|

*The LME will be closed on Monday, August 28, due to the UK Late Summer Bank Holiday. We will not produce the Metals First Look that morning. The trading desk will provide CME coverage, and current clients can contact metals@aegis-hedging.com for indications. * |

Aluminum

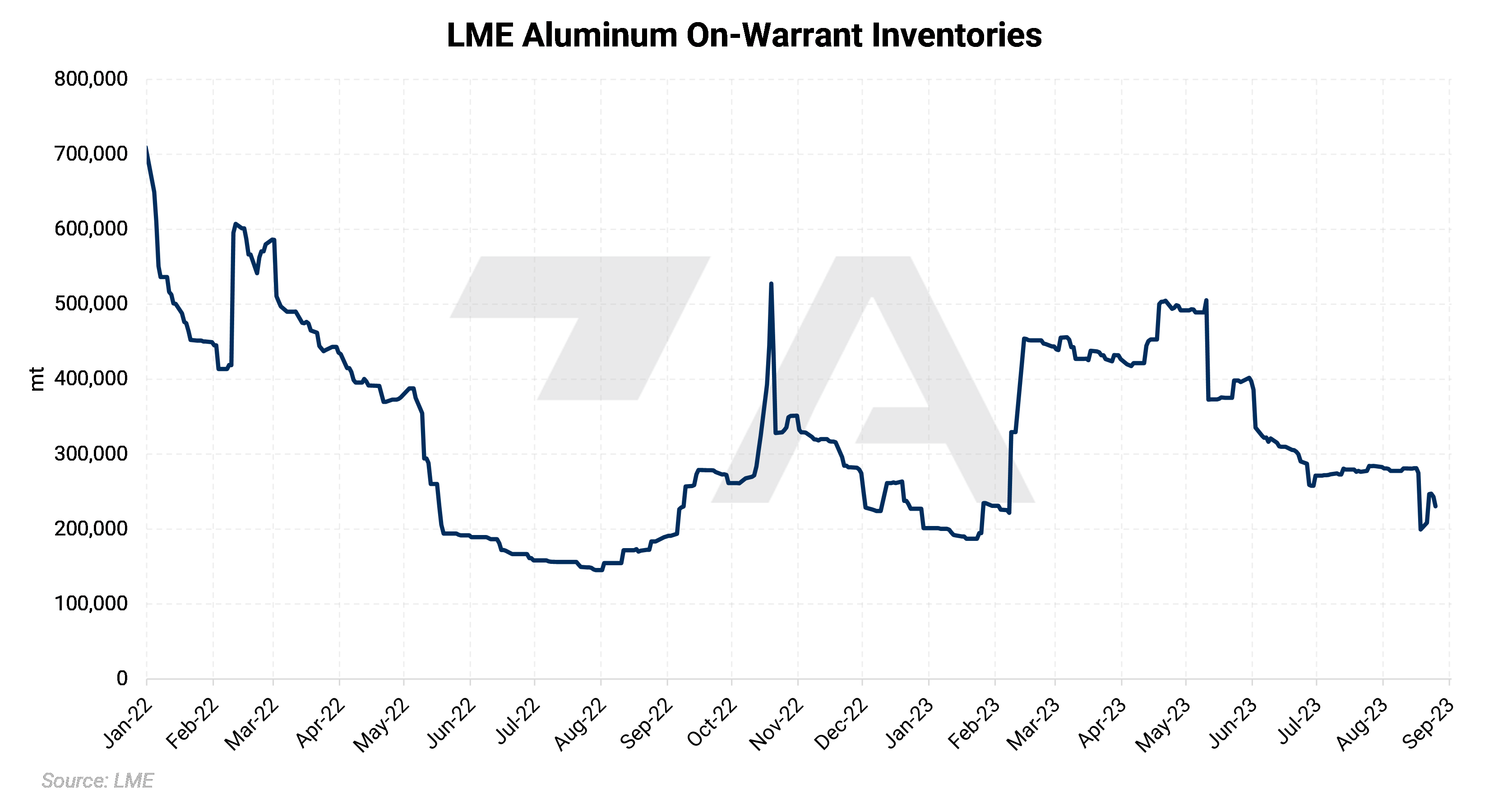

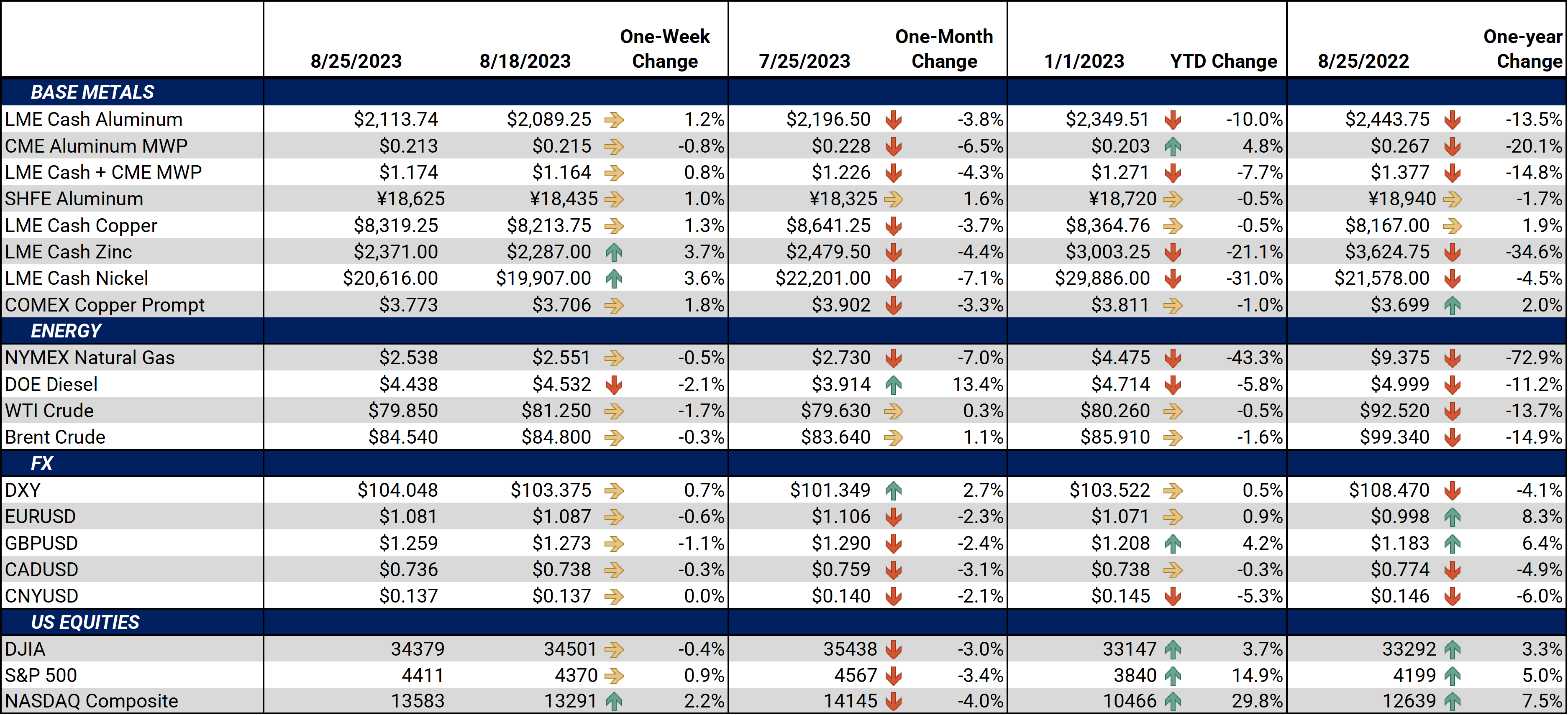

Russian aluminum supplies continue to have an oversized influence on the LME. Last Friday (August 18), the LME’s on-warrant aluminum stocks, meaning the metal is available to trade, fell to 199,425 mt, down 75,600 mt from Thursday. Nearly all this drawdown stems from cancellations in South Korean warehouses, a known repository of Russian-produced aluminum. Reuters and Bloomberg later reported that Citigroup was behind these South Korean cancellations, grabbing up $160 million, or approximately 75,000 mt, of Russian aluminum. (Source: LME, Reuters, Bloomberg)

