|

Aluminum Aluminum prices surged this week after reports from Politico that the EU might sanction Russian aluminum. The EU’s ability to implement these sanctions remains unclear, as doing so requires a unanimous decision by all 27 EU members. Since the start of the Russian-Ukraine conflict in early 2022, trading Russian metals has been a controversial subject in political circles and the physical market, with many physical buyers and sellers shunning Russian metals. Through September 2023, approximately 11% of the EU’s unalloyed and unwrought primary aluminum imports came from Russia, down from 20% during the same period in 2022 and 2021. (Sources: Bloomberg, Reuters) |

|

|

This news could be bullish for international import premiums. Prompt month CME European Duty Paid Premium futures jumped slightly on this week’s news, but prompt month CME MWP futures were little changed. The European premium had previously bottomed in mid-December and rallied from approximately $188/mt to $225/mt as of Friday’s close. Meanwhile, the prompt month Midwest Premium has been essentially flat since mid-November, but the futures forward curve has developed in that time. If the EU does ban imports of Russian imports, both premiums could rally as the US competes against the EU for the same non-Russian metal. (Source: CME) After importing a near-record amount of primary aluminum in 2023, China’s imports could jump again this year due to a continually strong import arbitrage. The spread between SHFE and LME prices, known as arbitrage, steadily rose from January to September 2023, a move that favored imports into China. Although this arbitrage has dipped slightly in recent months, Bloomberg analysts believe China will continue to import significant volumes due to low inventories and steadying demand. (Source: China Customs, Bloomberg) After last month’s surge of Russian aluminum into the LME system, this metal could already be leaving the LME’s warehouses. Canceled warrants, meaning the metal is set for delivery, in South Korea have spiked from 5,750 mt on January 8 to 35,575 mt as of Friday. The LME’s South Korean warehouses are a known repository of Russian metal. (Source: LME) Due to “abnormally cold weather,” Magnitude 7 Metals will indefinitely shutter its Missouri-based aluminum smelter in late January, the company announced this week. Last year, the smelter produced 160,000 mt of aluminum, but this was far below capacity. Last month, Fastmarkets stated that the smelter had recently faced high energy costs and was on the verge of closing. With this closure, there will be only four US-based primary aluminum smelters operated by two producers, Alcoa and Century Aluminum. (Sources: Bloomberg, Fastmarkets) |

|

Copper Metals prices are also rallying on news that Chinese authorities implemented a stimulus measure related to bank lending. The Chinese government is also reportedly considering a stimulus package to boost the country’s ailing stock markets. This package would mainly consist of $278 billion to purchase onshore equities. Although the announcement led to an immediate surge in stock prices, some analysts downplayed the overall long-term effectiveness of this strategy as nothing concrete was announced. Some analysts were also skeptical about the impact on metals, with Sucden Financial saying that Chinese demand “will remain key in driving the general trend of the whole complex, most likely resulting in rangebound moves.” (Source: Bloomberg) Glencore and Trafigura want Chinese copper smelters to use spot refining fees for 2024 refined copper production rather than setting long-term contracts; the companies stated late last week. These fees, known as treatment charges, were usually set yearly between smelters and large miners such as Trafigura and Glencore. Spot treatment charges in China have fallen dramatically in recent months due to low copper supply amid poor end-user demand. Glencore and Trafigura also want these smelters to agree to a cap on these fees in case supply or demand increases. (Source: Reuters) JCHX Mining Management Co., a Chinese mining construction contractor, will buy an 80% stake in Zambia’s Lubambe Copper Mine. JCHX will also invest $114 million into expanding the mine’s production, with output expected to reach 32,500 mt/year. This purchase is part of a growing trend of Chinese metals producers buying controlling stakes in foreign mining operations. (Source: Bloomberg) Chile’s state-owned copper miner, Codelco, will soon issue more debt to finance ongoing and new projects, the company announced this week. This new debt issuance comes four months after the company sold $2 billion of bonds that were earmarked for current projects that were over budget and behind schedule. Yesterday, Codelco also announced that it will buy Lithium Power International Ltd. This is Codelco’s first lithium asset and a key component to its plans to diversify and increase its revenue streams. Codelco has suffered through many production issues recently, leading to declining revenue and forcing the debt-ridden company to further tap into global debt markets. (Source: Bloomberg) US-based Freeport McMoran, one of the world’s largest copper miners, stated that 4Q2023 copper sales totaled 1.1 billion lbs, slightly higher than what it predicted in October. As for 2024, the company expects to sell 1 billion lbs of copper in Q1, and total annual sales will be 4.1 billion lbs. The sales goal for 2024 is in line with 2023. (Source: Bloomberg) |

