|

*Please note that our offices will be closed on Monday, February 20 due to the President’s Day holiday. We will not produce a Metals First Look that morning. However, the trading desk will provide LME coverage, and current clients can contact metals@aegis-hedging.com for indications. * |

Copper

LME copper prices have trended sideways in 2023; however, AEGIS believes the prices could start to move higher on improving Chinese demand prospects and supply concerns in Indonesia and Panama. Specifically on China, the country’s real-estate sector has recently experienced falling home prices and poor sales, both of which have weighed on copper demand. However, government stimulus efforts to prop the real-estate sector could be working, as Chinese home prices rose in January, halting 16 straight months of price declines. Although this is welcome news, analysts recently told Reuters that more stimulus measures are needed to spark demand and create long-term recovery for the housing sector.

|

|

|

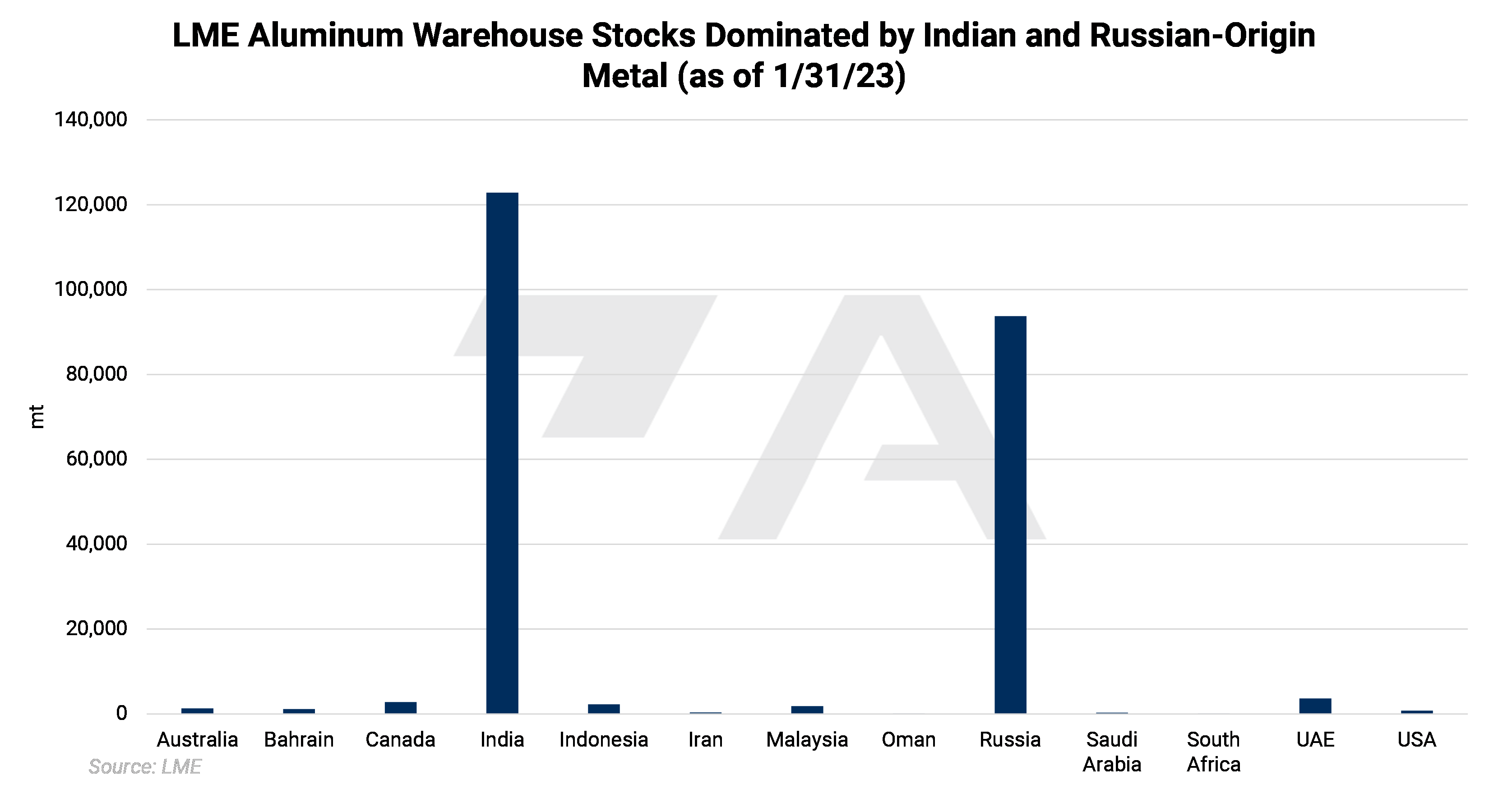

As for supply, mine closures in both Indonesia and Panama could be further supportive to copper prices. Earlier this week, Freeport-McMoRan stated it is suspending operations at its Grasberg copper mine in Indonesia due to mudslides. The Grasberg mine is one the largest in the world and is responsible for about 3% of global copper production. As for Panamanian production, operations continue at the Cobre Panama; however, an ongoing tax and royalty dispute could lead to a closure, according to its parent company, First Quantum Minerals. Based on USGS figures and company data, the Cobre Panama is responsible for approximately 1.5% of global production. (Sources: China National Bureau of Statistics, Bloomberg, Reuters, USGS) Aluminum Norwegian aluminum producer Norsk Hydro thinks that aluminum demand will increase due to improving macroeconomic conditions. As for supply, they believe that recently shuttered aluminum smelters will remain closed despite increasing aluminum prices and falling energy costs. AEGIS notes that since early 2022 falling demand has outweighed the supply constraints as of late. However, if supplies continue to fall even further, we could see an uptick in aluminum prices. Norsk Hydro essentially said as much, stating that another 600,000 tons of production capacity could be curtailed if European energy prices rise again. In a recent interview on Bloomberg TV, Norsk Hydro’s CFO proclaimed “smelters in Europe that