|

|

|||

|

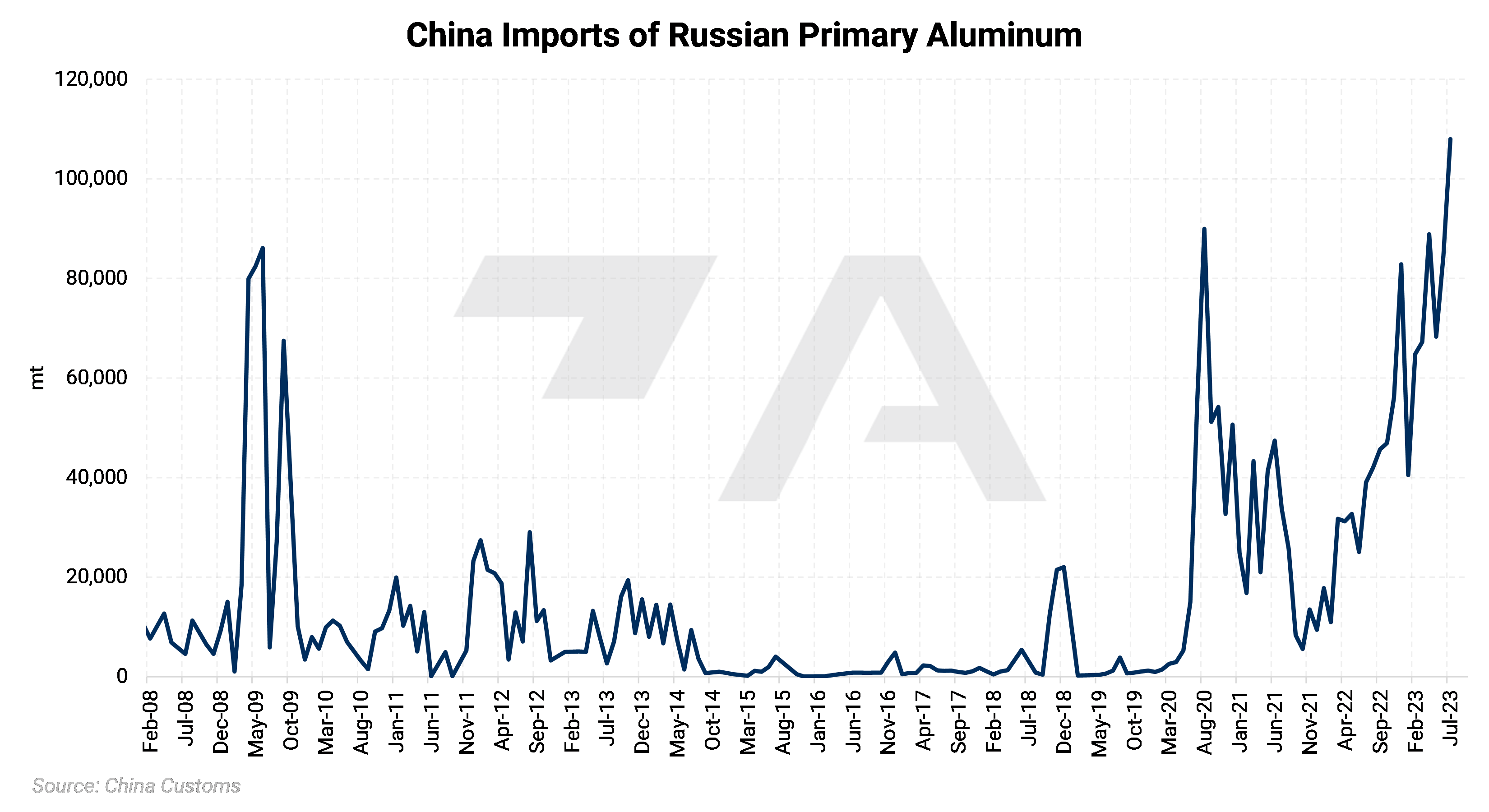

China’s imports of Russian aluminum soared to 108,000 mt in July. According to customs data that dates to 2008, this is the highest volume on record. The country imported 116,569 mt last month; therefore, approximately 93% was of Russian origin. Due in part to self-sanctioning efforts by former Western buyers, Russia has deepened its relationship with Eastern buyers, namely China. (Sources: China Customs, Bloomberg)

