|

Automakers & Mining Investments To secure supplies of battery metals such as cobalt, lithium, and copper, automakers such as Tesla, GM, and Stellantis (formerly Fiat Chrysler) are considering or have already invested in mining operations throughout the world, according to Bloomberg and Reuters. However, earlier this week Goldman Sachs commented that these investments will likely “end in tears” due to the expertise involved in mining projects. Extrapolating further, Goldman Sachs stated, “car companies will be better off sticking to their core competencies and reducing their exposure to commodity price swings through hedging.” |

AEGIS fully agrees with these comments. More importantly, AEGIS is very adept at creating and implementing strategies for cobalt, copper, and other battery metals. This might include a variety of strategies involving swaps and options. For example, LME copper has sufficient liquidity for both swaps and options. CME Cobalt futures has seen explosive growth in open interest in recent months. Please note that there is no options market for CME cobalt. As for lithium, open interest remains low. However, if you need to hedge lithium, we suggest using limit orders. This would allow control of the purchase price. If you are attempting to buy the April '23 lithium contract at a price of $72/kg or better, a limit order may be deployed. Please contact AEGIS for specific strategies that fit your operations.

|

Aluminum

Last month, smelters in China’s top aluminum production region, Yunnan province, curtailed another 650,000 to 800,000 mt in annual capacity due to power rationing, according to Caixin. This is even deeper than the 415,000 mt of annual capacity requested by local authorities in mid-February. AEGIS notes that aluminum prices are essentially flat since this latest round of curtailment requests and are similarly flat on the year. Given that LME aluminum prices were down over 15% last year, and that supply issues in China are potentially bullish, AEGIS believes this is an excellent time for consumers to lock in future usage. (Source: Bloomberg)

AEGIS also notes that this latest round of curtailments now brings Yunnan province’s total cuts to 1.9 million mt in annual production capacity, meaning that approximately one-third of the region’s production is now offline. At 5.3 million mt, Yunnan Province’s annual capacity is responsible for about 12% of China’s aluminum production capacity. AEGIS also wonders how long this production will remain offline, and more importantly, if Chinese consumers will need to fill the void by further relying upon imports. Likewise, will more curtailments occur, and will that force end-users to pull even more from global supplies?

The saga regarding Russian metals in the LME continues. On Tuesday, the LME announced that Russian metals cannot be delivered to US-based LME warehouses. This action stems from the White House’s announcement last week that it will soon implement a 200% tariff on imports of Russian aluminum. AEGIS believes that the LME’s announcement will have little to no market impact on the Midwest Premium (MWP) because there is currently no Russian primary aluminum, lead, nickel, or copper in US-based LME warehouses. However, if you are concerned that this might have a bullish impact, AEGIS believes US consumers should maintain their standard hedging policy. (Source: LME)

AEGIS notes that although no other major importers of aluminum have implemented a similar tariff, it remains to be seen what the LME will do if other countries also apply a restrictive tariff. The White House’s tariffs would essentially block imports of Russian aluminum from the US market. If other importers follow suit, would the LME block deliveries of Russian metals into other warehouses, namely in Europe? We note that South Korean warehouses hold most of the Russian-origin primary aluminum that is in the LME system. Thus, like the US, blocking Russian metals from Euro-based warehouses would likely have a minimal market impact.

However, AEGIS believes the White House’s announcement could have a wider implication for aluminum import premiums. For example, if Euro-zone countries implement a similar tariff, major buyers would be forced to seek out other suppliers. European import premiums have already rallied about 19% this year due to shortages of high-purity aluminum and could rally further if Russian supplies are blocked from the market. More importantly, as we compete for the same cargoes, this could push the US MWP higher. The MWP has rallied over 44% due to the high-purity aluminum shortages in Europe and could rally further if more Russian supply is blocked from the market.

Copper

Last Thursday, First Quantum Minerals, the parent company of the huge Cobre Panama copper mine, stated that they have been forced to stop ore processing at the mine because the Panamanian government is blocking its metal from being loaded at the port. This presents a potentially bullish price risk for consumers, as blockage keeps nearly 1.5% of the global copper off the market. Even though prices have already rallied by over 6% in 2023, this could still be a good time for end-users to implement a long-term hedging program.