don’t have long-term power contracts, the situation still looks challenging… We haven’t seen a lot of restarts apart from the state-subsidized ones.” Extrapolating on Norsk Hydro’s comments regarding production, AEGIS notes that only one European aluminum smelter, Aluminum Dunkerque, has announced a ramp up in production after a previous curtailment. Echoing Norsk Hydro’s comments on subsidies, we note that Aluminum Dunkerque buys most of its power through a French nuclear-power program known as ARENH, with the remainder of its power needs purchased at market prices. Moreover, approximately 1.16 million mt/yr, or 26% of Europe’s annual smelter capacity, remains offline due to poor demand or high electricity prices, based on AEGIS estimates. Are the fears of Russian metal being offloaded onto the LME overblown or on point? As of January 31, approximately 41% of the primary aluminum, or 93,750 mt, that is in LME warehouses is of Russian-origin, according to the newly initiated LME Country of Origin stock report from last Friday. AEGIS notes that the amount of Russian aluminum in LME warehouses has likely increased since January 31, and could be why LME prices have stalled this month. Last week, aluminum stocks in South Korea jumped by over 100,000 mt, and Reuters reports suggest that this metal was of Russian-origin. Glencore, who is the top-customer of Russian aluminum producer Rusal, was responsible for last week’s deliveries, according to the same reports. We also note that inflows of Indian-origin aluminum have likely increased in February and could have also added to the recent pressure on aluminum prices. On Monday morning, 91,825 mt of aluminum was delivered into Malaysian LME warehouses. According to Reuters, Malaysian LME warehouses are a known delivery point for Indian-origin metals. As of January 31, approximately 53% of the primary aluminum, or 122,850 mt, that is in LME warehouses is of Indian origin, according to the LME Country of Origin stock report. (Source: Reuters, LME) Many traders have feared that allowing large amounts of metal onto the exchange could distort global prices. The reasons behind this are two-fold. First, to deliver to the exchange, a trader such as Glencore needs to open a (likely large) short position. Opening a large short position could put downward pressure on prices. Also, delivering to the exchange likely occurs when a trader cannot find a physical buyer or end-user for the metal. This signals that market demand is falling. |