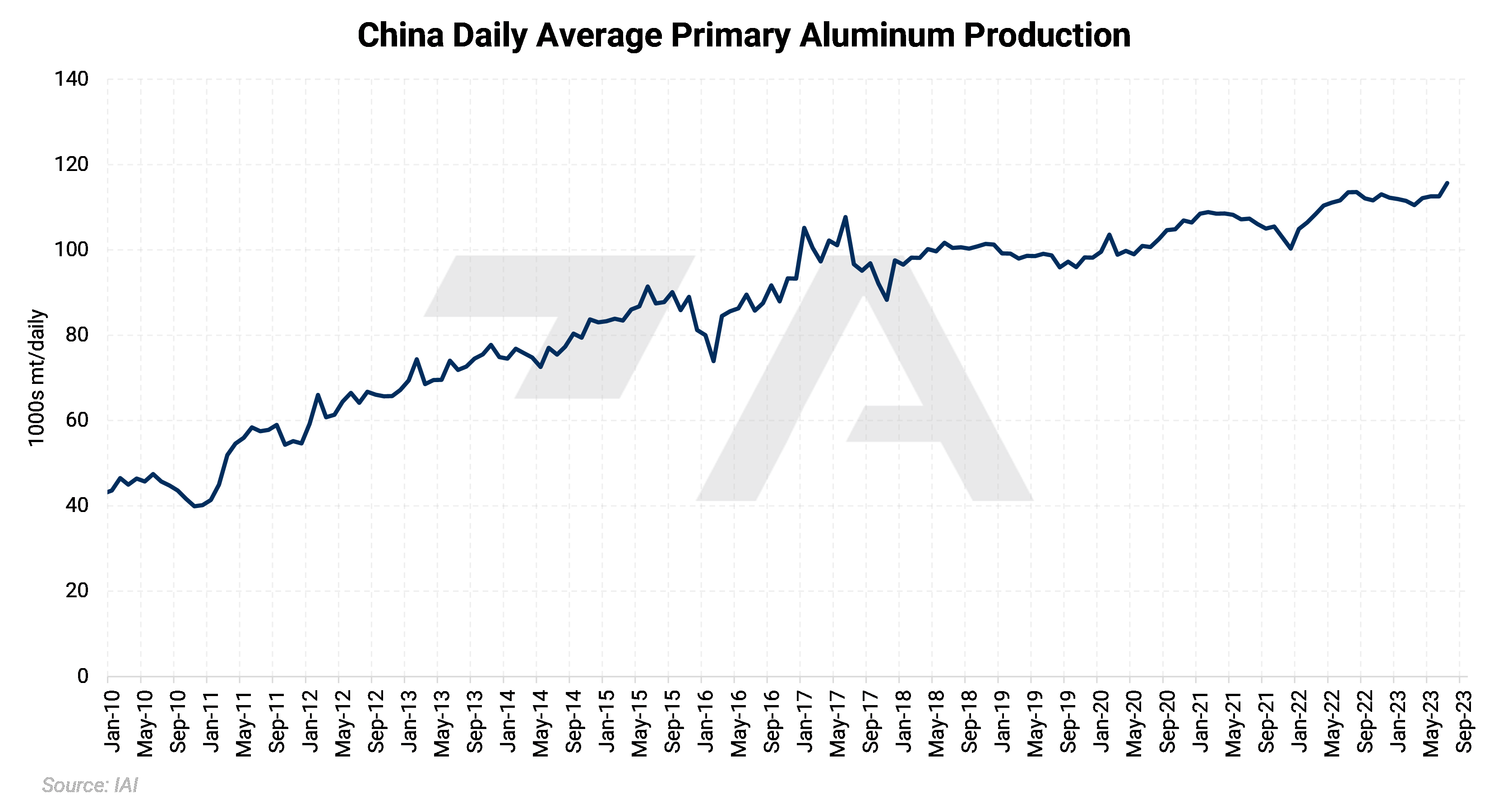

Although there is some disagreement between analysts over the exact figures, China’s aluminum production remains robust and is likely outpacing demand. According to Shanghai Metal Market (SMM), primary aluminum production hit 3.568 million mt in July, while daily production averaged approximately 115,100/mt. This uptick in production was mainly due to restarting previously curtailed smelters in the top-producing Yunnan province. According to the International Aluminum Institute, however, the country’s production averaged 111,900 mt/day in July, down slightly from the June average of 112,600 mt/day. July’s production figure is also down from the 113,500 mt/day average in July 2022.