First Quantum Minerals believes this blockage is a negotiating tactic stemming its ongoing dispute with the Panamanian government over tax and royalty payments. However, the Panamanian government claims it’s a compliance issue that is not related to the dispute. Based on USGS figures and company data, Cobre Panama produced 351,000 mt of copper in 2022, making it responsible for approximately 1.5% of global production.

AEGIS notes that this export blockage adds to the woes that the Central and South American copper mining industries have faced in early 2023. Political protests and subsequent road blockages in southern Peru have forced several of the world’s copper mines to curtail production fully or partially. In neighboring Chile, water supply issues and project delays have led to lower-than-expected production volumes in 2022 and 2023. Chile and Peru are the world’s largest and second-largest copper producers, according to the USGS. (Sources: Bloomberg, Reuters, USGS)

Russia’s Metal Sales

Last Friday, the White House announced it will increase tariffs on imports of Russian aluminum to 200%, up from the current level of 35%. Prior to this announcement, Reuters recently suggested that Russia might retaliate by banning sales of palladium and nickel to the US. Even though US import premiums for palladium and nickel cannot be directly hedged, AEGIS believes that most of the price risk that could come from such a ban can be hedged via palladium or nickel swaps.

The possibility of Russian banning sales of nickel and palladium is of grave importance, as the US gets approximately 35%, or 20 mt, of its palladium imports from Russia. Similarly, 11%, or 92,000 mt, of US nickel imports come from Russia. If Russia bans exports of palladium and nickel to the US, then American buyers need to source these metals from other suppliers. Please keep in mind that if Russian metal is sold elsewhere, it suppresses that region's price via more supply, and supports the US price, via less supply. As we compete for the same cargoes as other major importers, such a ban could create havoc on US import premiums. (Sources: Bloomberg, Reuters, Trade Data Monitor)

Please note that although there are assessments for nickel import premiums into the US, this premium cannot be directly hedged by a futures or swaps market. There are no known import premiums for palladium. Thus, the lack of tradable financial products further complicates the issues that American palladium and nickel buyers could face.

