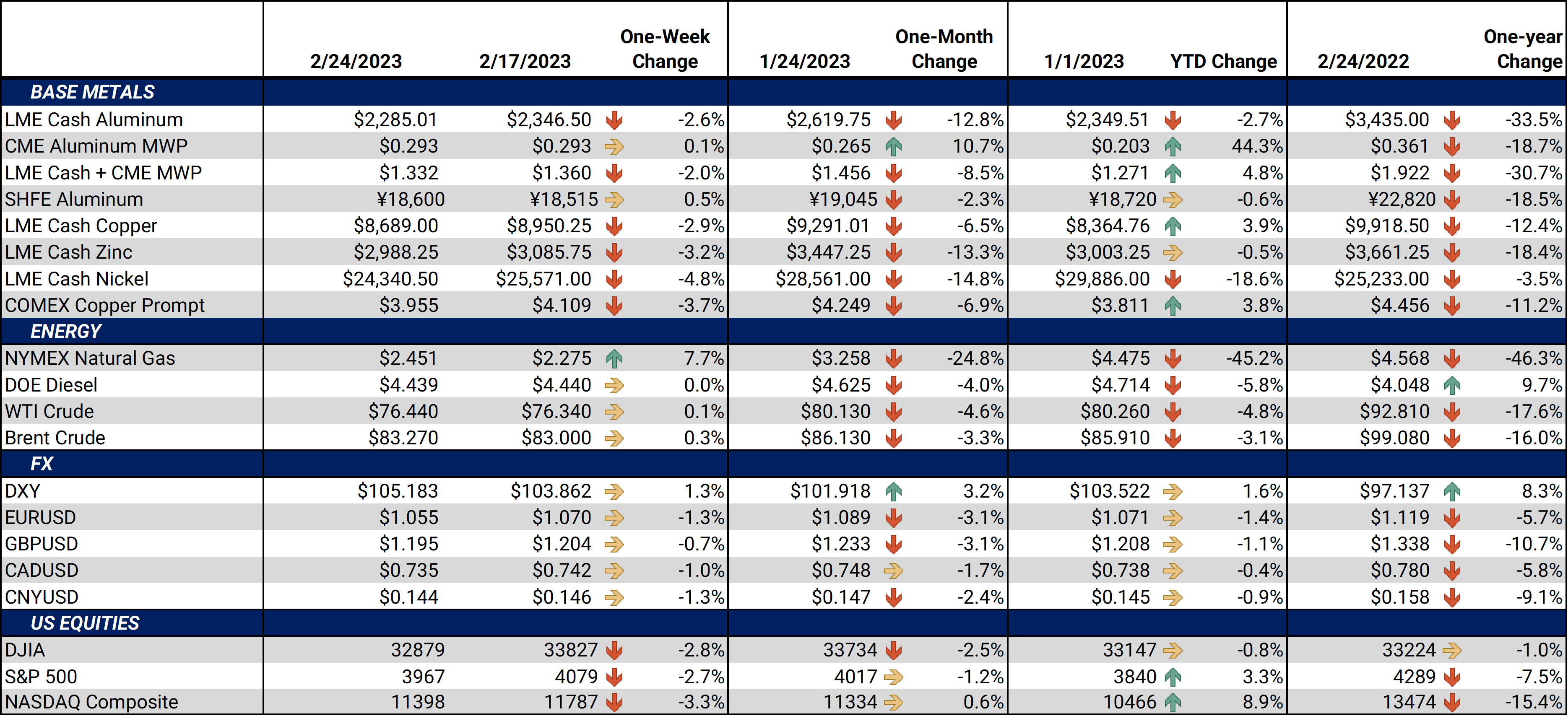

|

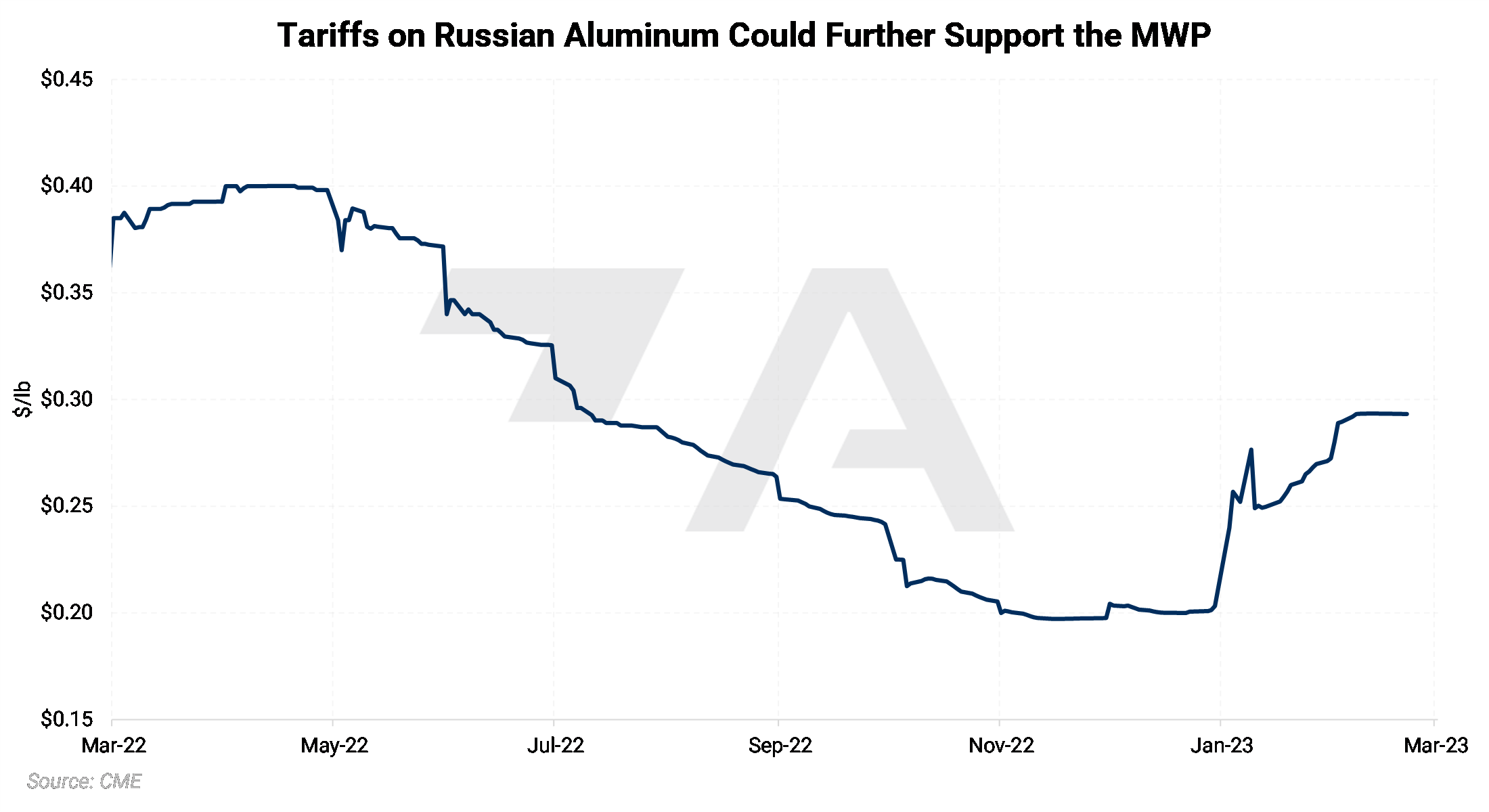

Aluminum On Friday morning, the White House announced it will increase tariffs on imports of Russian aluminum to 200%, up from the current level of 35%. AEGIS believes this could provide a bullish price risk to the aluminum Midwest Premium (MWP) market; however, this price risk exposure can be mitigated via CME MWP swaps. This bullish price risk exists mainly because this tariff could effectively shut off our imports of Russian aluminum. Moreover, those that buy Russian aluminum would need to fill the void by buying from other global suppliers. As US buyers compete for the same cargoes as other major importers, the MWP would likely need to rise to entice cargoes that would otherwise go to Europe or elsewhere. Please contact us for further thoughts on the Russian tariff/sanction situation and implications for the MWP. |

