|

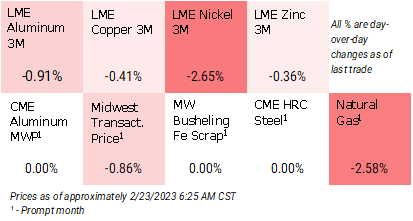

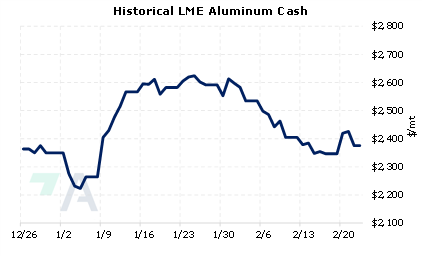

Some Wall Street analysts continue to express bullish aluminum price forecasts. AEGIS agrees that there is an upside risk not only to LME aluminum prices but also to the CME MWP. Citing the possibility of sanctions on Russian aluminum and Chinese production issues, "upside risks abound" for global aluminum prices, according to Citigroup. Citigroup believes that aluminum prices could hit $2,700/mt this year; however, could rally to $3,000/mt if these issues worsen. The last trade on the LME 3M Select was $2,405/mt, thus prices need to rally approximately $300/mt, to match Citigroup’s low-end price target (7:00 AM CST). (Source: Bloomberg) |

|

|

|

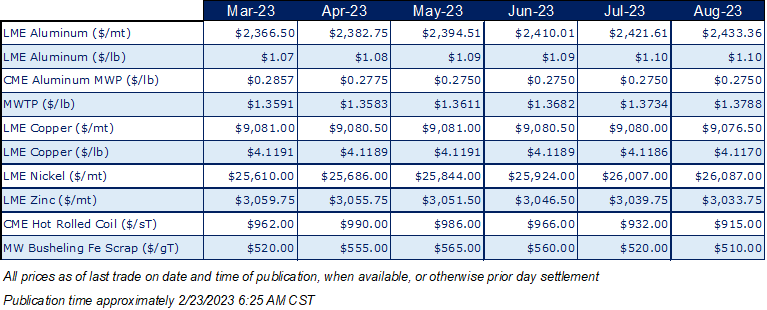

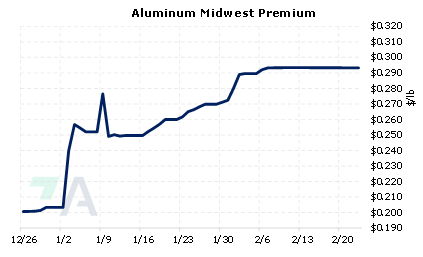

The possibility of sanctioning Russian aluminum has been a hot-button issue in recent months. AEGIS believes that the Biden Administration’s recently proposed 200% tariff on imports of Russian aluminum if implemented, is essentially a sanction as it would effectively shut off our imports of Russian aluminum. As for market impact, such a tariff is likely to be bullish to the aluminum Midwest Premium (MWP). Currently, approximately 3% of aluminum imports come from Russia; however, those that buy Russian aluminum would need to fill the void by buying from other global suppliers. As our importers compete for the same cargoes as other major importers, the MWP would likely need to rise to entice cargoes that would otherwise go to Europe or elsewhere. Please contact us for further thoughts on the Russian tariff/sanction situation and implications for the MWP. The competition for cargoes has already started. For example, shortages of high-purity aluminum in Europe led to a nearly 19%, or $48/mt, rise in European import premiums. However, to entice cargoes away from Europe, the MWP has rallied over 44%, or $198/mt. As we suggested above, the MWP could rally further if Russian supplies into the US evaporate. However, American aluminum end-users can mitigate this price risk by hedging with CME MWP swaps. The forward curve is now backwardated through May 2023, but then largely goes flat beyond that contract. This means that end-users can hedge future usage at a discount to spot prices. Please note that there is no options market for the CME MWP. The CME Midwest Premium swap market is thinly traded, thus, we recommend using limit orders, as doing so would allow you to control how much you would pay. For example, if you were trying to buy the MWP at 30 cents, by using a limit order, you are attempting to lock in a price of 30 cents or better. Please contact AEGIS for specific strategies that fit your operations. (2/23/2022) |

||

|

|

||

Note: Clients with AEGIS Platform access can see this and other research, plus hedge portfolio reporting and tools here. |

||

|

|

||

Price Indications |

||

|

|

||

|

|

||

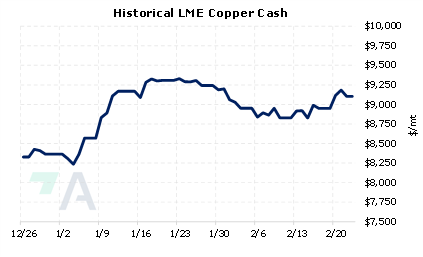

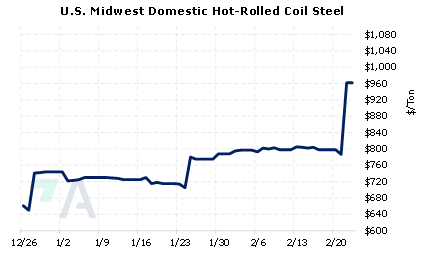

Today's Charts |

||

|

|

|

|

|

|

AEGIS Insights |

||

|

02/22/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 02/07/2023: Will Aluminum's Rally Continue? 01/24/2023: Peruvian Protests Could Support Copper Prices 01/11/2023: Nickel Prices Could Remain Volatile Into 2023 |

||

|

|

||

| Important Headlines | ||

|

2/22/2023: Rio Tinto slashes dividend as profit plunges on slower China demand 2/21/2023: US HRC: Prices jump as mills again hike prices 2/21/2023: BHP Group says reform to LME nickel contract 'long overdue' |

||

|

|

||

|

Important Disclosure: Indicative prices are provided for information purposes only, and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee to the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as “edge,” “advantage,” “opportunity,” “believe” or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.

|

||