shifted vertically lower, by about $800/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last settled at $798/T, up $1/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

02/8/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 02/07/2023: Will Aluminum's Rally Continue? 01/24/2023: Peruvian Protests Could Support Copper Prices 01/11/2023: Nickel Prices Could Remain Volatile Into 2023 |

|||||

Notable News |

|||||

|

2/10/2023: Copper heads for third straight weekly loss on weak Chinese demand 2/8/2023: Glencore deposits more Russian aluminium on LME system -sources 2/8/2023: Exclusive: Peru mines on power despite protests, though halt risk looms 2/6/2023: U.S. considering 200% tariff on Russian aluminum, official says 2/6/2023: Analysis: Dollar's gyrations raise hedging costs for U.S. companies |

|||||