|

Aluminum Aluminum prices stalled this week while Chinese economic data continues to disappoint. Last Friday, a key gauge of Chinese factory activity showed the sector has contracted for five consecutive months (through February). According to data from Shanghai Metal Market, China’s aluminum inventories are at the highest level since last May, suggesting that demand remains muted post-Lunar New Year. (Source: Bloomberg) |

|

|

The CME Midwest Premium (MWP) could rally this year if shipping rates continue to increase due to the Red Sea conflict, according to a Bloomberg analysis. This premium, which incorporates shipping rates, tariffs, and other variables, has fallen this year because of subpar US demand. AEGIS does caution that demand remains a burden, and the UAE-Israel road corridor has become an alternative shipping route for the region. (Source: Bloomberg) Emirates Global Aluminum (EGA), which produced a record amount of aluminum last year, will expand production via recycling, the company announced earlier this week. They also downplayed the shipping crisis in the Red Sea, stating they have alternative routes and a diverse group of customers. Even though weak demand has pressured prices and profitability, EGA remains optimistic that demand will grow, justifying their expansion efforts. (Source: Bloomberg) Rusal exported a total of 458,000 mt of primary aluminum in January & February, up 14.6% compared to last year, according to information from Russian Railways, which was later reviewed by Interfax. Domestic shipments also rose by 12% to 117,000 mt. The Russia-Ukraine conflict has been a boon for Russia’s domestic aluminum demand. Exports have also increased due to steep discounts and improving import arbitrage for its top buyer, China. (Source: Bloomberg) Aluminum of Greece, the country’s only aluminum primary smelter and a key producer of recycled aluminum, produced 239,000 mt (183,000 mt primary, 56,000 recycled) last year, up 1% compared to 2022. This slight uptick in production comes despite volatile prices and weak manufacturing sectors across Europe. Late last week, Aluminum of Greece's parent company, Mytilineos, reiterated that energy costs remain a top concern, as electricity represents nearly 40% of the production cost for primary aluminum. They also stated the EU’s upcoming carbon tax scheme will be a burden for the industry. (Source: S&P Global) |

|

Copper Copper prices initially reacted little to China’s new infrastructure plan, out Tuesday. The government will issue 1 trillion yuan in new bonds for infrastructure projects, according to the report. They cautioned that real estate-related debt remains a problem, especially for local governments that might not be able to handle the issue. (Source: CNBC) Canadian copper miners cannot rely on Chinese investments, Canada’s natural resources minister stated earlier this week. Even though Canada implemented stricter rules in 2022 to discourage Chinese investment, several major transactions have been announced since then. In January 2024, China’s Zijin Mining Group Co announced it planned to buy a 15% stake in Solaris Resources, a Vancouver-based copper producer. Although transactions such as this are controversial, production growth will likely come from investments such as these. (Source: Bloomberg) To shore up public support with the goal of restarting the mine, First Quantum Minerals has opened its recently shuttered Panamanian copper mine to public visitors. On Thursday, the government requested that First Quantum end tours, but its unclear if the company has or will do so. Late last year, the company’s Cobre Panama copper mine was ordered closed by the Panamanian government due to environmental concerns. “We had a mine that worked for the people of Panama, so I’m confident that we will find a solution,” First Quantum’s Chairman recently proclaimed. Although the chances of reopening the mine are slim, doing so would add significant supply to the market. At one point, the Cobre Panama mine was responsible for about 1.5% of global copper mine production. (Source: Bloomberg) India’s Kutch Copper Ltd, a subsidiary of Adani Resources, will source copper concentrate from Chile, Peru, and Australia when operations start in a few weeks, the company stated last week. The facility will be the world’s largest copper smelter, with an initial annual capacity of 500,000 mt/year. Adani plans to double the smelter’s capacity by 2028 or 2029. India has recently become one of the world’s largest copper consumers and aims to reduce its dependency on imports of copper. (Source: Reuters) Codelco, Chile’s state-owned copper miner and the world’s largest producer, will continue to add debt to fuel its expansion goals, company executives proclaimed last week. At the end of 2023, Codelco was $20.4 billion in debt and added $2 billion in January. By 2027, this debt pile could increase to $31.5 billion, according to company estimates. Codelco expects 2024 to reach 1.35 million mt, up from 1.325 million last year, with output ultimately reaching 1.7 million mt by 2030. Although executives downplayed the company’s reliance on debt, this growing debt pile makes Codelco more susceptible to unforeseen costs and falling prices. (Source: Reuters) |