|

Steel Prices for zinc, a key raw material for hot-dipped galvanized (HDG) steel production, remain rangebound despite recent mine closures. Similarly, investment funds, purely speculators in metals markets, remain ambivalent about zinc. As of last Friday, these funds are net long a mere 1,653 contracts, their smallest position in nearly a month. This is likely why LME zinc prices have trended sideways to lower in January. (Source: LME) Continuing on raw materials, prices for nickel, a key raw material for stainless steel production, continue to fall due to poor demand amid ample inventories. Yesterday, the benchmark LME 3M closed at $16,000/mt, its lowest close in nearly three years. As BMO Capital Markets recently stated, “The pressures in the global nickel market are becoming increasingly apparent. We have noted that further temporary or permanent capacity cuts were required to balance the nickel market following last year’s surplus, but it is yet to be seen whether sufficient adjustment has taken place.” (Source: Bloomberg) Tata Steel, one of the world’s largest steelmakers, will shutter its two UK-based blast furnaces due to unprofitability, the company announced last Friday. The two blast furnaces have a combined production capacity of 5 million mt/year but have only been producing 3.2 million mt/year recently. They also stated that the decommissioning process will be completed by the end of 2024. These blast furnaces will be replaced by a more efficient, less polluting 3 million mt/year electric arc furnace that will start steel production in 2027. (Source: S&P Global, Reuters) Continuing on Tata Steel, the company returned a profit of $61.7 million last quarter as lower costs helped offset declining revenue. While reporting earnings earlier this week, Tata’s CEO highlighted several recent concerns, stating “Global operating environment has been complex, with economic slowdown in China and geopolitics weighing on commodity prices in general. During this quarter, China has exported between 7 to 8 million tons of steel every month, which is the highest since 2015 and this has adversely impacted global steel prices as well as profitability.” He later added that India remains a growing market. (Source: Bloomberg) Like Tata Steel, another one of India’s largest steelmakers, JSW Steel, had stellar results this past quarter. “India’s economic growth remains strong, led by the momentum in manufacturing and investments in infrastructure,” JSW proclaimed during its earnings release. They also reiterated that weaker global markets and increasing raw steel imports remain a concern. (Source: Bloomberg) |

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

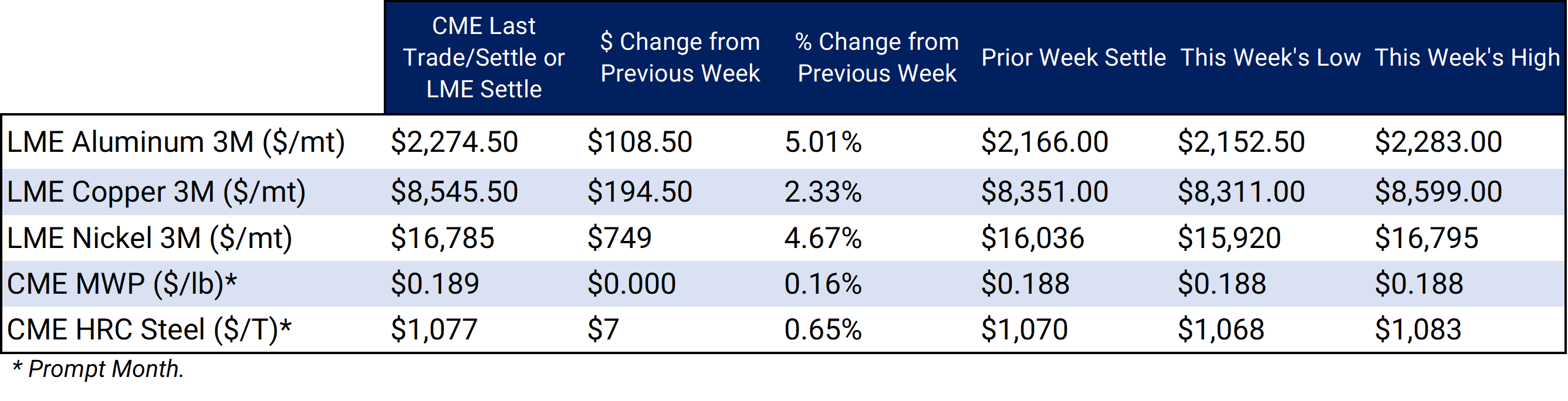

LME Aluminum 3M settled at $2,274.5/mt, up $108.5/mt on the week. Aluminum prices were up this week. This has caused the futures forward curve to shift vertically higher by approximately $110/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 18.9¢/lb this week. The CME Midwest Premium market is now in a contango from the February ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,545.5/mt, up $194.5/mt on the week. Compared to last Friday, LME Copper's forward curve has risen vertically by approximately $200/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $16,785/mt, up $749/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $750/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $1,070/T, down $6/T on the week. Steel mill profit margins improved dramatically throughout 3Q and 4Q2023 and are also starting 2024 on a good note. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $650/st, up from about $320/st on September 1. This is mainly due to prompt month CME HRC steel futures rallying alongside prices in the physical market. Since steel prices have increased significantly recently, mills should consider hedging production and raw material usage for 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

1/25/2024: Aluminum Starts 2024 On a Down Note, But Potential Supply Shocks Give Consumers a Reason to Hedge 1/24/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 1/11/2024: Important US Economic Data (AEGIS Reference) 1/4/2024: Year-End Review of LME Aluminum, Copper, CME HRC Steel and Hedging Implications for 2024 12/8/2023: Aluminum and Copper Markets Diverge but Hedging Opportunities Persist for End-Users |

|||||

Notable News |

|||||

|

1/24/2024: Morning Bid: Shoring up confidence in fragile China 1/24/2024: Japan's Nippon Steel exec meets US Congress members amid US Steel deal 1/23/2024: Funds sell copper as weak demand trumps supply pressures 1/23/2024: Aluminum price jumps after report EU may sanction Russian metal 1/23/2024: China's Surge in EV Exports to Europe Sparks Aluminum Industry Concerns |

|||||