|

|

|

According to Bloomberg, this “tariff on Russian aluminum will take effect [on] March 10, and aluminum products which are manufactured using any amount of aluminum cast or smelted in Russia will be affected from April 10.” This announcement comes on the one-year anniversary of the start of the Russia-Ukraine conflict. Based on USGS data, approximately 3% of U annual aluminum imports currently come from Russia. However, as we stated above, this new tariff could drop import volumes to zero. (Sources: Bloomberg, Reuters, White House, USGS) |

|

|

|

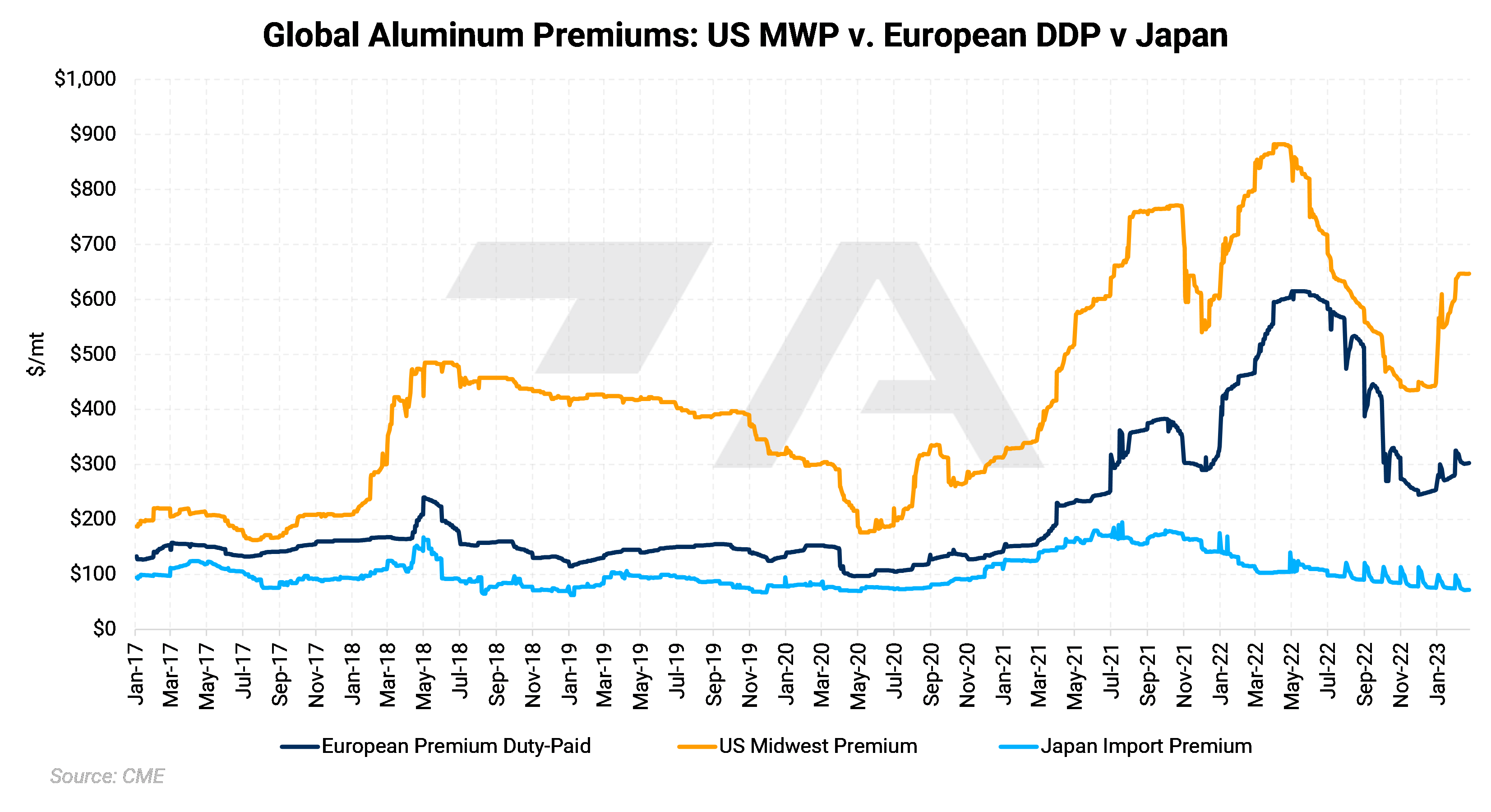

The competition for aluminum cargoes has already started. For example, shortages of high-purity aluminum in Europe led to a nearly 19%, or $49/mt, rise in European import premiums since January 1. However, to entice cargoes away from Europe, the MWP has rallied over 44%, or $198/mt since January 1. As we suggested above, the MWP could rally further if Russian supplies into the US evaporate. |