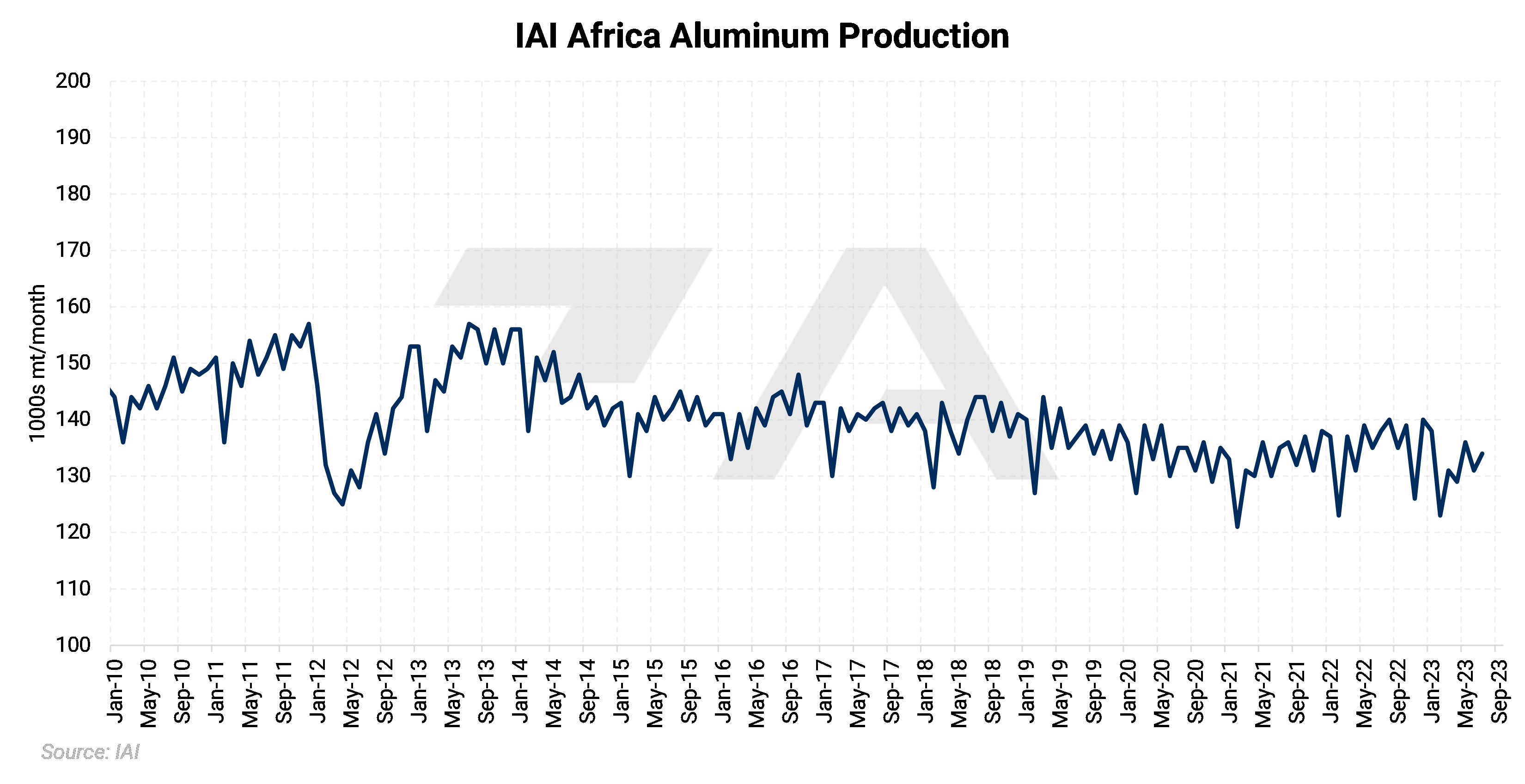

According to recent reports from the Wall Street Journal, some of the world’s top miners are diversifying into secondary aluminum production. This is mainly due to growing scrap supplies from China and the low cost of building an aluminum scrap processing facility. According to Wood Mackenzie, the cost to set up a new aluminum scrap processing facility is one-tenth the cost of building a new primary smelter. The amount of aluminum produced from scrap will grow to 42% by 2050, compared to 26% last year, Wood Mackenzie also estimates. (Source: Bloomberg) Australia-based South32, which operates two of Africa’s largest aluminum smelters, expects growth in the coming years, the company stated earlier this week. The company expects its Hillside aluminum smelter in South Africa to produce 720,000 mt in 2024 and 2025, up slightly from the 719,000 mt produced in 2023. Meanwhile, its Mozambique-based Mozal smelter should produce 365,000 mt in 2024 and 372,000 mt in 2025, up from 345,000 mt in 2023 and 278,000 mt in 2022. For both smelters, they expect production to reach near-total capacity in 2024 and 2025. (Source: South32)

Copper Analysts continue to point to China regarding the continued lackluster performance of LME copper. In a note earlier this week, ANZ bank stated, "China's beleaguered property sector shows no signs of improving…New starts and buildings under construction have fallen nearly 50% year-on-year. That looks unlikely to reverse in the short term." (Source: Bloomberg) Earlier this week, the