|

Steel Nippon Steel will meet with the United Steelworkers (USW) union later this month to gain support for the company’s potential buyout. The USW cannot block the merger, but it may sway lawmakers who would have otherwise blocked the deal. The merger will be heavily scrutinized by US lawmakers, citing national security and other issues. (Source: Reuters) Like aluminum, some analysts are cautious about China’s demand for iron ore. In a note late last week, Chinese researcher Mysteel stated, “The fundamentals of the steel market should gradually improve during March as demand gradually returns. The short term is not pessimistic, and the future is cautiously optimistic.” A meeting this week of key Chinese political figures will be closely watched for any cues or stimulus that could help the country’s sagging real estate sector and, therefore, impact metals demand. (Source: Bloomberg) Chinese steel mill profit margins have slowly increased this year while iron ore prices have fallen. Currently, profit margins hover near $45/mt, up from the 2023 average of $41/mt. These improving profit margins may lead to increased steel production, even though real estate demand remains muted. (Source: Bloomberg) Thyssenkrupp, one of the EU’s top steel producers, has rebuked claims by a German newspaper the company’s restructuring will cost jobs and significantly reduce steel output. German newspaper Handelsblatt recently reported that Thyssenkrupp’s steel business will cut 5,000 jobs and reduce production capacity from 11.5 million mt/year to between 8 and 9 million mt. Thyssenkrupp denied all the allegations, saying that Handelsblatt’s speculation was “highly dubious.” (Source: Reuters) Prices for nickel, a key raw material for stainless steel production, have rallied in recent weeks while investment funds cover their large short position. From the February 9 close through last Friday, investment funds, generally speculators in metals markets, have purchased approximately 14,300 (net) contracts, bringing their net short position to 10,320 contracts. These investment funds can have an oversized influence on metals prices, which is partially why LME nickel prices rallied over 11% during that period. (Source: LME) |