|

|

|

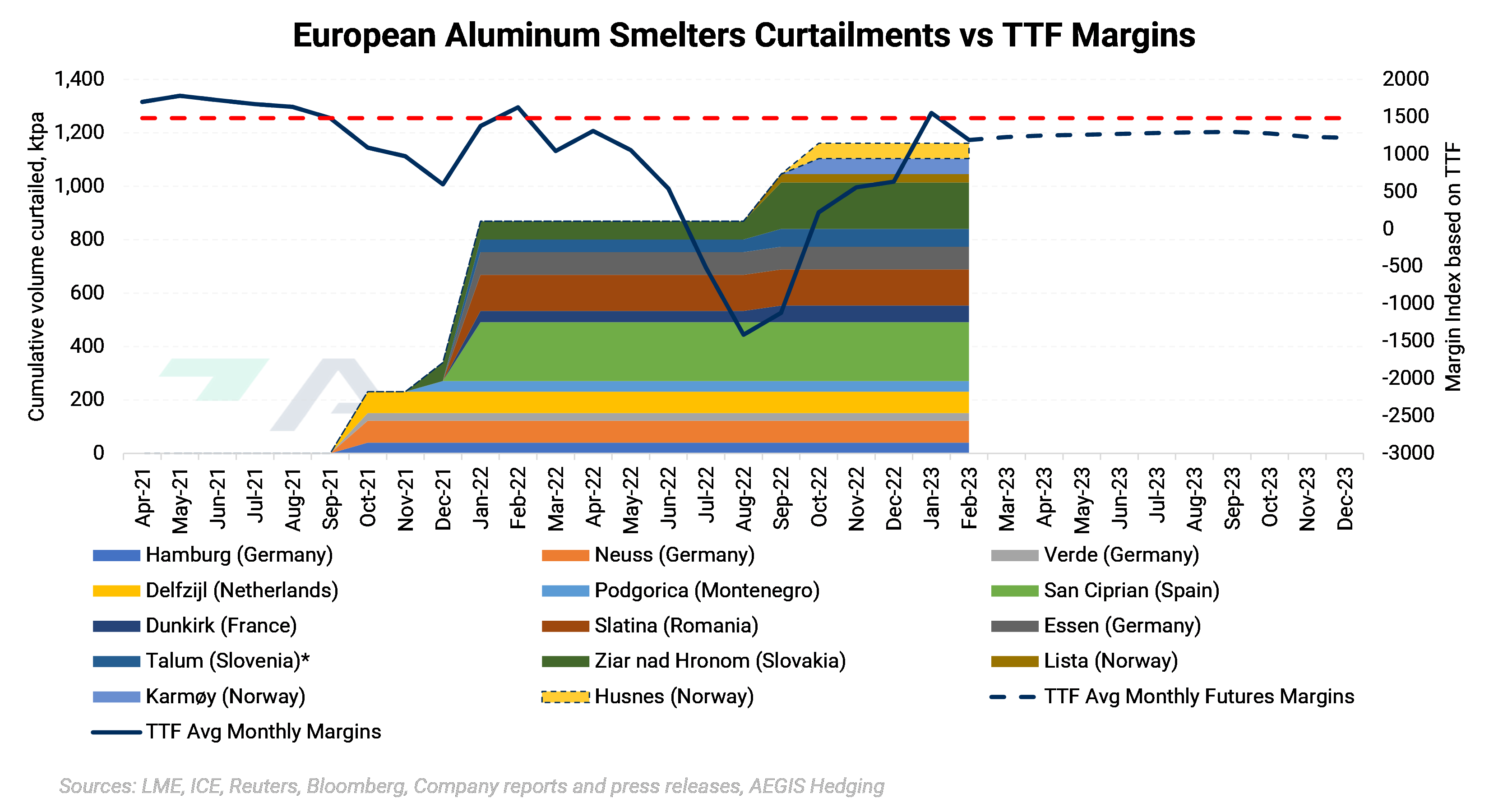

Aluminum prices could rally in 2023, as a nearly 80% drop in electricity and natural gas prices across Western Europe still isn’t enough to incentivize previously curtailed aluminum smelters to severely ramp up production, according to BloombergNEF. Based their analysis, BloombergNEF’s average aluminum price target for this year is $2,490/mt. AEGIS also notes that this price target is only approximately $100/mt away from the current $2,389/mt average price for 2023 LME aluminum futures (2/24/23 close). According to AEGIS’s European aluminum smelter margin calculator, using the TTF prompt price and the TTF futures curve, LME aluminum cash and LME alumina prompt, European smelter margins have turned profitable; however, not profitable enough to entice smelters to restart curtailed production. Therefore, AEGIS believes that either TTF prices need to fall further, or aluminum prices need to rise to entice European smelters to restart production. For example, smelters started shutting off or making curtailments announcements when our model showed profits margins at approximately $1,485/mt. Based on the TTF futures curve, the profit margins are about $1,300/mt from March 2023 through the remainder of the year. Therefore, aluminum prices need to rise at least $185/mt before we could (or will likely see) smelters come back online. (Please note that our margin calculator is for demonstration purposes only and does not factor in every cost that an aluminum smelter might incur). |