|

|

|

Battery Metals/Energy Transition Supply gluts for EV metals such as nickel, lithium, and cobalt will pressure prices this year, according to the China Nonferrous Metals Industry Association. AEGIS believes end-users of these metals can use short-term price and demand drawdowns to hedge for the long-term. Specifically for nickel, the Chinese association believes that prices will fall in 2H2023. These comments reiterate Goldman Sachs’s bearish outlook on EV metals due to “surging production.” Similarly, Rystad Energy recently stated that EV demand in China has slowed, leading to “thin” spot demand for nickel, lithium, and cobalt. Therefore, Rystad believes EV metals prices will remain subdued through 1Q2023. For all our clients, AEGIS suggests knowing, in advance, the commodity price that would satisfy your procurement budget. If that price is above current market prices, then perhaps you have the ability to wait for a potential dip in prices, then you hedge forward more aggressively. However, we must point out that these markets have sufficient liquidity to create a level of "efficiency," where known supply, demand, regulatory, etc. issues are well understood and discussed. This usually results in forward prices that already reflect market conditions. Therefore, if you are waiting to hedge on a potential decrease in prices, we prefer another tactic: hedge a "foundation" level of metal right now, if the price agrees with your budget. Use remaining volumes to average-down your cost if the market gives you such an opportunity. AEGIS notes, and believes, that this supply glut of EV metals is likely to be short-lived. An astounding 5.2 billion mt of steel, aluminum, copper, cobalt, and other metals will be required to achieve net zero global emissions by 2050, according to Bloomberg estimates. AEGIS notes that this transition could put upward pressure on most metals prices unless supply dramatically increases. We also note that multi-decade supply and demand projections are very likely to be less accurate than expected. This could lead to greater price volatility if actual supply or demand differs greatly from these initial projections. Based on Bloomberg estimates, approximately 270.5 million mt/year of steel is used for the energy transition; however, this volume will jump to almost 1.1 billion mt/year by 2050. Similarly, copper usage for the energy transition will jump nearly six-fold to 38.3 million mt/year, and aluminum demand will grow roughly five-fold to 80.3 million mt/year. (Source: Bloomberg) |