|

|

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

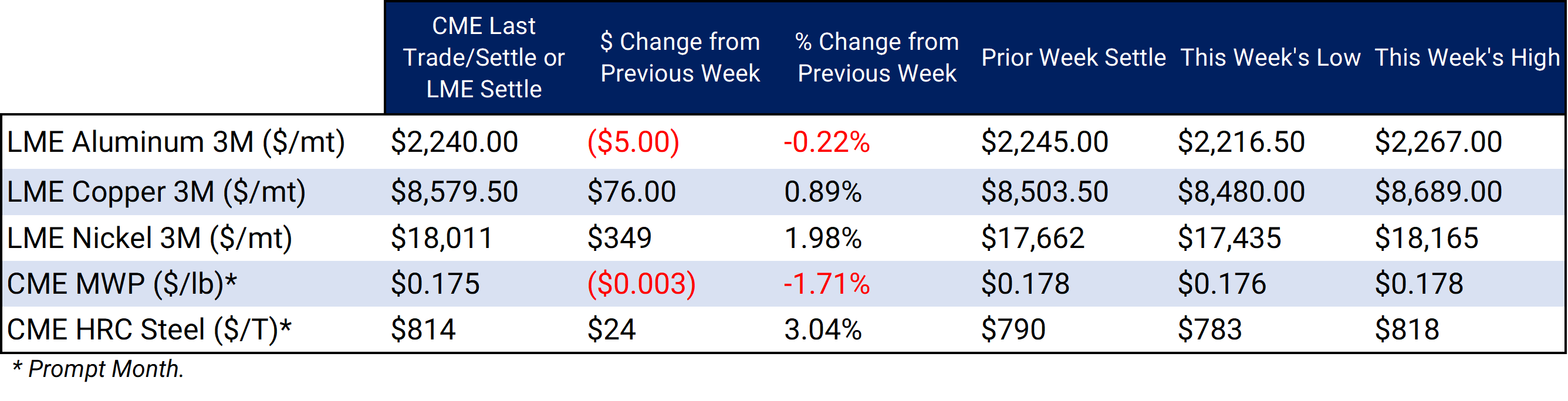

LME Aluminum 3M settled at $2,240/mt, down $5/mt on the week. Aluminum prices were down this week. Compared to last week, the futures forward curve has shifted vertically lower by approximately $5/mt. It remains in a steep contango, meaning nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. Depending on risk tolerance, end-users might consider strategies that use only swaps or options or a combination of both. The aluminum market has sufficient liquidity to use swaps and options. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

Midwest Premium |

|||||

|

Prompt month CME MWP last traded/settled at 17.5¢/lb this week. The CME Midwest Premium market is now in a contango from the March ‘24 contract on forward. The CME Midwest Premium swap market is thinly traded, with no options market. Hedging in this thinly traded market is challenging, so we recommend using limit orders. Please get in touch with AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,579.5/mt, up $76/mt on the week. Compared to last Friday, LME Copper's forward curve has risen vertically by approximately $75/mt and remains in contango throughout 2024 and 2025. The copper market has sufficient liquidity to use swaps and options. Depending on their risk tolerance, consumers might consider strategies that use only swaps, options, or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $18,011/mt, up $349/mt on the week. As prices were up this week, nickel’s forward curve has also shifted vertically higher by about $350/mt. It remains in a steep contango, meaning that nearby prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Depending upon your risk tolerance, consumers might consider strategies that use only swaps or options or a combination of both. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last traded/settled at $814/T, up $24/T on the week. Steel mill profit margins improved dramatically throughout 3Q and 4Q2023 and are also starting 2024 on a good note. The CME HRC Steel – CME MW Busheling Fe Scrap spread, which is generally used as a gauge for steel mill profitability, is now approximately $420/st, up from about $320/st on September 1. This is mainly due to prompt month CME HRC steel futures rallying alongside prices in the physical market. Since steel prices have increased significantly recently, mills should consider hedging production and raw material usage for 2024. For most steel producers, this would consist of buying CME MW Busheling Scrap swaps and selling CME HRC swaps. Options are available for CME HRC, but they are relatively illiquid. Please get in touch with AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

3/6/2024: AEGIS Factor Matrices: Most important variables affecting metals prices 2/27/2024: Aluminum Consumers Should Still Implement Hedges, Even Though Russia Sanctions Mean Little 2/13/2024: Important US Economic Data (AEGIS Reference) 2/2/2024: China's Real Estate Woes Provide Opportunity for Copper Consumers 1/25/2024: Aluminum Starts 2024 On a Down Note, But Potential Supply Shocks Give Consumers a Reason to Hedge 1/4/2024: Year-End Review of LME Aluminum, Copper, CME HRC Steel and Hedging Implications for 2024 |

|||||

Notable News |

|||||

|

3/7/2024: Panama asks First Quantum to suspend visitor program at disputed copper mine 3/6/2024: US imposes preliminary duties on aluminum extrusions from China, Indonesia, Mexico, Turkey 3/5/2024: Nippon Steel exec to meet USW head to seek support for U.S. Steel deal 3/5/2024: Future of First Quantum mine is for the people of Panama to decide, US official says 3/4/2024: China's Huayou Cobalt chief proposes battery material policy to tackle overcapacity 3/3/2024: China breaks with tradition at annual ‘Two Sessions’ meeting by scrapping premier’s press conference |

|||||