|

Aluminum US Senator Josh Hawley introduced a bill on Wednesday that, if passed, would raise the import tariff on Chinese EVs to 125%, up from 27.5% currently. The bill would also increase the tariff on EVs produced in Mexico by Chinese companies to 100%, up from 2.5% currently. This move aims to protect domestic EV manufacturers against cheaper, foreign-produced EVs, potentially shutting imports out of the US market. This would also likely dramatically affect aluminum demand in China and North America. China’s EV sector is a major source of aluminum demand and a key growth industry for aluminum usage. As for North America, several Chinese EV producers have plans to build factories in Mexico but could decide against doing so if they face onerous tariffs. (Source: Reuters) |

|

|

Investment funds, generally speculators in metals markets, have become quite bearish on aluminum in recent weeks. As of last Friday, these funds are net short over 20,800 contracts, their largest short position so far this year. From the February 2 close through last Friday, they sold nearly 15,700 contracts, contributing to the nearly 2.3% drop in prices during that period. (Sources: LME) China’s aluminum demand will grow at a slower pace this year compared to 2023, Chinese researcher Antaike said in a note earlier this week. This slump in growth is mainly due to continually depressed real estate and construction sectors, the researcher clarified. Renewable energy remains a growth sector, specifically for electric vehicles, solar panels, and lithium batteries. (Source: Bloomberg) China’s prices for alumina, the key raw material from which aluminum is produced, surged late last week after bauxite miners in Guinea announced a strike for this week. According to Jinrui Futures Co, China only has about half to one month’s bauxite supply on hand. “Chinese alumina production could be further constrained if Guinea bauxite mining is affected to an extended period,” the brokerage proclaimed. Guinea is the world’s second-largest bauxite producer and is China’s top supplier of the key raw material that is used to produce alumina (Sources: Bloomberg, USGS, China Customs) Continuing on alumina, Alcoa has made a $2 billion bid to buyout Alumina Ltd, an Australian joint-venture arm of Alcoa, the company announced earlier this week. This move would help consolidate and streamline Alcoa’s Australian operations and would “enhance Alcoa’s position as of one of the world’s largest bauxite and alumina producers,” according to Alcoa’s press release. Alcoa has recently experienced issues with its Australian alumina operations, including the closure of the Kwinana alumina plant as part of a cost-cutting measure. (Sources: Bloomberg, Alcoa) |

|

Copper Unlike aluminum, investment funds have been buying LME copper, which has helped push prices higher. As of last Friday, these funds are net long 22,100 contracts, having bought over 11,500 contracts (net) over the past two weeks. This is their largest net long position since mid-December. Investment funds are likely getting bullish due to China’s upcoming construction season as well as perceived shortages of refined copper in China. (Source: LME) Due to the low availability of feedstock, treatment charges in China, which are the fees miners pay to have their raw copper processed into refined metal, have fallen to the lowest level since at least 2013. This drop in fees has dramatically reduced profit margins for many smelters while others are essentially breaking even. Plummeting fees, along with little available feedstock, fund buying, and improving spot demand, have led to higher LME prices. (Source: Bloomberg) Vale, a top copper miner, was told by the Brazilian government to suspend operations at two mining sites due to non-compliance and other environmental licensing issues. One operation, known as Sossego, is Vale’s second-largest copper mine, producing 66,800 mt last year. Vale will work as fast as possible to achieve compliance, according to a statement from last Thursday. (Source: Bloomberg) Jubilee Metals Group, a diversified mining company with assets across southern Africa, is in the process of buying a shuttered Zambian copper-cobalt refinery from Eurasian Resources Group (ERG), according to Zambia’s mining ministry. ERG closed the plant in 2020 due to a lack of feedstock. The refinery, which is situated near the border with the Democratic Republic of the Congo (DRC), has a production capacity of 55,000 mt/yr for copper and 6,000 mt/year of cobalt. The DRC and Zambia are Africa’s top producers of copper and cobalt. (Source: Bloomberg) Vedanta Ltd, an Indian metals producer, will not be able to reopen its shuttered copper smelter due to a Supreme Court ruling. Earlier this week, India’s Supreme Court ruled that the smelter must stay closed due to environmental concerns. The 400,000 mt/year smelter was closed in 2018 due to pollution concerns, forcing the country to rely mainly on imports. Due to urbanization and infrastructure projects, copper imports are expected to increase over the coming years. (Source: Bloomberg) |