|||||

|

|

|||||

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

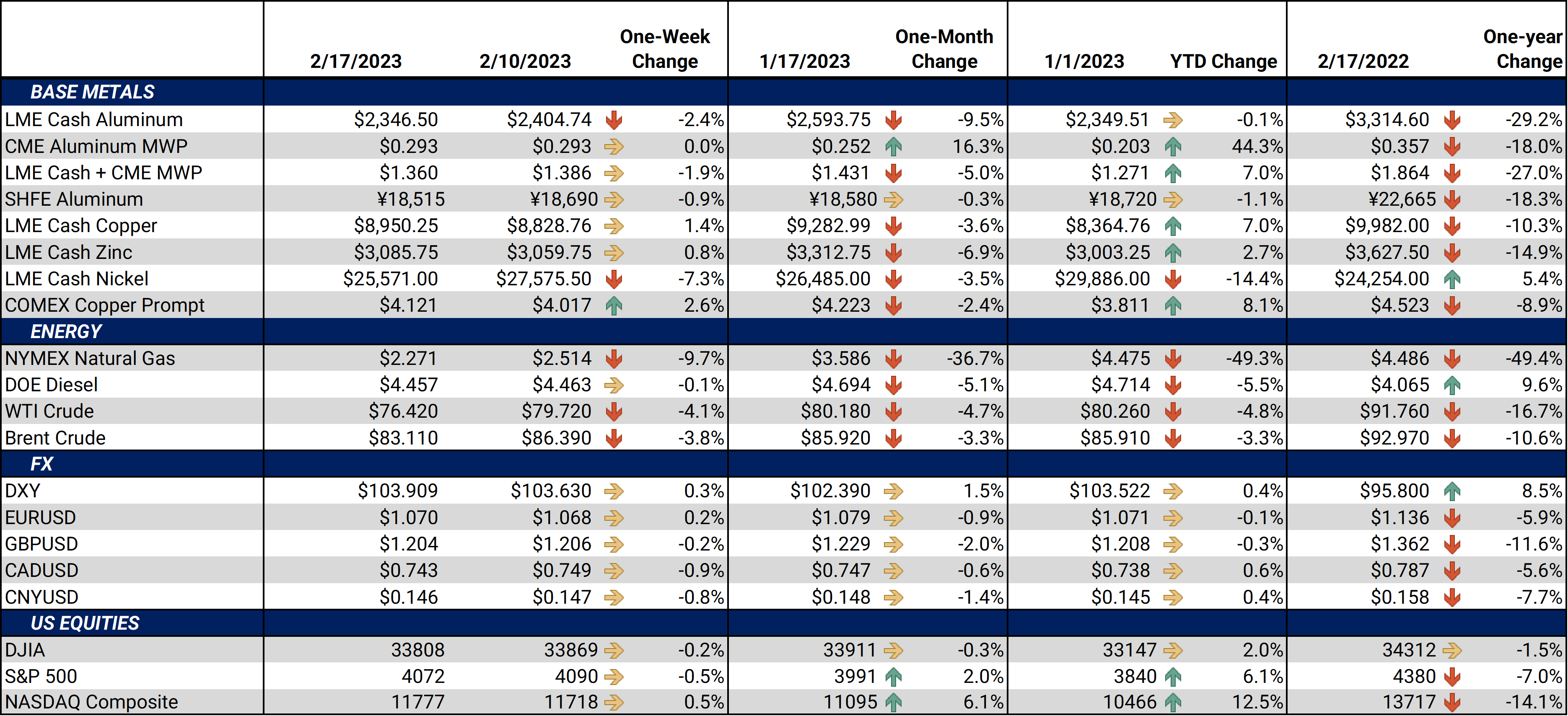

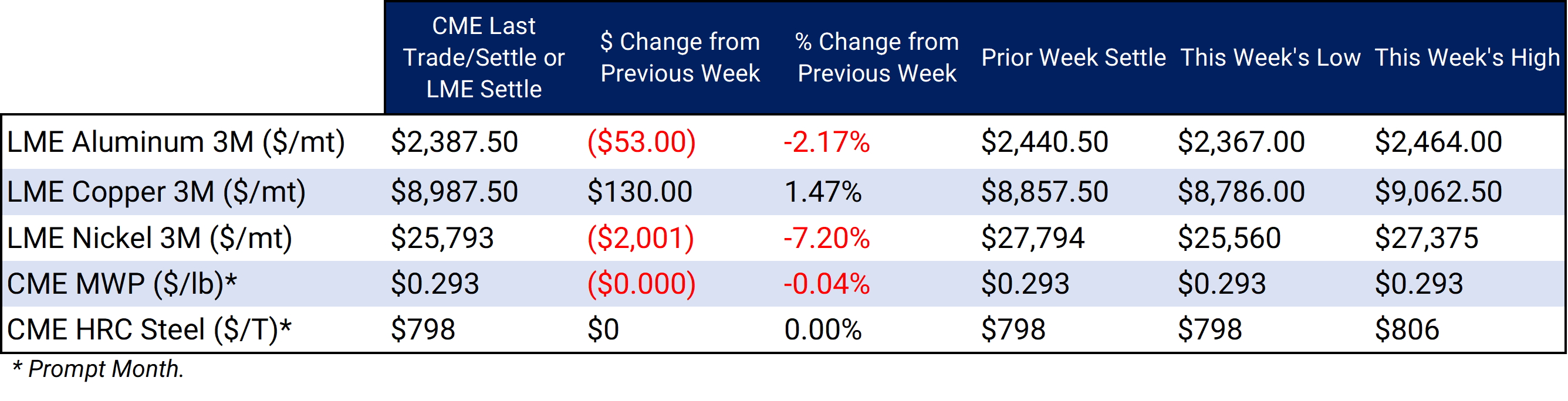

LME Aluminum 3M settled at $2,387.50/mt, down $53/mt on the week. Aluminum prices were down this week. This has caused most of the forward curve to shift vertically lower by approximately $50/mt. It remains in contango, meaning that nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. End-users might consider strategies that use only swaps or options or a combination of both, depending on risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 29.3¢/lb this week. The CME Midwest Premium market is backwardated through April 2023 but then becomes largely flat for the remainder of this year. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,987.50/mt, up $130/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted higher by about $130/mt. The forward curve is now relatively flat throughout 2023 but becomes backwardated in 2024 and beyond. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon their risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $25,793/mt, down $2,001/mt on the week. As prices were down this week, nickel’s forward curve has also shifted vertically lower, by about $2,000/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last settled at $798/T, unchanged on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

02/15/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 02/07/2023: Will Aluminum's Rally Continue? 01/24/2023: Peruvian Protests Could Support Copper Prices 01/11/2023: Nickel Prices Could Remain Volatile Into 2023 |

|||||

Notable News |

|||||

|

2/17/2023: Russians switch to used cars as sanctions pummel auto sector 2/16/2023: Exclusive: First Quantum warns employees that Panama mine may close if dispute is not settled 2/16/2023: Steep levies on Russian aluminium could threaten U.S. nickel supply 2/16/2023: Peru protests jolt mine activity with Las Bambas, Antapaccay hit hardest 2/14/2023: EU lawmakers approve effective 2035 ban on new fossil fuel cars 2/10/2023: Copper heads for third straight weekly loss on weak Chinese demand 2/9/2023: UPDATE 1-Russian metal makes up 42% of LME warehouses' stocks -report 2/8/2023: Glencore deposits more Russian aluminium on LME system -sources |

|||||