|||||

|

|

|||||

|

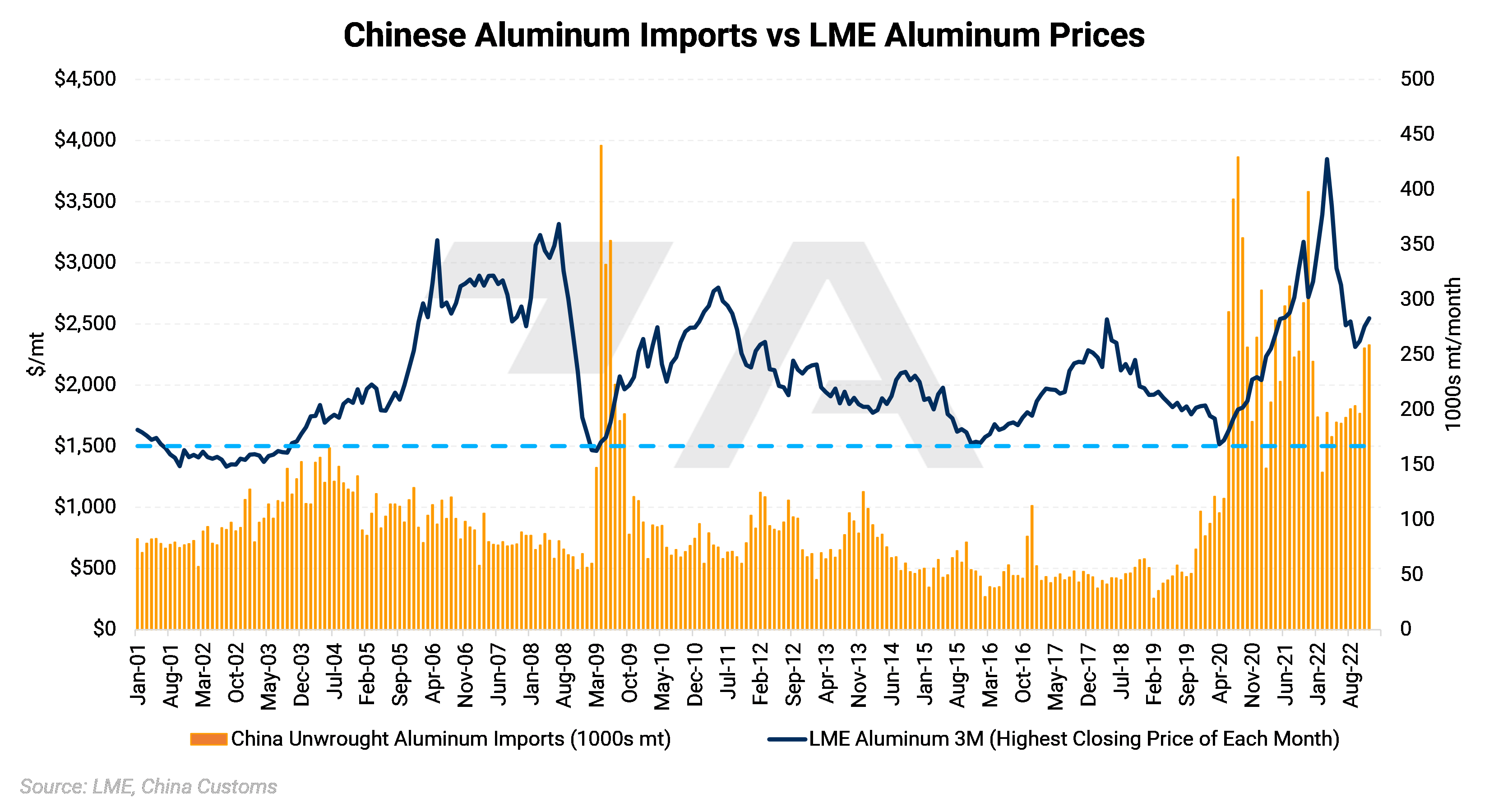

European supply issues are only a small part of the puzzle. AEGIS believes we should look to Chinese demand and supply for cues on global prices. Aluminum prices could rally this year if Chinese supply dwindles even further, forcing Chinese buyers to further tap into global supplies. Yunnan province, which is one of China’s main aluminum production regions, has ordered its aluminum smelters to curtail 415,000 mt of annual capacity due to low hydropower generation, according to Bloomberg. Jack Shang from Citigroup believes this curtailment could last through 1H2023, as the region remains plagued with production and electricity supply issues. This latest round of production cuts adds to the nearly one million mt of cuts last fall, thereby bringing total curtailments to approximately 1.4 million mt of annual capacity. At 5.3 million mt, Yunnan Province is responsible for about 12% of China’s aluminum production. According to Bloomberg, both steady demand and unreliable power issues in key production areas such as Yunnan province have led to increasing Chinese aluminum imports during the pandemic era. AEGIS notes that Chinese aluminum imports have risen alongside global prices. Relative to history, this is quite unusual, as normally their imports rise when global prices are low. For example, as you can see on the chart below, imports tend to increase when LME prices are near $1,500/mt (as noted by the blue dashed line). Furthermore, Chinese aluminum end-users could be forced to continue importing, if more domestic supply goes offline. |

|||||

|

|

|||||

|

Finally, some Wall Street analysts continue to express bullish aluminum price forecasts. AEGIS agrees that there is an upside risk not only to LME aluminum prices but also to the CME MWP. Citing the possibility of sanctions on Russian aluminum and Chinese production issues, "upside risks abound" for global aluminum prices, according to Citigroup. Citigroup believes that aluminum prices could hit $2,700/mt this year; however, could rally to $3,000/mt if these issues worsen. The last trade on the LME 3M Select was $2,342/mt, thus prices need to rally approximately $360/mt, to match Citigroup’s low-end price target (2/24/2023 close). (Source: Bloomberg) |