|

Steel CME HRC Steel prices continue to fall in early 2024. The prompt month (March ‘24) contract currently hovers near the lowest prices since early October. Similarly, the CME HRC Steel futures forward curve for April ’24 onwards is in contango, meaning that futures prices are higher than spot. The fall in prompt months and a contango futures market suggest the market is amply supplied. As for demand, sources are telling AEGIS that end-user demand remains subdued. (Source: CME) The Biden administration will closely scrutinize Nippon Steel’s ties to China while reviewing the company’s potential merger with US Steel, according to reports from late last week. One worrisome factor for the merger is that the merger could lead to higher imports of Chinese-produced steel. The US currently imports a minimal amount of steel from China, though, and any steel imports from China are subject to the 25% Section 232 tariffs. (Source: Bloomberg) The United Steelworkers (USW) union has signed a nondisclosure agreement with Nippon Steel, even though the union still opposes Nippon’s potential buyout of US Steel. The USW cannot block Nippon’s acquisition of US Steel, but the union can influence lawmakers who might seek to block the merger. The merger will be subject to a lengthy review by US officials due to national security, job preservation, and antidumping. (Source: Bloomberg) Ukraine struck Russia’s largest steel mill over the weekend, coinciding with the two-year anniversary of the Russian invasion. The steel produced in this mill is used to manufacture Russia’s armaments, including missiles, drones, and artillery. The mill is responsible for approximately 18% of Russia’s annual steel production. (Source: Reuters) Finally, at the behest of other major nickel producers, Indonesia will keep pumping out nickel exports despite the recent price slump, government officials reiterated this week. “The purpose for the government is to find an equilibrium so that nickel demand, especially for EVs, is well supplied,” Indonesian officials declared. Indonesia is the world’s nickel producer and exporter, with most exports going to China in the form of stainless steel or refined nickel. Prices for nickel, a key raw material for stainless steel production, fell by 45% last year due to ample global supply amid subdued demand. LME prices have recovered slightly in 2024, up roughly 5% as of this writing. (Source: LME, Bloomberg) |

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

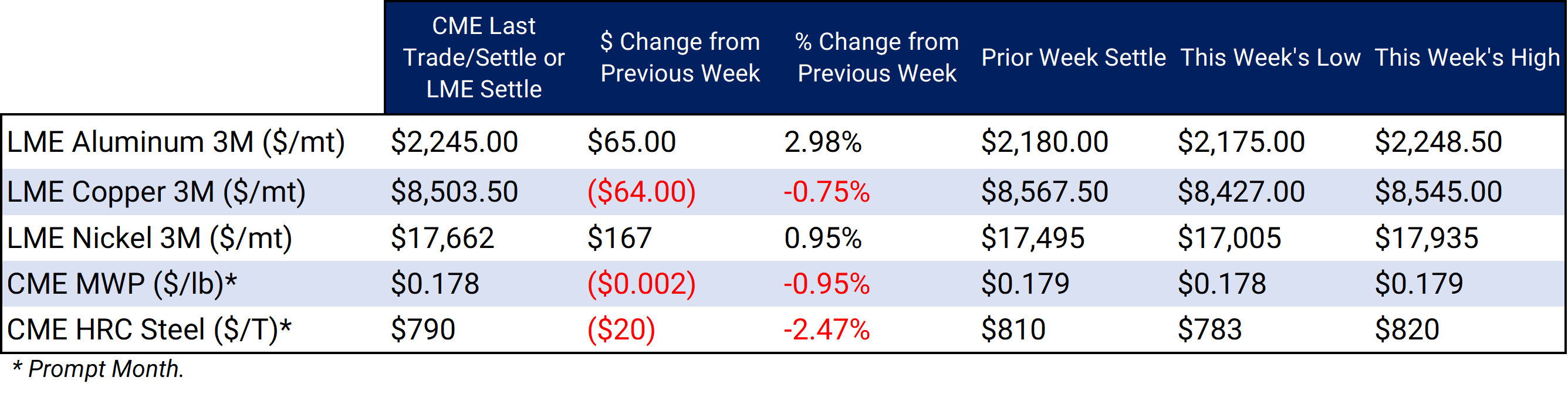

LME Aluminum 3M settled at $2,245/mt, up $65/mt on the week. Aluminum prices were up this week. Compared to last week, the futures forward curve has shifted vertically higher by approximately $65/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 17.8¢/lb this week. The CME Midwest Premium market is now in a contango from the March ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,503.5/mt, down $64/mt on the week. Compared to last Friday, LME Copper's forward curve has fallen vertically by approximately $65/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $17,662/mt, up $167/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $170/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $925/T, down $4/T on the week. Steel mill profit margins improved dramatically throughout 3Q and 4Q2023 and are also starting 2024 on a good note. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $400/st, up from about $320/st on September 1. This is mainly due to prompt month CME HRC steel futures rallying alongside prices in the physical market. Since steel prices have increased significantly recently, mills should consider hedging production and raw material usage for 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

2/28/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 2/27/2024: Aluminum Consumers Should Still Implement Hedges, Even Though Russia Sanctions Mean Little 2/13/2024: Important US Economic Data (AEGIS Reference) 2/2/2024: China's Real Estate Woes Provide Opportunity for Copper Consumers 1/25/2024: Aluminum Starts 2024 On a Down Note, But Potential Supply Shocks Give Consumers a Reason to Hedge 1/4/2024: Year-End Review of LME Aluminum, Copper, CME HRC Steel and Hedging Implications for 2024 |

|||||

Notable News |

|||||

|

3/1/2024: China's parliament to unveil more stimulus next week, bold reforms unlikely 3/1/2024: Top Codelco execs see debt growing as production recovers 3/1/2024: Thyssenkrupp workers want pledges on investment, jobs ahead of steel business revamp 2/29/2024: Adani's $1.2 billion copper smelter to import concentrates from Peru, Chile, Australia 2/28/2024: Republican US senator wants to hike tariffs on Chinese vehicles 2/28/2024: Thyssenkrupp dismisses report about potential job, capacity cuts 2/24/2024: Ukraine says it struck big Russian steel plant on invasion anniversary 2/23/2024: US should block cheap Chinese auto imports from Mexico, US makers say |

|||||