|

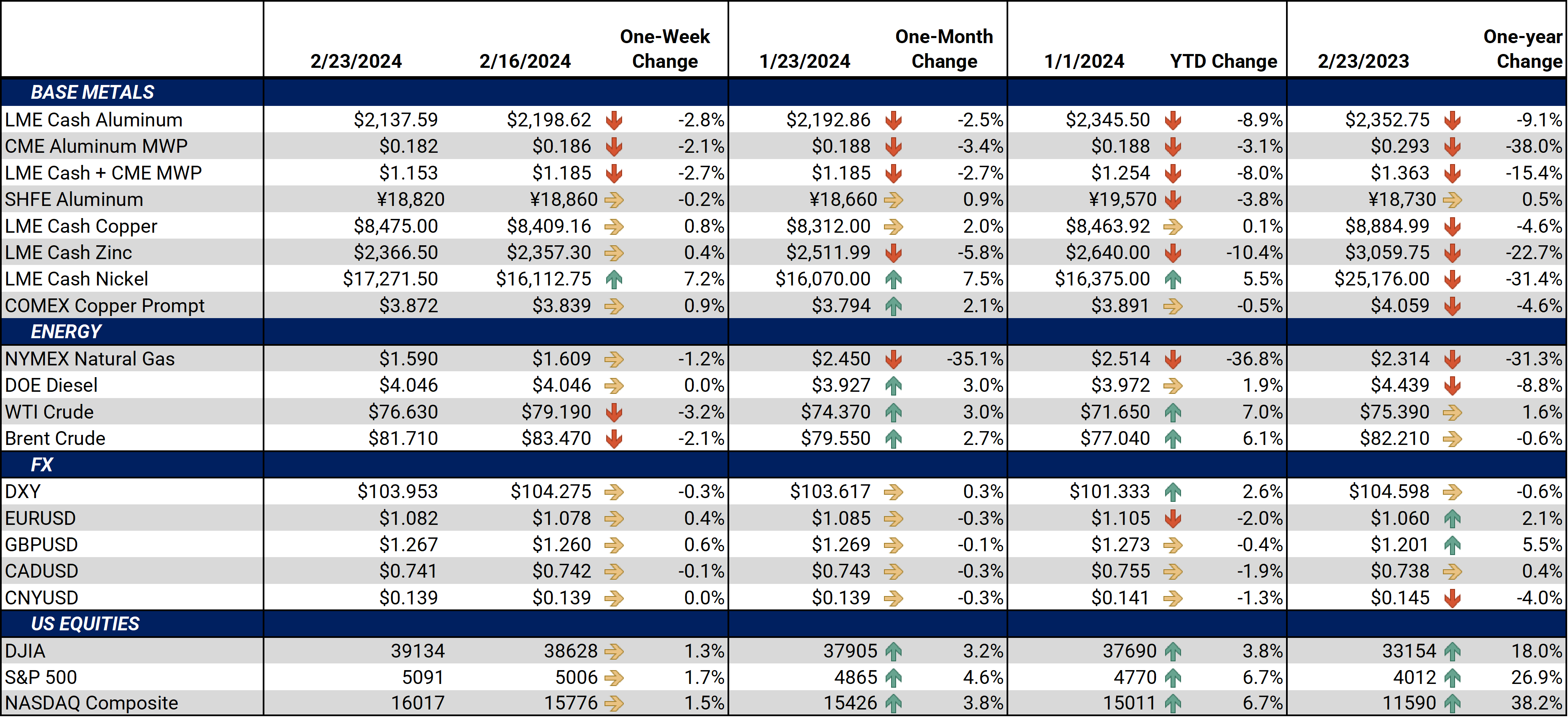

Aluminum LME aluminum prices were down on the week, while reports that the Biden administration could implement new sanctions against Russia took center stage. The new sanctions implemented early Friday seemed to target specific individuals and Russia’s financial, defense, and energy sectors, as opposed to Russian aluminum producers or exports. In any case, these will likely have little impact on the flow of Russian metal into the US. In late February 2023, the Biden administration imposed a 200% import tariff on Russian aluminum, effectively shutting out Russia from US markets. (Source: Bloomberg, White House) |

|

|

Norsk Hydro, one of Europe’s top aluminum producers, recently reiterated that high interest rates and poor construction demand will likely pressure aluminum demand. The company believes certain regions will see a 50% drop in construction and building demand year-over-year. Because of this, they predict that aluminum demand won’t recover until at least 2H2024. They believe that if interest rates stay high through 2H2024, aluminum demand won't recover this year. Norsk Hydro made these comments in an interview with the Financial Times on Monday. (Source: Bloomberg) Last year, China imported a record 1.175 million mt of Russian primary aluminum, up from approximately 462,000 mt in 2022. In 2023, about 76% of China’s primary aluminum imports came from Russia. Steep discounts, along with an improving import arbitrage, led to record volumes being shipped to China. (Sources: Bloomberg, Reuters, China Customs) |

|

Copper Some analysts remain skeptical about China’s construction sector. "Uncertainty about China's growth prospects, therefore, remains high and is a major negative factor for the base metals markets," Commerzbank stated in a note earlier this week. LME copper prices are down slightly in February despite the expectation that the Chinese construction season will boost copper demand. (Source: Bloomberg) Teck Resources, a Canadian miner, produced 103,400 mt of copper last quarter, up 58% from a year prior. Total production last year was 296,000 mt. This surge in production was mainly due to steady and increased output at three key mines in Canada, Peru, and Chile. For 2024, they estimate copper production will be between 465,000 to 540,000 mt. (Source: Teck Resources) Rio Tinto, one of the world’s largest copper miners, reported its annual net income fell by 19% in 2023 amid lower prices and higher operational costs. Last year, copper production costs were $1.95/lb, compared to $1.63/lb. For 2024, Rio estimates production costs to be $1.40 to $1.60/lb due to higher volumes at two production sites. (Source: Rio Tinto) |