Chinese central bank, known as the People’s Bank of China, cut its one-year lending rate by only 0.10%. This interest rate cut was slightly less than expected, leading to a tepid response by investors. Most household and corporate loans are based on the one-year benchmark lending rate, making it a critical factor in copper demand. (Source: Reuters) Due to slumping Chinese demand and falling prices for copper and other commodities, BHP’s annual profit fell by 37%, according to its 2023 annual report. Specifically for copper, the company produced 1.7 million mt, up 9% compared to the previous year. This uptick in production stems from “strong performances at Escondida, Spence, and Olympic Dam.” The Escondida mine is the world's largest copper mine and produced 1.055 million mt last year. BHP’s annual capital expenditure will grow to $10 billion this year, up from $7.1 billion last year, as the company expands operations for copper and other commodities. (Source: BHP) According to Bloomberg's latest estimates, the copper market will be balanced next year. Due to continued infrastructure buildouts, India’s copper demand will grow by 15%. Meanwhile, emerging markets in Asia will also grow by 5%. Chinese demand will remain subdued and could fall if its faltering real-estate sector does not improve. A continuously weakening Chinese real-estate sector could also weigh on domestic demand for consumer durables. Poor Chinese demand might lead to the destocking of inventories, which could also likely weigh on copper prices. (Source: Bloomberg) |