|

|

|||||

|

|

|||||

LME Aluminum |

|||||

|

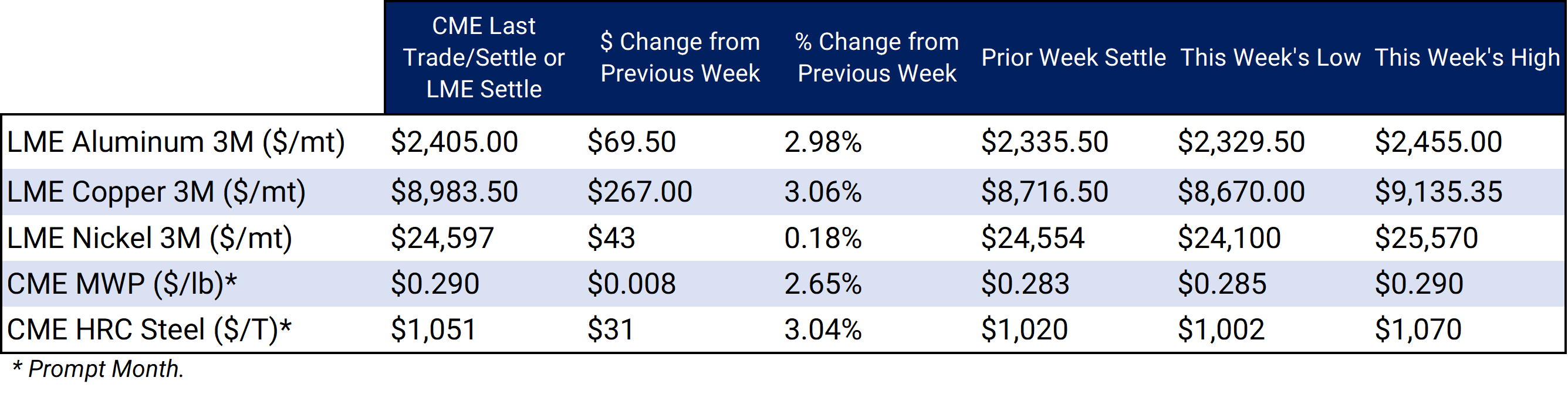

LME Aluminum 3M settled at $2,405/mt, up $69.50/mt on the week. Aluminum prices were up this week. This has caused the forward curve to shift vertically higher by approximately $70/mt. It remains in contango, meaning that nearby prices are lower than forward prices. Aluminum consumers concerned about increasing prices might consider hedging future needs by buying swaps or call options. End-users might consider strategies that use only swaps or options or a combination of both, depending on risk tolerance. The aluminum market has sufficient liquidity to use swaps and options. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|||||

|

Prompt month CME MWP last settled at 29.0¢/lb this week. The CME Midwest Premium market is backwardated through July 2023 but then becomes largely flat for the remainder of this year. The CME Midwest Premium swap market is thinly traded, and there is no options market. Hedging in this thinly traded market is challenging, so we recommend using strategically placed limit orders. Please contact AEGIS for specific strategies that fit your operations. * Please note all these charts are for desktop only. * |

|||||

LME Copper |

|||||

|

LME Copper 3M settled at $8,983.50/mt, up $267/mt on the week. Compared to last Friday, LME Copper's forward curve has shifted higher by about $270/mt. The forward curve is now relatively flat throughout 2023 but becomes backwardated in 2024 and beyond. The copper market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon their risk tolerance. Please contact AEGIS for specific strategies that fit your operations.

|

|||||

|

|||||

|

LME Nickel 3M settled at $24,597/mt, up $43/mt on the week. As prices were upthis week, nickel’s forward curve has also shifted vertically higher, by about $40/mt. It remains in contango, meaning that spot prices are lower than futures prices. The nickel market has sufficient liquidity to use swaps and options. Consumers might consider strategies that use only swaps or options or a combination of both, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

|

|

|||||

CME Hot Rolled Coil (HRC) Steel |

|||||

|

Prompt month HRC Steel last settled at $1,051/T, up $31/T on the week. For CME HRC Steel, liquidity is low for swaps, but hedging can still be done with limit orders. The same is true for options. Similar to other metals, a combination of both swaps and options might work in certain cases, depending upon your risk tolerance. Please contact AEGIS for specific strategies that fit your operations. |

|||||

|

|

|||||

AEGIS Insights |

|||||

|

03/01/2023: AEGIS Factor Matrices: Most important variables affecting metals prices 02/24/2023: European Aluminum Smelters Improve, But Not Enough To Entice More Production 02/07/2023: Will Aluminum's Rally Continue? 01/24/2023: Peruvian Protests Could Support Copper Prices 01/11/2023: Nickel Prices Could Remain Volatile Into 2023 |

|||||

Notable News |

|||||

|

3/3/2023: Volkswagen board discusses two new North America plants at meeting - sources 3/2/2023: Lithium miner SQM's profit more than triples on EV demand 3/2/2023: Aluminium open interest, volume on CME hit record high in February 3/1/2023: Tesla plans 6,000 jobs in Mexico and eyes more investment, government says 3/1/2023: Freeport Indonesia says Grasberg mine operations back to normal after floods 2/28/2023: Panama and Canada's First Quantum nearing agreement over copper mine -lawyer 2/28/2023: LME halts flow of Russian metals into its U.S. warehouses 2/28/2023: Column-United States targets Russian aluminium and other metals: Andy Home 2/28/2023: Analysis: Lithium price slide deepens as China battery giant bets on cheaper inputs 2/27/2023: A $1.5 billion hoard of copper and cobalt is piling up in Congo 2/27/2023: Stellantis invests $155 mln in Argentine copper mine 2/27/2023: Trafigura lines up Russia aluminum deal in challenge to Glencore |

|||||