|

Steel After trending sideways to lower for the better part of three months, American steel producers have finally started ramping up production. Last week, these steelmakers had a total output of 1.721 million st, the third consecutive week of increasing production. This was also the highest volume since early October. Steel profit margins have been relatively steady lately and currently hover near $530/st, based on AEGIS calculations. (Sources: AISI, CME) Cleveland Cliffs, one of America’s top steelmakers, will close its West Virginia-based tinplate plant, the company announced late last week. The US International Trade Commission recently struck down so-called dumping duties on steel can imports, much to the behest of domestic producers such as Cleveland Cliffs. According to Cleveland Cliffs’s CEO, the ITC ruling made “it impossible for us to viably produce tinplate.” Tinplate is tin-plated steel that is used to make food and beverage cans. (Source: Reuters) Prices for nickel, a key raw material for stainless steel production, have trended sideways for most of 2024. Investment funds, generally speculators in metals markets, have been net short LME nickel since late May 2023. This is the longest time they have been net short nickel since at least the pandemic in early 2020. Funds have been slowly adding to this position in early 2024, but contrary to normal price action, prices have been rangebound until recently. Unless these funds find a reason to do significant short covering, this position could remain a burden for LME nickel prices. (Source: LME) Finally, Kumba Iron Ore, a South Africa-based subsidiary of Anglo American, will soon go through a reconfiguration that will affect nearly 500 jobs, the company announced earlier this week. The restructuring is mainly due to supply and logistical issues that have impacted the company’s ability to export iron ore. As a whole, South Africa is one of the world’s top iron ore producers, with most exports going to China for steel production. (Source: Bloomberg) |

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

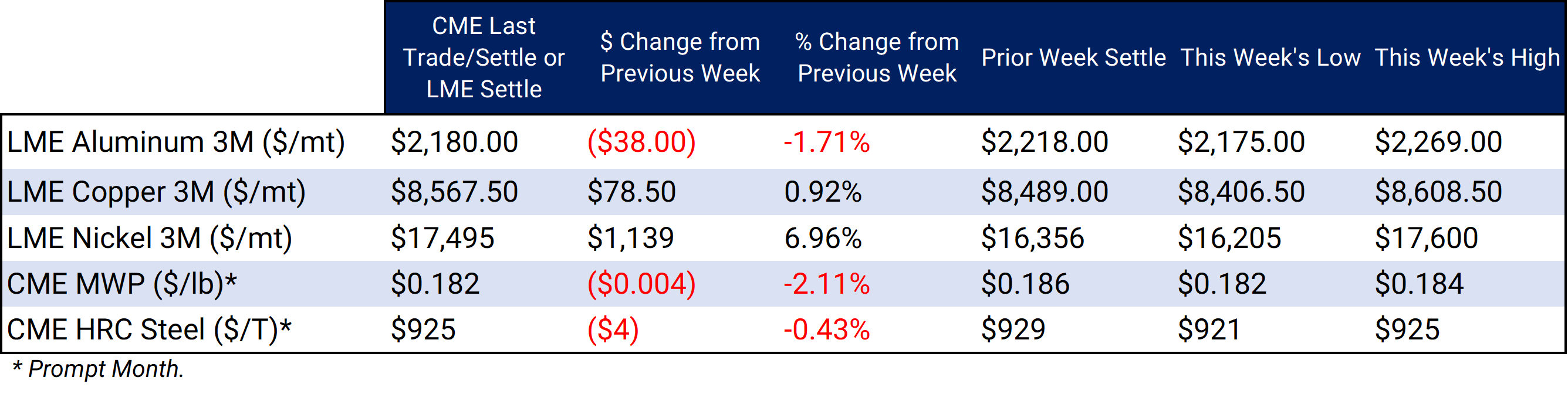

LME Aluminum 3M settled at $2,180/mt, down $38/mt on the week. Aluminum prices were down this week. Compared to last week, the futures forward curve has shifted vertically lower by approximately $40/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 18.2¢/lb this week. The CME Midwest Premium market is now in a contango from the February ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,567.5/mt, up $78.5/mt on the week. Compared to last Friday, LME Copper's forward curve has risen vertically by approximately $80/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $17,495/mt, up $1,139/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $1,100/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $925/T, down $4/T on the week. Steel mill profit margins improved dramatically throughout 3Q and 4Q2023 and are also starting 2024 on a good note. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $520/st, up from about $320/st on September 1. This is mainly due to prompt month CME HRC steel futures rallying alongside prices in the physical market. Since steel prices have increased significantly recently, mills should consider hedging production and raw material usage for 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

2/21/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 2/13/2024: Important US Economic Data (AEGIS Reference) 2/2/2024: China's Real Estate Woes Provide Opportunity for Copper Consumers 1/25/2024: Aluminum Starts 2024 On a Down Note, But Potential Supply Shocks Give Consumers a Reason to Hedge 1/4/2024: Year-End Review of LME Aluminum, Copper, CME HRC Steel and Hedging Implications for 2024 12/8/2023: Aluminum and Copper Markets Diverge but Hedging Opportunities Persist for End-Users |

|||||

Notable News |

|||||

|

2/22/2024: Funds amass record bear bets on zinc as LME stocks jump 2/22/2024: UK announces new Russia sanctions to mark Ukraine invasion anniversary 2/22/2024: Anglo American can mine Vale for revamp ideas 2/22/2024: Anglo American to review assets after writedowns and profit plunge 2/22/2024: Metallurgical coal is the commodity world's quiet performer |

|||||