|

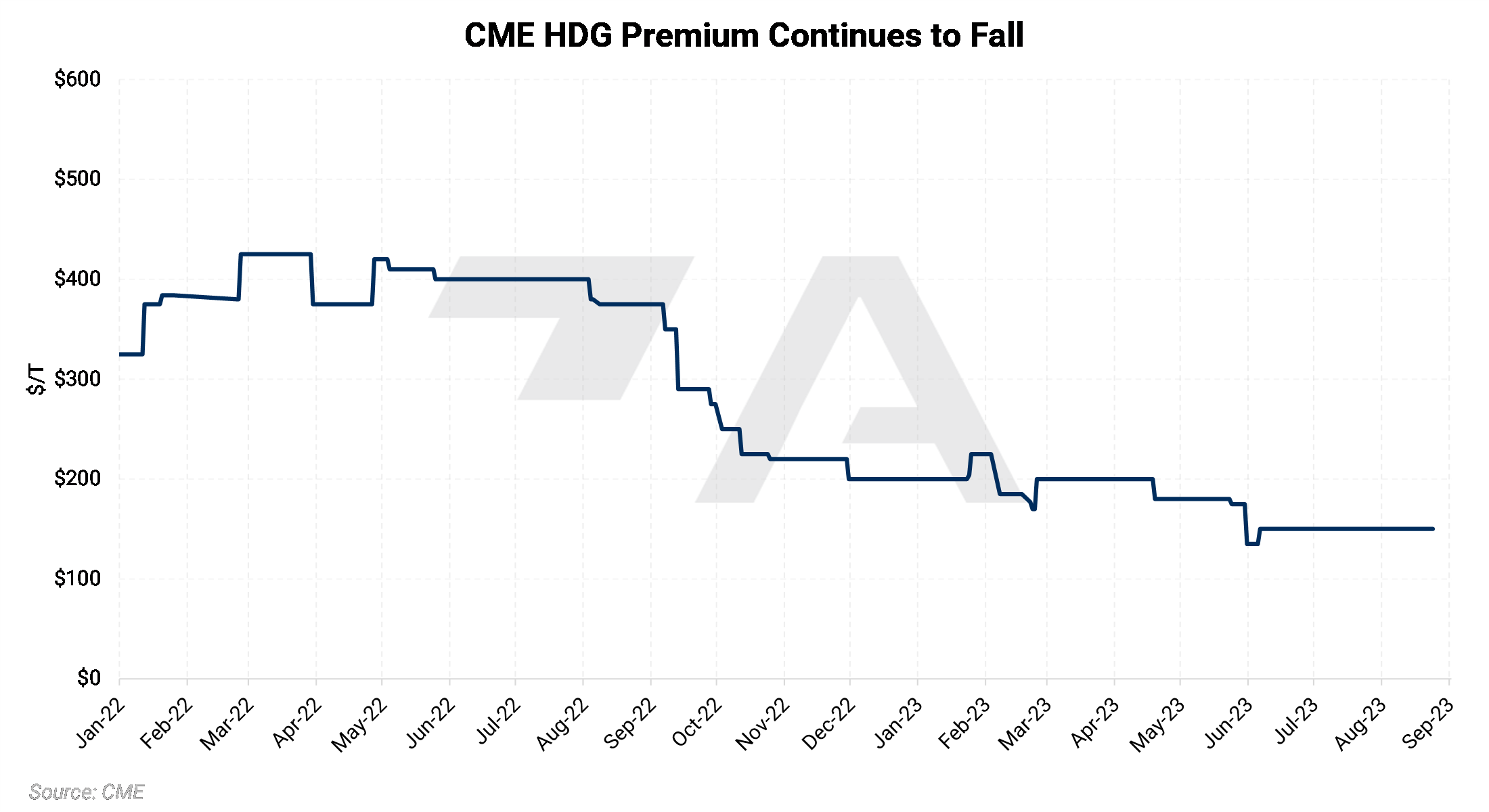

Steel Physical HRC prices continue to fall as demand remains subpar. Argus’s weekly domestic HRC assessment fell to $760/st, down nearly 37% from the high seen in early April. Reports from the SMU Steel conference suggest that steel demand for the remainder of 2023 will be “steady.” Some conference attendees fear that steel demand could fall even further if the United Autoworkers union strikes against Stellantis, GM, and Ford. (Source: Argus) The saga over the potential sale of US Steel continues. Per its labor agreement, the United Steel Workers (USW) labor union cannot block a potential buyout of US Steel, the company stated late last week. Earlier in the week, the USW indicated that it would only back a potential buyout by Cleveland Cliffs, citing Cleveland Cliffs' warm relationship with its employees. The USW had also transferred its contractual right to bid on US Steel’s assets to Cleveland Cliffs. US Steel acknowledged this transfer of rights but also stated that the rights holder cannot veto a transaction. US Steel’s current contract with the union also stipulates that a new labor agreement must be in place before a sale is finalized. (Source: Reuters, Axios) On early Tuesday, US Steel sent a letter to the United Steelworkers (USW) union stating that two conditions must be met before the company can proceed with a sale. These two requirements are that “any potential buyer would need to recognize the USW as the representative of US Steel employees” and “Any potential buyer would need to assume the terms of the existing Basic Labor Agreement.” (Source: Bloomberg) Late Wednesday, Esmark announced that it had pulled its bid to buy US Steel, citing the United Steelworkers union’s relationship with Cleveland Cliffs, a rival bidder, for rescinding its offer. Besides Cleveland Cliffs, only Arcelor Mittal has also expressed interest in US Steel. However, Arcelor Mittal, a Luxembourg-based steel manufacturing company, has yet to make a formal offer. (Source: Bloomberg) Like HRC, prices for some raw materials continue to fall. Zinc, the critical raw material in hot-dipped galvanized (HDG) steel, has experienced dramatically falling demand and prices in recent months. LME Zinc prices have dropped nearly 21% this year, while LME inventories have jumped by over 800% since early February. The CME HDG Premium, which an HDG Steel buyer can use to hedge purchases, is currently hovering near 2023 lows. (Sources: LME, CME) |