|||||

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

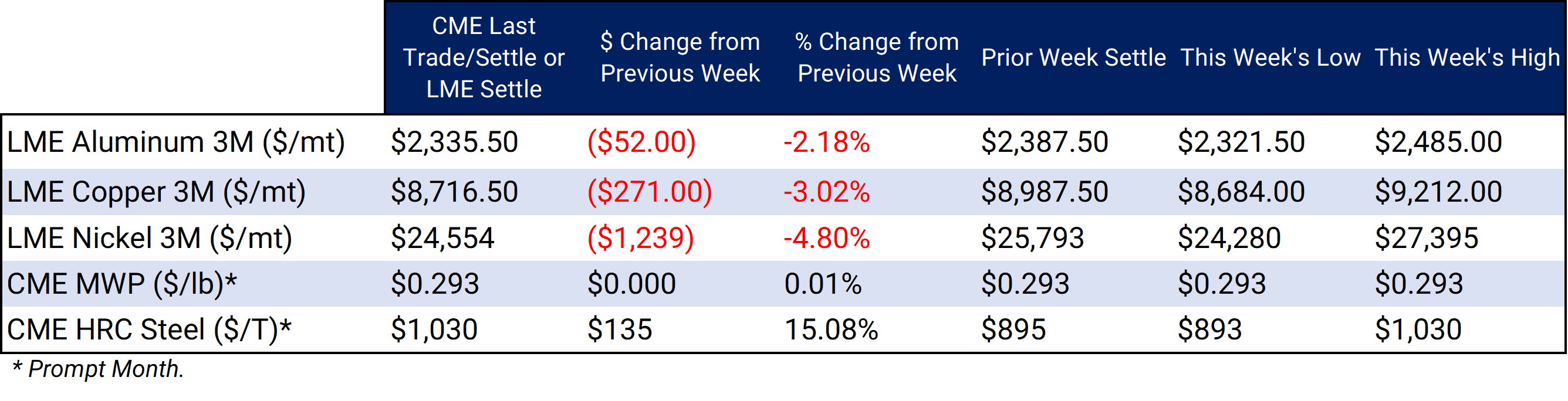

LME Aluminum 3M settled at $2,335.50/mt, down $52/mt on the week. Aluminum prices were down this week. This has caused the forward curve to shift vertically lower by approximately $50/mt. It remains in contango, meaning that nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. End-users might consider strategies that use only swaps or options or a combination of both, depending on risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 29.3¢/lb this week. The CME Midwest Premium market is backwardated through May 2023 but then becomes largely flat for the remainder of this year. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,716.50/mt, down $271/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted lower by about $270/mt. The forward curve is now relatively flat throughout 2023 but becomes backwardated in 2024 and beyond. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon their risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $24,554/mt, down $1,239/mt on the week. As prices were down this week, nickel’s forward curve has also shifted vertically lower, by about $1,200/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last settled at $1,030/T, up $135/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

02/24/2023: European Aluminum Smelters Improve, But Not Enough To Entice More Production 02/22/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 02/07/2023: Will Aluminum's Rally Continue? 01/24/2023: Peruvian Protests Could Support Copper Prices 01/11/2023: Nickel Prices Could Remain Volatile Into 2023 |

|||||

Notable News |

|||||

|

2/24/2023: A Proclamation on Adjusting Imports of Aluminum Into the United States 2/24/2023: U.S. Treasury sanctions Russian mining sector, goes after sanctions evasion 2/24/2023: U.S. targets Russia with sanctions, tariffs on war anniversary 2/23/2023: First Quantum suspends ore processing at disputed Panama mine 2/22/2023: Rio Tinto slashes dividend as profit plunges on slower China demand 2/21/2023: US HRC: Prices jump as mills again hike prices 2/21/2023: BHP Group says reform to LME nickel contract 'long overdue' |

|||||