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

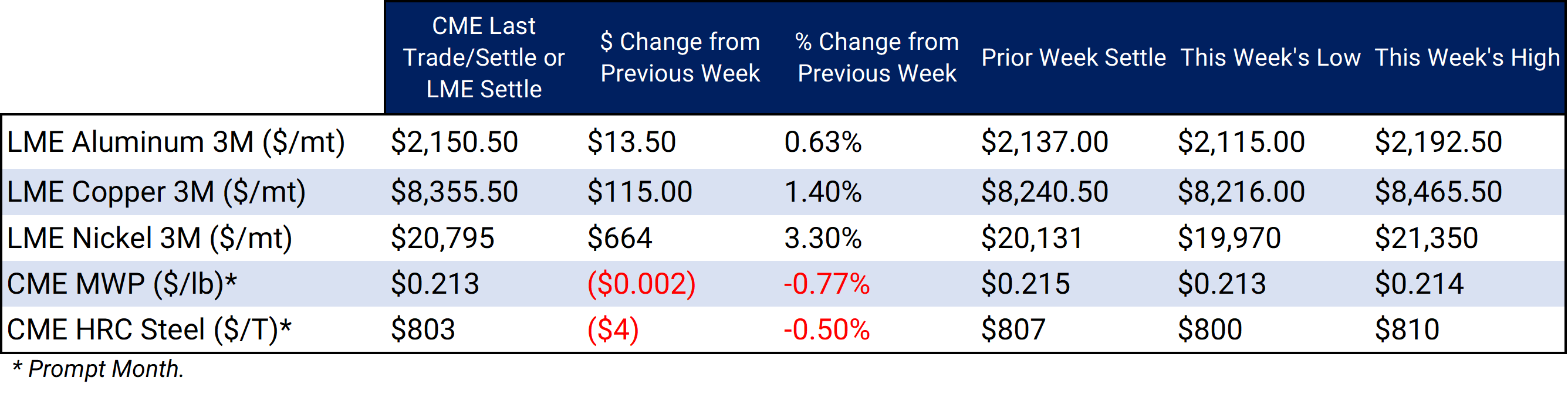

LME Aluminum 3M settled at $2,150.5/mt, up $13.5/mt on the week. Aluminum prices were up this week. This has caused the futures forward curve to shift vertically higher by approximately $10/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 21.3¢/lb this week. The CME Midwest Premium market is now in a slight contango from the September ‘23 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,355.5/mt, up $115/mt on the week. Compared to last Friday, LME Copper's forward curve has risen vertically by approximately $115/mt and remains in contango for the remainder of 2023 and throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending upon their risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $20,795/mt, up $664/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $700/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $803/T, down $4/T on the week. For CME HRC Steel, liquidity is lower than other metals for swaps, but hedging can still be done with limit orders. The same is valid for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending on risk tolerance. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

08/25/2023: Growing Secondary Aluminum Supply Could Further Weigh on Prices 08/23/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 08/18/2023: Steel Buyers Can Strengthen Pricing Power During Industry Consolidation 08/03/2023: Important US Economic Data (AEGIS Reference) 07/20/2023: Aluminum Prices Could Hinge on Chinese Stimulus 07/11/2023: Copper Prices Could Remain Subdued While African Production Grows |

|||||

Notable News |

|||||

|

8/25/2023: Codelco's new CEO Alvarado tasked with finding fixes for copper slide 8/24/2023: Column: LME warehousers bet the great metals destock is over 8/23/2023: Esmark scraps bid for U.S. Steel 8/22/2023: US HRC: Prices keep falling, sentiment weighs 8/22/2023: No new Novelis deals to buy Russian aluminium since Ukraine war 8/22/2023: Column: BHP sees China commodity demand as stable. And that's the best case 8/21/2023: Russian miners, Chinese investors interested in Polymetal's Russian assets -FT 8/20/2023: Another Chinese property giant flirts with default 8/20/2023: Citi takes delivery of Russian-origin aluminum on LME -Bloomberg 8/20/2023: Column: Trickle of LME zinc deliveries turns into a flood 8/17/2023: Focus: How U.S. Steel became an acquisition target |

|||||